Flashback:

– Gold is a Crap Investment – Unless …

– Inflation, Hyperinflation and Real Estate (Price Collaps)

What the Fed is looking at.

– What If There’s A Recession in 2014? (Gonzalo Lira, Dec 16, 2013):

If policymakers were gunfighters, they’d be out of bullets: They have run out of effective policy tools to improve the economy.

So the question is simple: If there is a recession in 2014, and policymakers are out of bullets, how will it play out across the American economy?Recently, Deutsche Bank’s Jim Reid very astutely pointed out that the current “expansion” of the U.S. economy is on its fifth year—the seventh longest in history.

We are due for a recession.

Now, before facing up to a possible 2014 recession, let’s ask ourselves: What happened during the last recession?

No one can quite agree as to the specific causes of the 2007–09 recession—and fighting that particular fight isn’t the point of this essay. But we can all more or less agree that global overindebtedness caused a mini-Minsky Moment, whereby borrowers could no longer borrow enough to keep from defaulting on their previous loans. Hence September 2008. Hence the collective global “Ahhh!!!!” moment that we all recall with such sweet and fond nostalgia.

To stave off what looked like financial and economic Armageddon, the Treasury Department first under Henry Paulson and then under Timothy Geithner, and the Federal Reserve under Ben Bernanke, basically threw money into the economy: The Treasury’s Troubled Asset Relief Program (TARP) originally authorized $700 billion to buy up toxic assets, while the Fed created the Maiden Lane vehicles, lowered interest rates to zero (zero interest-rate policy, ZIRP), and simultaneously created money by way of the various iterations of Quantitative Easing (QE).

Combined, these Treasury and Fed programs prevented the bankruptcies of the so-called “systemically important” (a.k.a., “Too Big To Fail”) banks, and provided the U.S. Federal government with the cash to carry out the 2009 stimulus program. After all, had it not been for the Fed’s purchases of Treasury bonds by way of QE, the yields on the government’s bonds would have risen so high that the stimulus program could not have been financed, let alone the +$1 trillion deficits of 2009, 2010, 2011 and 2012.

But screw the deficit—the Treasury and Fed measures saved everybody’s bacon. Equities crashed? Houses underwater? 401(k)’s in the toilet? Thanks to TARP, ZIRP and QE, they rebounded.

Rather than take the hit, work out the bad loans, and organically regrow the economy, the Treasury and Fed measures were essentially morphine—or heroin—to dull the pain of the Global Financial Crisis: They made us feel great, but the disease is still there.

Overindebtedness. Bad debts piled on top of bad debts.

Now because of the Treasury’s and especially the Fed’s morphine/heroin drip, starting in Q3 of 2009, the American economy’s gross domestic product has been expanding, which economists hail as the end of the 2007–09 recession, and the beginning of the current “expansion”.

(Re. the “expansion”: Nevermind that unemployment was scrapping 10% as late as Q3 of 2011, and that as of Q4 of 2013, we are still at 7% U-3 unemployment—and this U-3 figure ignores the long-term unemployed, who have simply given up, reducing the employment participation rate to historic lows, thereby skewing the real unemployment figure something awful.)

So here we are in Q4 of 2013, staring down the barrel of 2014, suspecting—fearing—that we might have a recession staring right back at us.

Question: What could the Federal government and the Federal Reserve realistically do, to avert a recession in 2014? Or if not avert it, at least ameliorate its effects?

Oh boy . . .

Insofar as the Federal government is concerned, realistically, nothing. In 2008, facing what appeared to be the end of the financial world, Congress was snookered into agreeing to the Bush Administration’s $700 billion TARP bailout. Then in 2009, the incoming Obama Administration had two winds at its back—the Global Financial Crisis, which required the incoming administration to do something, anything; and the fact that Obama was the new prez, who’d won decisively with his deceptive talk of “hope”. Thus the $787 billion stimulus package.

Combined, the Bush TARP and the Obama stimulus were some $1.5 trillion mainlined into the American economy.

Today, five years after his inauguration, and after the Government shutdown and the botched Obamacare launch, Obummer just doesn’t have the pull. More to the point, the Democratic caucus does not trust him. So Democrats on the Hill will not stick their necks out for an Obama stimulus program. So the O-Administration’s economic brain trust might come up with all sorts of plans to preëmptively stop a 2014 recession—but they don’t have the votes to make these plans happen.

As to a repeat of the Henry “Give-us-all-your-money-or-the-banks-will-die!” Paulson scare tactics—they won’t work today, not after the nasty taste left by the one in 2008.

So macro-economically speaking, Barack Obama is walking around with an empty peashooter: He can’t even wave the threat of using it without seeming foolish.

Turning now to the Federal Reserve: They might be packing a big ol’ .45 Magnum, but they are most definitely out of bullets. They can’t lower interest rates any further than they have—what are they going to do, start charging people who deposit money in banks? This is the problem with hitting the lower bound: You can’t go any lower than ZIRP. At best, the Fed could expand QE even further, and buy up even more Treasury debt. But then any impact from more QE will be marginal, assuming it has any effect at all.

So if the Federal government and the Federal Reserve are essentially out of bullets, what’s going to happen to us law-abiding citizens when the Big Bad Recession comes rolling into town?

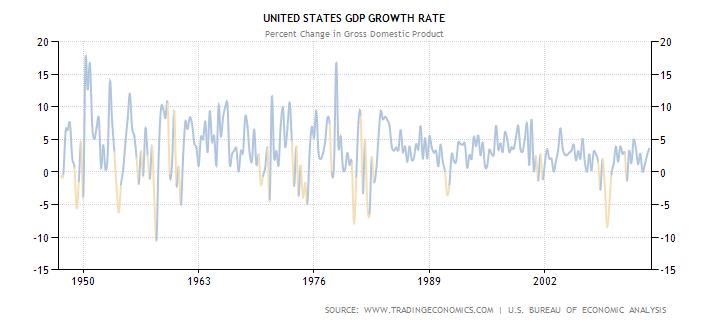

First off, no one can seriously or responsibly doubt that a recession will not come. Even if the American economy by some miracle manages to sneak through 2014 with positive numbers, a downturn will hit in 2015 anyway. Don’t believe me? Check out this chart:

I have grounded, non-orthodox reasons to think that a recession will hit in 2014, reasons which I will expand upon during my live presentation next Thursday (see here). But even if you don’t buy my heterodox reasons, the orthodox business cycle would confirm that a recession is on its way.

So to weather it, you’d have to know what’s going to happen.

A basic outline is pretty clear:

Stocks will take the brunt of the beating, once recession-fever hits—after all, equities are floating on nothing but QE, and everybody knows it.

Bonds won’t do so well either, at least not corporate issuance. Treasury bonds will continue trending with flat yields, if only because the Federal Reserve will probably signal that it will continue (or even expand) QE. Treasury bonds will also continue high because of a simple safe-haven play . . . but there won’t be the sense of today’s Treasuries being the rock-solid Treasuries of yore: There will be more volatility in the T-bond markets. A greater willingness to exit Treasuries at a moment’s notice, especially if there are hints of inflation.

Real estate? Forget it—it’ll be another popping bubble, with the same damage as the last one.

The only store of value will be commodities. Not just precious metals, but all commodities: Industrials, agros, and fossil fuels. It will simply make more sense for the investment community to rotate out of iffy stocks and dodgy bonds, and rotate into physical commodities. Why? Because there is too much liquidity.

If there is such a rotation from equities and bonds into commodities, then the prices of food and transportation will rise—precipitously.

Thus we will have inflation, possibly severe inflation. But the Fed will be loathe to rein in inflation via interest rate hikes.

You know the saying about owning a hammer, and everything looking like a nail? The Fed cannot conceive of any way in which to help the economy that does not involve keeping interest rates low. The Fed under Bernanke (and Greenspan previously, who was guilty of the same sin) does not understand that it is not the job of the Fed to maintain full employment, stable prices, and a solvent banking sector. The Fed’s only mission is to ensure the stability of the fiat currency. Full employment? That’s the Federal government’s problem. Banking sector solvency? That’s not the government’s problem, that’s the free market’s problem.

But the Fed, blinded, thinks that it has to support the banking sector and try to do something about employment. Thus it has lowered interest rates to laughable/insane levels. And it cannot raise them because of its own bias: “You don’t raise interest rates during a recession” is practically a Zen koan with the Fed economists.

If commodities start to rise, as a market reaction to falling stock prices and a need to find an investment safe-haven, then inflation will rear its ugly head and hurt the American economy very, very badly. But the Fed—repeating exactly the same error that brought us stagflation—will not raise interest rates to quell it. The Fed will be too frightened of smothering the economy during a recession to raise rates and defend the currency.

Thus the Fed will stand pat with ZIRP and QE, come a recession in 2014.

In other words, the government will not be able to save the economy. This is the single point I’m trying to make here: If you think for a second that the Federal government and the Federal Reserve will step in once again and save everyone’s bacon (like the last time), then you have not been paying attention to what I’ve been saying—or been paying attention to how truly helpless the Obama Administration and the Fed really are.

The Federal government and the Federal Reserve are out of bullets.

Which means we are on our own come a recession. And we’ll be paying not only for the recession of 2014, but also for the recession of 2007-09, which was deferred, but not worked out.

In other words, a recession in 2014 just might well be The Big One.

Oh boy . . .

Okay, that’s my thinking—here’s my pitch: This coming Thursday, at 8pm EST, I’m going to give a live presentation that’s going to look into all these issues in a lot more detail—really start us thinking seriously about what to do, if and when a recession hits the American economy. The title of this web seminar? Simple:

“What A Recession in 2014 Will Look Like”

Click on the link—and in case you missed it, here it is again. In this live presentation, I will expand on this brief essay, and will take audience questions, too.If you’re not sure if I’m an idiot or not, check out my appearance on Max Keiser last year and see for yourself:

Avert a recession in 2014? Five years of growth? Where are the idiots getting their numbers? We have been in a contraction since 2007-08, there is NO recovery except in the fake numbers put out by this government.

If this is recovery, I hate to think what more recession will do. Look at food, energy and sheltering costs, they are through the roof…….but they are not counted in the inflation factor.

There are lies, damn lies and statistics.