Back in December 2014, when we first learned that Japan was willing to risk hundreds of billions in Japanese pensions to boost and prop up the domestic stock market – the only true “”arrow of Abenomics – by shifting cash out of bonds and into stocks in the country’s gargantuan (and world’s biggest) $1.4 trillion Government Pension Investment Fund, or GPIF, we wrote that “The GPIF Has A Warning For Japan’s Citizens: Abenomics Better Work, Or Your Pensions Are Toast.”

As the WSJ wrote then, “Japan’s $1.1 trillion government pension fund is betting that a long-term recovery and rising corporate profits will push Tokyo stock prices higher, helping the fund increase returns for the nation’s retirees. Mr. Abe has pushed for the fund to become a more aggressive and sophisticated investor. The fund decided in October to shift its portfolio to seek higher returns, slashing its target allocation to domestic bonds almost in half while nearly doubling that of domestic and foreign equities.”

Expectations that Mr. Abe’s policies will succeed have already helped double Japan’s benchmark stock index since late 2012. Further gains would no doubt benefit GPIF’s ¥23.9 trillion ($202 billion) domestic stock portfolio.

Oops.

Less than 2 years later, Abenomics is in tatters, the Japanese economy yoyo’s from recession to negligible growth, while the stock market has slid into a bear market having lost a quarter from its recent highs as a result of a surge in the Yen as the BOJ has largely wiped out all of its credibility with the now widely mocked decision to unleash negative rates.

And while all of the above is terrible news for Japan, whose demographic implosion assures a deflationary black hole no matter how much money the BOJ prints, those most impacted by Abe’s reckless decision are the country’s pensioners. Because as we concluded in December 2014, “unfortunately, for Japan, and its tens of millions of pensioners, the only news here is simple: the entire country is now held hostage by Japan’s last-gasp attempt to prove Monetarist and Keynesian policies work. Because, said otherwise, “Abenomics better work, or else all your pensions are toast.”

Sadly, this process is now in play. Late last week, Morgan Stanley’s Yohei Iwao calculated that after suffering ¥5 trillion in losses in the year ended March 31, the GPIF has started off the new year with a another anti-bang, losing another ¥4.4 trillion in losses in the first quarter, or a total of just under $100 billion.

So with Abenomics careening off the cliff and headed for a traumatic death, and with Kuroda having become the laughing stock of central bank circles, has Japan finally learned its lesson? Will the GPIF rotate out of money-losing stocks and back into bonds which are currently trading at record high prices? According to Morgan Stanley, the answer is not a chance, for the simple reason that as a result of an upcoming asset rebalancing, the GPIF will have no choice but to buy even more money-losing stocks.

As Bloomberg reports, because shares held by Japan’s $1.4 trillion Government Pension Investment Fund have suffered such large losses, it will need to add to those holdings to meet targets for their weighting, while selling sovereign bonds whose value has soared. Assuming no re-weighting was done since Jan. 1, GPIF will need to buy 4.2 trillion yen ($41 billion) of local stocks and sell 9.8 trillion yen of Japanese government bonds to reach its goals. The brokerage didn’t give a time frame for this buying.

“Many foreigners think the pension rebalancing story is over,” said Yohei Iwao, executive director of the institutional equities division at Morgan Stanley MUFG. “But if we see any confirmation of more buying, it could help sentiment, at least in terms of pensions being there to support the downside.”

This may be good news for the short-term as a third party helps the BOJ in pushing stocks higher, but in the longer-run it simply guarantees even more losses as the Yen surge continue on the back of a Japanese economy that has lost virtually all levers to grow, including currency debasement. It also means that once the “rebalancing” dry powder is gone, there will be that much less in “money on the sidelines” after the upcoming buying spree.

Others, most notably those who will be selling all they can to the giant pension fund, are delighted:

GPIF rebalancing “is going to put a floor on stock declines in a market that’s full of uncertainty — it’s big,” said Koichi Kurose, Tokyo-based chief market strategist at Resona Bank Ltd. “It’s also important for the BOJ. A welcome story for them.”

The mechanics of the rebalancing are simple: Japanese stocks probably accounted for about 22% of GPIF’s holdings at the end of last month, while domestic debt made up 43% of assets, according to Morgan Stanley. He based his calculations on GPIF’s 23% weighting in domestic shares and 38 percent allocation to local bonds at the end of December and adjusted for market moves since then.

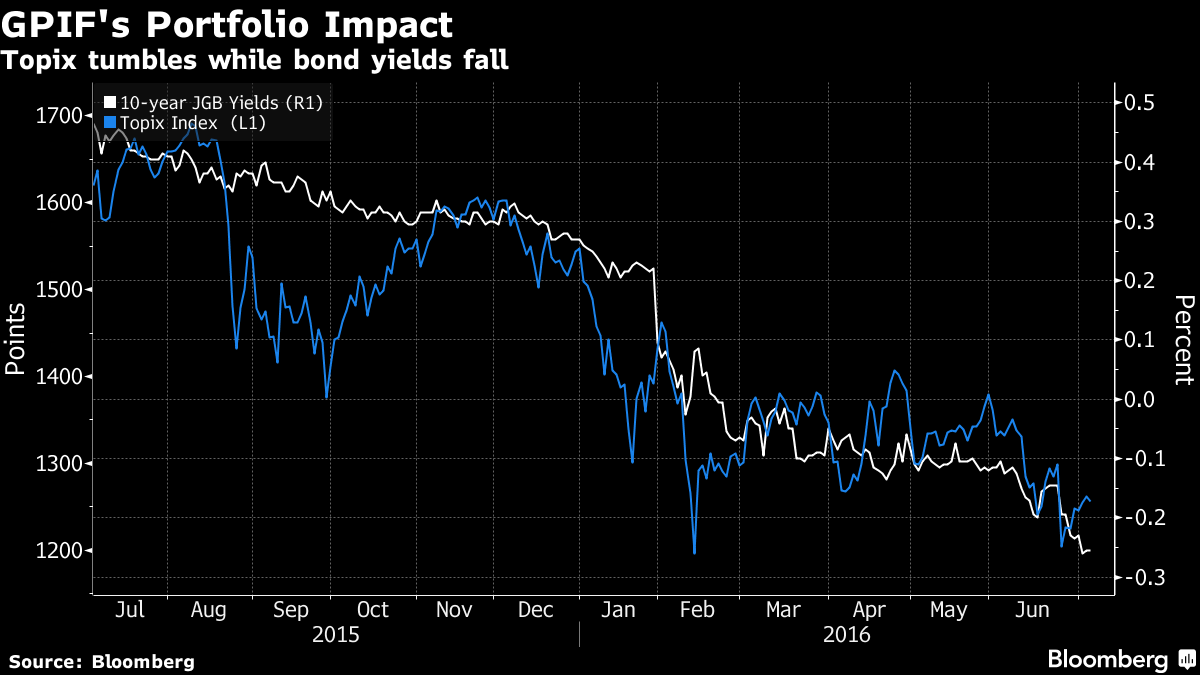

Meanwhile, the net upside from the GPIF’s recent capital allocation into stocks has already been more than wiped out as a result of the bear market in Japanese stocks. The Topix slumped 19% this year through June. Ironically, had the GPIF remains mostly in bonds, it would have a greater AUM than ever before: 10-year JGB yields tumbled to as low as minus 0.24% in the first half, while the yen gained about 16 percent against the dollar. This means nominal JGB prices have never been higher, which is bad news for those GPIF managers who dumped bonds to buy stocks… and lose trillions of yen in the process

* * *

There is a small glimmer of hope the pension fund won’t all all in just yet: while its portfolio structure means GPIF needs to buy more Japanese stocks and sell local debt, the pension’s managers are facing pressure from opposition lawmakers to do the contrary. Yukio Edano, secretary general for the opposition Democratic Party of Japan, says GPIF has gambled with the state’s pension by shifting into stocks from bonds, and called for a reversal of strategy, the Asahi newspaper reported this month.

Another possibility is that, like in the US, where defined benefit pension plans are about to “throw in the towel” and rush headlong into purchases of long duration securities to offset their liabilities, Japan will likewise end its idiotic gamble with people’s savings all in the name of propping up stocks, and at least preserve the purchasing power that locals have worked all their lives to accumulate.

Still, this is virtually assured not to happen thanks to “astute advisors” such as Resona Bank’s Kurose who says “that’s exactly what they shouldn’t be doing. The only question is the timing…. They may take their time,” Kurose said, adding it could take between six months to a year to reach their targets. “It may not be enough to chase shares higher, but it’s enough to wipe out concerns of shares falling further.”

And that’s the kind of brilliant insight that Paul Krugman delivered to Abe several years ago when he first proposed this idea.

Sadly, for Japan, it is too late: as we explained before, the entire country is now held hostage by Japan’s last-gasp attempt to prove that Abenomics is right, even if it is now all too clear what the endgame is.

As such, out condolences to Japan’s retirees: not only do you face a demographic implosion, but you will have to face it with no funds once Abenomics is done propping up the market “other people’s money”, even if in this case the money belongs to all those tens of millions who have worked hard for decades to save it an allocate it wisely instead of handing it over to a lunatic with a monetary deathwish.

* * *

Finally, if there is still any confusion how all this plays out, re-read: “Paul Krugman Is “Really, Really Worried” That He Might Have Screwed Up Japan.” And just because “Krugman is Krugman”, we’re never more than one Google search away from a hilarious soundbite from the New York Times blog archives, and so it’s with great pleasure and with everything said above in mind, that we leave you with the following excerpt from a Krugman classic entitled “Why Keynes Is Slowing Winning” ca. 2014:

“Why does the tide finally seem to be turning? Partly, I think, it’s just a matter of time; after six years it’s becoming hard not to notice that the anti-Keynesians have been wrong about everything. And the refusal of almost everyone on the anti-Keynesian side to admit any kind of error has gradually made them look ridiculous.”

* * *

PayPal: Donate in USD

PayPal: Donate in EUR

PayPal: Donate in GBP