– Former IMF Chief Economist Admits Japan’s “Endgame” Scenario Is Now In Play:

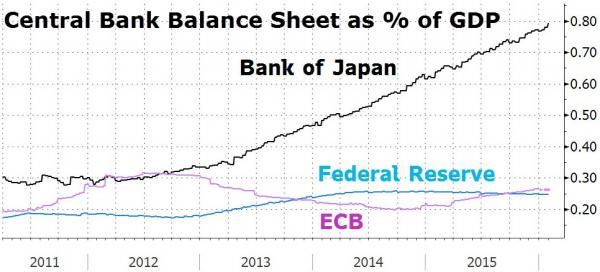

Back in October 2014, just after the BOJ drastically expanded its QE operation, we warned that the biggest risk facing the BOJ (and the ECB, and the Fed, and all other central banks actively soaking up securities from the open market) was a lack of monetizable supply. We cited Takuji Okubo, chief economist at Japan Macro Advisors in Tokyo, who said that at the scale of its current debt monetization, the BOJ could end up owning half of the JGB market by as early as in 2018. He added that “The BOJ is basically declaring that Japan will need to fix its long-term problems by 2018, or risk becoming a failed nation.”

Which is why 17 months ago we predicted that, contrary to expectations of even more QE from Kuroda, we said “the BOJ will not boost QE, and if anything will have no choice but to start tapering it down – just like the Fed did when its interventions created the current illiquidity in the US govt market – especially since liquidity in the Japanese government market is now non-existent and getting worse by the day.”

As part of our conclusion, we said we do not “expect the media to grasp the profound implications of this analysis not only for the BOJ but for all other central banks: we expect this to be summer of 2016’s business.”

Since then, the forecast has panned out largely as expected: both the ECB and BOJ, finding themselves collateral constrained, were forced to expand into other, even more unconventional methods of easing, whether it be NIRP in the case of the BOJ, or the outright purchases of corporate bonds as the ECB did a month ago.

* * *

Then, in September of 2015, the IMF realized the severity of what our forecast meant for Japan, and released a working paper with the non-pretentious title “Portfolio Rebalancing in Japan; Constraints and Implications for Quantitative Easing“, which however had momentous implications because it was a replica of what we had said a year earlier.

In the paper, the IMF said that the Bank of Japan may need to reduce the pace of its bond purchases in a few years due to a shortage of sellers. The paper predicted a world in which, just as we cautioned, “the BoJ may need to taper its JGB purchases in 2017 or 2018, given collateral needs of banks, asset-liability management constraints of insurers, and announced asset allocation targets of major pension funds… there is likely to be a “minimum” level of demand for JGBs from banks, pension funds, and insurance companies due to collateral needs, asset allocation targets, and asset-liability management (ALM) requirements. As such, the sustainability of the BoJ’s current pace of JGB purchases may become an issue.”

The paper’s shocking punchline was how Japan would survive this inevitable phase shift, or as we rhetorically asked, what happens when the regime shifts from the current buying phase to its inverse: The IMF response: “As this limit approaches and once the BoJ starts to exit, the market could move from a situation of shortage to one with excess supply. The term premium could jump depending on whether the BoJ shrinks its balance sheet and on the fiscal deficit over the medium term.

When considering that by 2018 the BOJ market will have become the world’s most illiquid (as the BOJ will hold 60% or more of all issues), the IMF’s final warning is that “such a change in market conditions could trigger the potential for abrupt jumps in yields.”

Or as we put last September, “at that moment the BOJ will finally lose control.”

We even timed it: “But before we get to the QE endgame, we first need to get the interim point: the one where first the markets and then the media realizes that the BOJ – the one central banks whose bank monetization is keeping the world’s asset levels afloat now that the ECB has admitted it is having “problems” finding sellers – will have no choice but to taper, with all the associated downstream effects on domestic and global asset prices.

It’s all downhill from there, and not just for Japan but all other “safe collateral” monetizing central banks, which explains the real reason the Fed is in a rush to hike: so it can at least engage in some more QE when every other central bank fails.

But there’s no rush: remember to give the market and the media the usual 6-9 month head start to grasp the significance of all of the above.

Sure enough, it took the market about 6 months to finally grasp that the BOJ is out of ammo: the result has been a dramatic surge in the Yen coupled with a plunge in the Nikkei, meanwhile Kuroda is left scratching his head what he can do in a world in which the G-20 have specifically prohibited him from easing and making the dollar stronger as that will lead to a return of China’s weak currency-driven, capital outflow crisis.

As for our other forecast from October 2014 in which we said “expect the media to grasp the profound implications of this analysis not only for the BOJ but for all other central banks: we expect this to be summer of 2016’s business” this too was quite prescient. Because while summer is just around the corner, earlier today the mainstream media, in this case the Telegraph’s Ambrose Evans-Pritchard, finally caught up with a piece titled: “Olivier Blanchard eyes ugly ‘end game’ for Japan on debt spiral.” In it he cites none other than the IMF’s former chief economist, Olivier Blanchard who left the IMF just at the time the IMF’s study from last September was made public.

The content of Pritchard’s piece should be familiar to anyone who has followed our musings on this topic for the past two years.

In it, he says that “Japan is heading for a full-blown solvency crisis as the country runs out of local investors and may ultimately be forced to inflate away its debt in a desperate end-game, one of the world’s most influential economists has warned.”

From the article:

Olivier Blanchard, former chief economist at the International Monetary Fund, said zero interest rates have disguised the underlying danger posed by Japan’s public debt, likely to reach 250pc of GDP this year and spiralling upwards on an unsustainable trajectory.

Prof Blanchard said the Japanese treasury will have to tap foreign funds to plug the gap and this will prove far more costly, threatening to bring the long-feared funding crisis to a head.

“If and when US hedge funds become the marginal Japanese debt, they are going to ask for a substantial spread,” he told the Telegraph, speaking at the Ambrosetti forum of world policy-makers on Lake Como.

Analysts say this would transform the country’s debt dynamics and kill the illusion of solvency, possibly in a sudden, non-linear fashion.

That moment in which the illusion dies, is precisely the phase shift which we descibed in September as the moment “market conditions could trigger the potential for abrupt jumps in yields.”

Said otherwise, from plummeting deflation Japan would be faced with soaring yields and hyperinflation as the last recourse buyer, the BOJ, is swept aside.

Prof Blanchard, now at the Peterson Institute in Washington, said the Bank of Japan will come under mounting political pressure to fund the budget directly, at which point the country risks lurching from deflation to an inflationary denouement.

“One day the BoJ may well get a call from the finance ministry saying please think about us – it is a life or death question – and keep rates at zero for a bit longer,” he said.

Pritchard here catches up to what we said in October of 2014, namely that the “BoJ is soaking up the entire budget deficit under Govenror Haruhiko Kuroda as he pursues quantitative easing a l’outrance.” Incidentally, this is the same Pritchard who several years ago was lauding Japan’s QE.

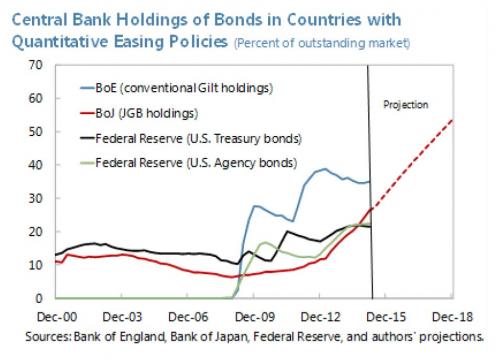

He next points out something we have also warned about for year: “the central bank owned 34.5pc of the Japanese government bond market as of February, and this is expected to reach 50pc by 2017.”

This is us circa last September.

What comes next is the scary part, the part we have been focusing on for years:

Prof Blanchard did not elaborate on the implications of Japan’s woes for the global financial system, but they would surely be dramatic and there are growing fears that this could happen within five years. Japan is still the world’s third largest economy by far. It is also the global laboratory for an ageing crisis that the rest of us will face to varying degrees.

Once markets begin to suspect that Tokyo is deliberately engineering an escape from its $10 trillion public debt trap by means of an inflationary ‘stealth default’, matters could spin out of control quickly.

It might lead to an abrupt reappraisal of sovereign debt risk in other parts of the world, especially in Europe with its own Japanese pathologies of low-growth and bad demographics. Roughly $7 trillion of debt is trading at negative yields worldwide, an accident waiting to happen for the bond market.

After Japan comes Europe:

Prof Blanchard said the risk for the eurozone is the election of populist “rogue governments” that let rip with spending in defiance of Brussels. “Investors would have serious thoughts about buying their sovereign bonds,” he said. The European Central Bank would be legally prohibited from activating its back-stop mechanism (OMT) to prevent yields soaring since these governments would not be in compliance with EU rules. “Some of them have very high debt and presumably would have to default,” he said.

Perhaps, or the ECB will simply unleash the first helicopter money if it can get over the loud German chorus of disagreement. Although once Europe launches Helicopter money, it will be promptly followed by the US as the global monetary devaluation round enters the final sprint. It is no coincidence that earlier today none other than Ben Bernanke admitted that “Helicopter Money May Be The Best Available Alternative.”

What shape the final stand of failed monetary policy takes, is irrelevant. What is relevant, is that for the first time, not only is the Japanese doomsday scenario finally in the mainstream press, but it is acknowledged by none other than one of the Keynesian luminaries AEP is so impressed by:

Prof Blanchard is one of the world’s top theoretical economists over the last quarter century and might have won the Nobel Prize by now if he had not been cajoled into IMF service by his fellow Frenchman, Dominique Straus-Kahn.

He transformed the IMF into a brain-trust of progressive ‘Keynesian’ thinking, much to the fury of Berlin. A leaked document from the German finance ministry said the institution should be renamed the ‘Inflation Maximizing Fund’.

Evans-Pritchard’s conclusion:

“Professor Blanchard has had the last laugh on that joke. Seven years after the Lehman crisis the eurozone is in outright deflation and yields on 10-year German Bunds are trading at an historic low 0.11pc. Touché.”

Actually let’s check back in another 7 years, because now that even one of the world’s “top theoretical economists” acknowledges that the endgame for trillions in debt ends in a hyperinflationary supernova, and not a deflationary black hole, all those years of sliding interest rates around the globe are about to be flipped on their head. At that point it will be the Germans who are laughing last.

Sadly, there will be nothing else to laugh about as the Keynesian “progressive thinkers” will have finally reached the inevitable and disastrous “end-game” of their failed religion.