– Fed Balance Sheet Explodes By $300BN As Bank Bailouts Lead To Record Discount Window Surge:

Earlier today we said that with Wall Street freaking out over the latest bank crisis, everyone’s attention would be focused on today’s weekly H.4.1 update from the Fed. And they weren’t disappointed because what we found was striking.

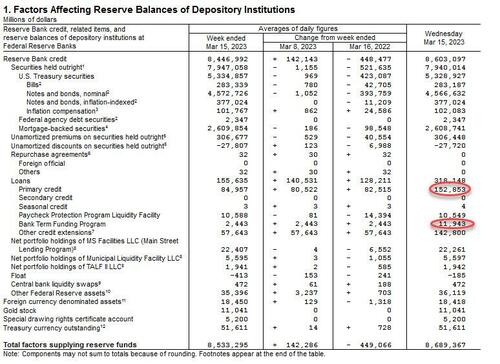

In the week ended March 15, borrowings under the Fed’s deeply stigmatizing last-ditch liquidity facility, the Discount Window, exploded to $152.85BN, a record $148BN weekly jump to an all-time high which surpassed even the borrowings during the financial crisis!

Just as importantly, those curious what the usage of the Fed’s new BTFP facility would be, got their answer – and the Fed won’t like it: at just $11.943BN, this was a very small amount as banks clearly fear the stigma associated with the BTFP program even more than they loathe the Discount Window. This is in line with what Goldman suggested: “While use of the BTFP is the most straightforward measure of the extent to which deposit outflows are putting banks under pressure, many banks say they will only use the BTFP once they have exhausted other funding sources such as FHLB advances, certificate of deposit issuance, and the wholesale debt market.” Clearly many banks are staying away.

Of course, as discussed earlier, we won’t know the names of the banks that used the two facilities – due to their deeply stigmatizing nature – for the next two years.

Taken together, the credit extended through the two backstops showed a banking system that remains broken and is dealing with over $100BN in deposit migration in the wake of the failure of Silicon Valley Bank of California and Signature Bank of New York last week.

And then the Fed also revealed that $142.8 billion in reserves were released by “Other Credit Extensions” (this line item was $0 last week), and “includes loans that were extended to depository institutions established by the Federal Deposit Insurance Corporation (FDIC). The Federal Reserve Banks’ loans to these depository institutions are secured by collateral and the FDIC provides repayment guarantees.”

Including loans that were extended to depository institutions established by the Federal Deposit Insurance Corporation (FDIC). The Federal Reserve Banks’ loans to these depository institutions are secured by collateral and the FDIC provides repayment guarantees.

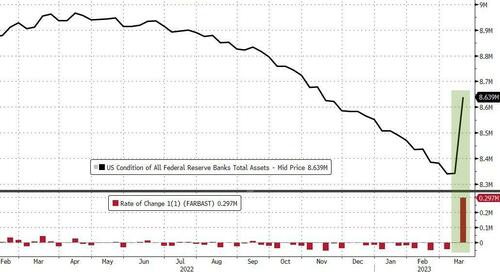

At the consolidated level, the surge in new liquidity created by the Fed meant that the Fed’s balance sheet rise by $297bn – its biggest jump since April 2020 and erasing 4 months of QT, or half of the entire program!

Separately, earlier today, we reported that JPMorgan’s Nick Panigirtzoglou estimated that the Fed’s new BTFP facility could rise as much as $2 trillion, and suggested that as a result of the massive reserves created by this facility it could serve as a Stealth QE. However, at $11BN per week, we will have to wait quite some time to get to JPM’s target.

Putting it together we said that we live in an interesting time: one when the Fed is hiking, the Fed is shrinking its balance sheet, and the Fed is also engaging in Stealth QE in hopes of injecting trillions in reserves in small banks.

What a time to be alive. The Fed is:

1. Hiking

2. Shrinking its balance sheet via QT

3. Injecting up to $2 TN in liquidity via BTFP which is "stealth QE" https://t.co/P01mcg5KT7— zerohedge (@zerohedge) March 16, 2023

Well, we can now say that for all intents and purposes, QT is over and as long as deposit flight continues, the Fed’s balance sheet will keep rising.