“The conditions in the economies of the rest of the world have undoubtedly proved weaker compared with a few months ago, in particular in the emerging economies. Global growth forecasts have been revised downwards. This slowdown is probably not temporary.”

– Mario Draghi Admits Global QE Has Failed: “The Slowdown Is Probably Not Temporary”:

Undoubtedly, the most amusing this about the prospect of more easing from the ECB (as telegraphed by Mario Draghi last week) and the BoJ (where Haruhiko Kuroda just jeopardized his status as monetary madman par excellence by failing to expand stimulus) is that both Europe and Japan both recently slid back into deflation despite trillions in central bank asset purchases.

In other words, the market expects both Draghi and Kuroda to double- and triple- down on policies that clearly aren’t working when it comes to altering inflation expectations and/or boosting aggregate demand. Indeed, both Goldman and BofAML said as much last week. For those who missed it, here’s Goldman’s take

The subdued and increasingly persistent inflation dynamics that have prevailed in recent years may have eroded central banks’ best line of defence in the face of adverse disinflationary shocks. The energy-price-driven decline in Euro area inflation from 2012 to 2015 has thrown this possibility into even sharper relief.

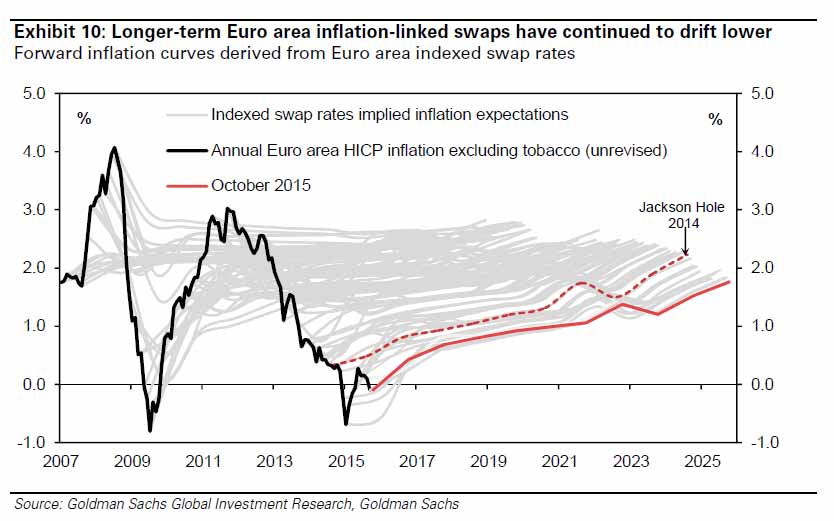

By embarking on unprecedented balance sheet operations and forward guidance, central banks in Europe have sought to ring-fence domestic inflation expectations and signal their intention to maintain monetary conditions easy for a protracted period of time. Mario Draghi himself described the ECB’s asset purchase programme as a way of ensuring that very low (and, at times, negative) inflation does not lead wage- and price-setters to adjust their behaviour to a perceived lower steady-state rate of inflation. However, judging from market-based implied measures of longer-term inflation expectations, the effectiveness of the ECB’s announcements has proved limited so far.

Or, visually:

Meanwhile, many critics have accused the ECB of adopting policies that work at cross purposes with Berlin’s insistence on fiscal rectitude. That is, the more Draghi’s PSPP drives down borrowing costs, the less effective the “market” is at pricing risk which in turn means investors aren’t able to punish governments for budgetary blunders. In other words, Spain, Portugal, and Italy shouldn’t be able to borrow for nothing based on the fundamentals, but thanks to the ECB they can – so why implement reforms?

And so, ahead of what might fairly be described as one of the most highly anticipated ECB decisions in history, everyone’s favorite Goldmanite gave an interview to Alessandro Merli and Roberto Napoletano. The transcript can be found on the ECB’s website, but we’ve included some notable excerpts below.

Perhaps the most interesting passage comes at the outset with Draghi essentially admitting that global QE has demonstrably failed:

The conditions in the economies of the rest of the world have undoubtedly proved weaker compared with a few months ago, in particular in the emerging economies, with the exception of India. Global growth forecasts have been revised downwards. This slowdown is probably not temporary. To illustrate the importance of emerging markets, it is recalled that they are worth 60% of gross world product and that, since 2000, they have accounted for three-quarters of world growth. Half of euro area exports go to these markets. The risks are therefore certainly on the downside for both inflation and growth, also because of the potential slowdown in the United States, the causes of which we need to understand fully. The crisis led to a sharp drop in incomes. It is up to us to push them up again.

So, a couple of things there. First, we agree that the “slowdown is probably not temporary.” Indeed, as we’ve documented extensively, we’ve likely entered a period of lackluster global growth and trade, and there’s every reason to believe this is structural and endemic, as opposed to fleeting and cyclical. Second, the last bolded passage there speaks volumes about what’s wrong with the current central planner “strategy.” No, Mario Draghi, it’s not “up to you” to push up incomes. It’s “up t you” to get out of the way and the market figure this out. Central planners had their chance to boost wage growth and they failed – miserably.

Here’s Draghi on the effect oil prices are likely to have on inflation expectations going forward:

As far as the next few months are concerned, the most relevant factor will be the price of energy. We expect inflation to remain close to zero, and maybe even to turn negative, at least until the start of 2016.

Of course what Draghi doesn’t say is that ZIRP is a contributor. That is, when you ensure that capital markets remain wide open, uneconomic producers continue to dig, drill, and pump and that contributes to lower prices and thus, to a deflationary impulse.

And here’s Draghi explaining that the idea of the “lower bound” is becoming antiquated thanks to Europe’s descent into NIRP:

Now we have one more year of experience in this area: we have seen that the money markets adapted in a completely calm and smooth way to the new interest rate that we set a year ago; other countries have lowered their rate to much more negative levels than ours. The lower bound of the interest rate on deposits is a technical constraint and, as such, may be changed in line with circumstances.

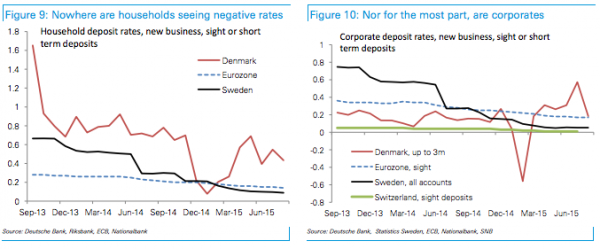

Again, it’s all about what Darghi doesn’t say. The reason NIRP is still doable is because it hasn’t yet been passed on to household deposits:

Here’s a bit from Draghi on inflating away massive debt piles…

Low inflation has two effects. The first one is negative because it makes debt reduction more difficult. The second one is positive because it lowers interest rates on the debt itself. The path on which fiscal policy has to move is narrow, but it’s the only one available: on the one hand ensuring debt sustainability and on the other maintaining growth. If interest rate savings are used for current spending the risk increases that the debt becomes unsustainable when interest rates go up. Ideally, the savings are instead spent on public investments whose rates of return permit repayment of the interest when it rises.

And finally, here’s how the ECB chief explains away the idea that central bank stimulus is incompatible with fiscal retrenchment:

Structural reforms and low interest rates complement each other: carrying out structural reforms means paying a price now in order to obtain a benefit tomorrow; low interest rates substantially reduce the price that has to be paid today. There is, if anything, a relationship of complementarity. There are also other more specific reasons: low interest rates ensure that investment, the benefits from investment and from employment, materialise more quickly. Structural reforms reduce uncertainty regarding macroeconomic and microeconomic prospects. Therefore, it is the opposite, rather than seeing an increase in moral hazard, I see a relationship of complementarity, of incentive.

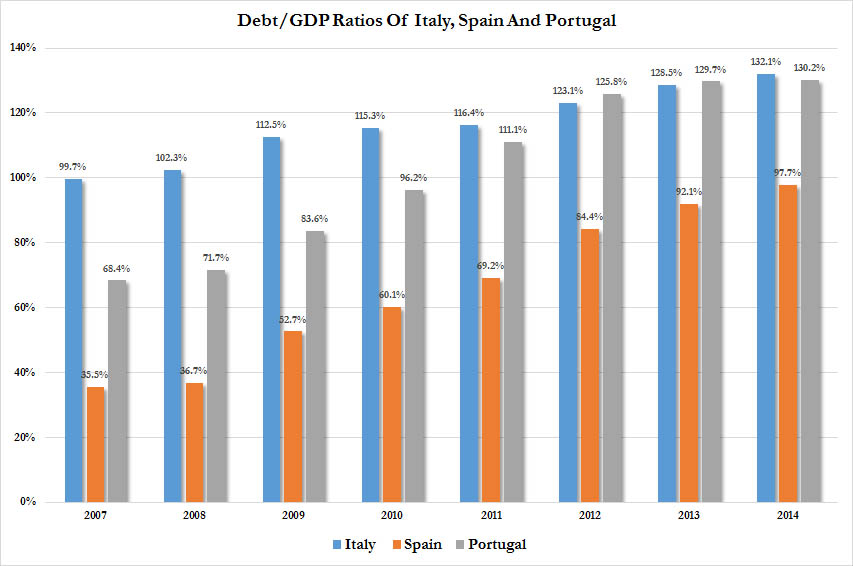

Sure. So what Draghi wants you to believe is that the EU periphery is committed to budgetary discipline and all the ECB is doing by artificially suppressing borrowing costs is making the transition to fiscal responsibility less painful. Here’s proof of how well that strategy is working:

But none of this matters. DM central bankers are all-in on this; that is, there’s no turning back. Just as night follows day, the ECB will ease further which will lead directly to more easing from the Riksbank and the SNB. Similarly, the BoJ will likely end up attempting to further monopolize the Japanese ETF market and may ultimately move into individual stocks in an insane attempt to control corporate management teams and mandate the wage hikes that Abenomics has so far failed to produce.

That said, both the ECB and the BoJ are running out of monetizable assets which makes us and others wonder whether they will not become gun shy, having realized that they’ve finally bumped up against the limits of Keynesian insanity.

Whatever the case, just note that while Mario Draghi is quite adept at playing emotionless bureaucrat (unless a twenty-something is throwing glitter at him), it seems clear that DM central bankers are now beginning to question their own omnipotence and as Kuroda will tell you, “the moment you doubt whether you can fly, you cease to be able to do it forever.”

Wonderful choice of words. Classic understatements hiding chaos.

Probably not temporary & lacklustre global growth.

I keep mentioning this need for growth. It is a bankster thing.

In reality, when one borrows from them to start or run a business, they want you to borrow more & more because that is their source of income. Been there.

If you just make a steady, income paying, inflation matching & reinvesting needs profit, which is fine for most people, they want more, they call it growth, but in reality it is indebtedness.

Then they start offering tempting credit packages to encourage you to stretch yourself & get bigger, or grow.

Multiply that by the hundreds of thousands of businesses & you get the picture they want.

Growth is not necessary. Progression is not growth, and growth is not progress, it is indebtedness, and now they are in such a mess, even the businesses making profit still, would be most unwise to keep it in the banks now the law says that any deposits become the bankster’s property.

We need to do what Iceland has done.

Here’s more on the subject. Having deposits in the bank is undesirable….for the banksters. They make nothing out of it.

They make money from debt, which they pick from thin air & charge us for.

If we are in credit it’s no good for us any more.

So now they charge us for being in credit.

So keep it to a minimum.

Geriatric fool.

http://www.shtfplan.com/commodities/americans-face-impoverishing-war-on-cash-more-big-banks-are-shunning-cash_10312015

Like it said on the Economic Collapse Blog, it feels just like the lull before the storm.

Here’s another thought along the same lines, but encouraging community…..

http://www.alt-market.com/articles/2723-community-preparations-for-catastrophic-events