– The Perfect Solution To The Banking Crisis Is To Make A Truly Safe Bank:

We don’t need to up the FDIC limit, we need to eliminate the need for FDIC and create a safekeeping bank.

Creating a Safe Bank

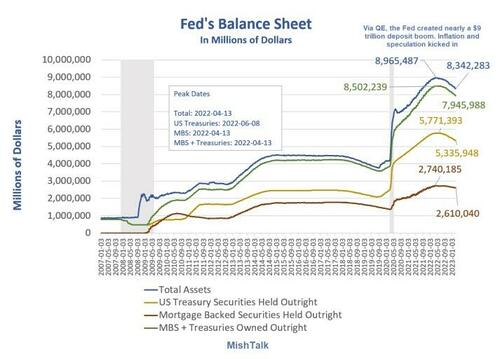

How many times do we have to go down the duration mismatch road with fractional reserve lending and nearly $9 trillion of Fed QE to prove the current banking doesn’t work?

Once again, systemic risk morphed into economic stress, bank failures, and then a bailout of the banking system, not just Silicon Valley Bank.

If you think only depositors got bailed out, you are mistaken. The Fed put a system backstop on $600 billion in bond losses. And although bank executives will lose their jobs, they cashed out tens of millions of dollars in stock options along the way.

Specifically, we need a bank that puts 100% of its assets in overnight treasuries and makes zero loans. The bank would not need any loan officers or many operational personnel for obvious reasons. There would be no need for FDIC guarantees because there would be zero risk of a run and zero risk of losses. We can still keep the FDIC term in place, but realistically it would not be needed. In essence, we would create a 100% reserve bank.

Such a bank might pay one percentage point less than the Fed ‘s overnight rate for safekeeping. If the overnight rate fell below 1 percent, the bank would charge a fee for safekeeping. The bank could also do term deposits at a slight discount to corresponding treasury yields. Depositors would be required to hold assets to term.

To prevent runs on existing banks right, we would let every bank participate in this offering. Customers would have a chance to place their deposits into safekeeping accounts at existing banks.

Bank Lending

To make loans, I propose banks would have to attract investment money instead of lending money into existence. They would do so by offering higher than market interest rates on term deposits, but those deposits would not be guaranteed.

As an added benefit, this setup would end fractional reserve lending. We would have a full reserve system, unfortunately one that is not backed by gold, but it would be a huge step in the right direction.

The immediate economic reaction would likely be contractionary, but that seems to be what the Fed wants now anyway to rein in inflation.

Alternatively, perhaps we could phase these ideas in over a 10-year period to mitigate risk.

Fed Should Admit Responsibility for Asset Bubbles

The Fed needs to admit it is largely responsible for these recurring bailouts.

Via QE, the Fed stuffed cash nearly $9 trillion in deposits down the throats of banks and that is why deposits soared so much in the first place.

Then despite the obvious risks, regulators eliminated all reserves on deposits and treasuries encouraging Silicon Valley Bank and other banks to seek yield.

It’s true that there were three rounds of fiscal stimulus, and the last one under President Biden was totally unwarranted as well as highly inflationary. But it’s the Fed’s job to understand that risk.

Unfortunately, the Fed not only sponsored the biggest asset bubble in history, it also failed to understand how free money, student debt cancellations, and zero percent interest rates might cause inflation.

Why Is There a Fed?

If the Fed cannot see the obvious, why is there a Fed? The only answer I can come up with is Congress would be worse.

The Fed aside, there is only one way to truly eliminate borrow-short, lend-long risk, and that is to go to a full reserve system where loans are not borrowed into existence and businesses and banks can have a bank where it is 100% certain their deposits will not be lent.

Admittedly, this could cause some short-term pain. Perhaps it would be the end of 30-year mortgages. But it would also serve to end financial speculation due to cheap money. And, as I suggested, perhaps there is a way to phase this in.

Why the Fed Doesn’t Want Full Reserve Bank

In the span of 20+ years, the Fed has blown three economic bubbles and we have had multiple bank bailouts.

The Fed does not want a full reserve bank because it wants inflation.

Inflation benefits those with first access to money. Banks, the already wealthy, and governments via tax collections are first in line.

Now that the Fed has created inflation, it doesn’t want that much of the tiger it unleashed.

Central Bank Digital Currencies

Another reason the Fed does not want a safe bank is so that it can sponsor its own digital currency.

Instead of sound money or merely sounder money, the Fed wants to be free to blow bubbles to fix the messes it creates while not understanding what inflation even is.

Those who believe the CPI or its PCE cousin measures inflation are wrong. Neither measure directly includes home prices or asset bubbles in general.

And we have proven once again that inflation and asset bubbles matter, not just alleged consumer inflation measures.

Serious change is needed. Instead, the Fed supports more of the same serial bubble-blowing measures, complete with bailouts and a charlatan digital currency savior on deck as its fake solution.