Blythe Masters is perhaps the most maligned human being on earth by silver investors due to suspicions of JP Morgan’s manipulation in the silver market. Well she’s back in the news, but it has nothing to do with silver. Rather, the news relates to the fact that her ex-husband and commodities traders, Daniel Masters, has just launched a Bitcoin hedge fund from the island of Jersey, a British Crown dependency.

“In retrospect we can understand why the inventor of the Credit Default Swap would only dare go out in public with a couple of armed gorillas covering her back.”

There is much new info in the just released Bloomberg profile on the infamous ex-JPMorganite Blythe Masters, among which the disclosure that she had made it clear that she had wanted to go along with the disposable JPM physical commodities unit (which as was reported recently, was sold to Swiss commodities giant Mercuria) and “and continue as the group’s chief”, a plan which did not work out as she had planned since she has no plans to “join the unit’s purchaser” (although joining Glencore is another matter entirely, and one which looks increasingly plausible) but what we find most striking is the following revelation: “Masters is under investigation by federal prosecutors in Manhattan, according to two people with knowledge of the matter. That probe was opened following a settlement with regulators that alleged JPMorgan manipulated power markets in the Midwest and California.”

Following our post yesterday which included the occasional F-bomb and got well over 40K reads since its posting late last night, the reaction was sharp and severe. So severe in fact that less than 24 hours later, Blythe Master has withdrawn from the CFTC. The culprit for Masters’ resignation in just 24 hours? A very angry Twitter.

Blythe Masters, JPMorgan Chase & Co.’s commodities head, withdrew from an advisory committee of the U.S. Commodity Futures Trading Commission a day after her appointment was disclosed, according to two people with direct knowledge of the decision.

We thought today’s newsflow and “market action” ranked pretty high on the absurd surrealism scale. And then we saw this.

BLYTHE MASTERS TO JOIN CFTC GLOBAL MARKETS COMMITTEE

JPMORGAN’S BLYTHE MASTERS TO JOIN CFTC ADVISORY COMMITTEE

CFTC SPOKESMAN COMMENTS ON BLYTHE MASTERS JOINING COMMITTEE

That’s right – you read it correct: “Blythe Masters, head of JPMorgan Chase & Co.’s commodities division, is joining an advisory committee of the U.S. Commodity Futures Trading Commission, said Steve Adamske, a spokesman for the regulator. Masters, 44, was invited by acting Chairman Mark Wetjen to sit on a global markets committee at the Washington-based regulator of futures and swaps, according to a person with knowledge of the matter. Masters is scheduled to participate in a CFTC meeting on Feb. 12 to discuss cross-border guidance on rules, the person said.”

It is somewhat ironic that none other than CNBC is reporting the news (which was suggested here months ago in “Will JPMorgan’s “Enron” Be The End Of Blythe Masters?”) that as part of its divestment of its physical commodities unit announced previously, JPMorgan may also seek to cover up any trace of market manipulation in the division recently embroiled in the aluminum cartel scandal (which we reported on in June 2011 and which story recently rose to prominence as a result of follow up reporting by the NYT) by getting rid of none other than Blythe Masters.

To wit: “JPMorgan’s initial round of conversations over the sale of its physical commodities unit has involved at least 50 potential suitors, according to someone familiar with the matter, as the bank attempts to ink a deal by the end of the year. In addition to energy supply contracts and metal-storage facilities, people close to the deal say the transaction could include a significant human asset: JPMorgan’s longtime commodities head, Blythe Masters. In addition to the physical assets it is selling—including the Liverpool, England-based metal-storage business Henry Bath & Son, U.S. power plants, and crude-oil and power supply agreements—any deal to sell JPMorgan’s commodities business could involve Masters, the division’s current leader, as well. Masters, 44, has found her future at JPMorgan in question as regulators crack down on both its power-supply business over alleged manipulations and the whole notion of banks owning commodities assets more generally.”

Ironic, because it was an extended CNBC interview-cum-PR campaign with Blythe Masters in April of 2012, just before the London Whale scandal broke, and one of her very rare media appearances, in which she made the following quite amusing, and factually wrong, in retrospect, statements:

One year after the infamous Jamie Dimon “tempest in a teapot” fiasco, which promptly turned out to be the biggest TBTF prop-trading desk debacle in history, things were going well for JPMorgan.

On one hand, the chairman of the TBAC (and thus US Treasury advisor and policy administrator), and former LTCM trader, Matt Zames, was just recently promoted to the sole second in command post at the biggest US bank (and 2nd biggest in the world) by assets, and first in line to take over from Jamie Dimon. On the other hand, one of Mary Jo White’s former co-workers, and a JPM defense attorney from Debevoise just became head of the SEC’s enforcement division, in theory guaranteeing that the US government would never do more than slap the wrist of JPM in perpetuity.

In this episode, Max Keiser and Stacy Herbert discuss a financial journalist so dangerous the frontpage of the Financial Times dare not speak his name and the semaphore of fraud and fraud flows that is high frequency trading and silver manipulation. They also talk about blonde bimbo regulators and the self-police force that never finds any evidence crimes they themselves have committed. In the second half of the show, Max Keiser talks to whistleblower Paul Moore, a former Head of Risk at HBOS, about financial holocaust and the City of London’s role in enabling banking fraud.

As readers enjoy JPM squirm his way through the JPM conference call (webcast live) explaining how it is that he not only was fooled by the CIO traders to the tune of billions, but more importantly to mismark hundreds of billions in CDS over the years, here is some delightful irony: “The J.P.Morgan Guide To Credit Derivatives” By Blythe Masters. Because it is truly ironic that the firm which created CDS will be the one responsible for destroying them.

Earlier today we listened with bemused fascination as Blythe Masters explained to CNBC how JPMorgan’s trading business is “about assisting clients in executing, managing, their risks and ensuring access to capital so they can make the kind of large long-term investments that are needed in the long run to expand the supply of commodities.” You know – provide liquidity. Like the High Freaks. We were even ready to believe it, especially when Blythe conveniently added that JPM has a “matched book” meaning no net prop exposure, since the opposite would indicate breach of the Volcker Rule. …And then we read this: “A JPMorgan Chase & Co. trader of derivatives linked to the financial health of corporations has amassed positions so large that he’s driving price moves in the multi-trillion dollar market, according to traders outside the firm.” Say what? A JPMorgan trader has a prop (not flow, not client, not non-discretionary) position so big it is moving the entire market? And we are talking hundreds of billions of CDS notional. But… that would mean everything Blythe said is one big lie… It would also mean that JPMorgan is blatantly and without any regard for legislation, ignoring the Volcker rule, which arrived in the aftermath of Merrill Lynch doing precisely this with various CDO and credit indexes, and “moving the market” only to blow itself up and cost taxpayers billions when the bets all LTCMed. But wait, it gets better: “In some cases, [the trader] is believed to have “broken” the index — Wall Street lingo for the market dysfunction that occurs when a price gap opens up between the index and its underlying constituents.” So JPMorgan is now privately accused of “breaking” the CDS Index market, courtesy of its second to none economy of scale and fear no reprisal for any and all actions, and in the process causing untold losses to, you guessed it, its clients, but when it comes to allegations of massive manipulation in the precious metals market, why Blythe will tell you it is all about “assisting clients in executing, managing, their risks.” Which client would that be – Lehman, or MFGlobal? Perhaps it is time for a follow up interview, Ms Masters to clarify some of these outstanding points?

The trader is London-based Bruno Iksil, according to five counterparts at hedge funds and rival banks who requested anonymity because they’re not authorized to discuss the transactions. He specializes in credit-derivative indexes, an off-exchange market that during the past decade has overtaken corporate bonds to become the biggest forum for investors betting on the likelihood of company defaults.

Investors complain that Iksil’s trades may be distorting prices, affecting bondholders who use the instruments to hedge hundreds of billions of dollars of fixed-income holdings. Analysts and economists also use the indexes to help gauge interest rates that companies must pay for new credit.

Though Iksil reveals little to other traders about his own positions, they say they’ve taken the opposite side of transactions and that his orders are the biggest they’ve encountered. Two hedge-fund traders said they have seen unusually large price swings when they were told by dealers that Iksil was in the market.

However, with that said, we are manipulating the silver futures market and playing a smaller (but still massively manipulative) role in manipulating the gold futures market. We have a little over a 25% (give or take a percentage) position in the short market for silver futures and by your definition this denotes a larger position than for speculative purposes or for hedging and is beyond the line of manipulation.

On a side note, I do not work directly with accounts that would have been directly impacted by the MF Global fiasco but I have heard through other colleagues that we have involvement in the hiding of client assets from MF Global. This is another fraudulent effort on our part and constitutes theft. I urge you to forward that part of the investigation on to the respective authorities.

In an article that is about three years overdue, “JPMorgan’s practices bring scrutiny” the FT finally takes aim at that other “vampire squid”, JP Morgan, which technically is incorrect: because if Goldman is a nimble and aggressive creature, with infinite tentacles in every governmental office, and unencumbered by massive liabilities, JPMorgan is just as connected, but unlike Goldman, it is a behemoth in every other possible capacity, and with its trillion in deposits, matched by tens of billions in bad loans, is a true Bank Holding Company. As such ‘Jabba the Hutt‘ would be a far more appropriate allegory to describe the the firm, whose reach, scope and scale lead the FT to classify it as “Three times a pallbearer, never a corpse.”

As some may recall, back in October 2009, Zero Hedge did an exhaustive expose on the relationship between JPMorgan and the then version of MF Global, Lehman Brothers, whose perfectly functioning division, its North American Brokerage, ended up being scooped up by Barclays for pennies on the dollar. In the meantime, however, JPMorgan, with the backing of the Fed, proceeded to demand as much extra collateral for Lehman repo positions on hold with JP Morgan and the Tri-Party repo system, of which JPM is one of only two custodians, simply because it could, and because this is the easiest way for the bank that is even closer to the Fed than Goldman Sachs, to procure liquidity during times of broad distress. Such as when the money market is about to freeze to death. Since then, the topic of just how much JPMorgan may have ripped off the Lehman estate has escalated, and is set to be an epic showdown in the form of a lawsuit which “accuses JPMorgan of using its “life and death power as the brokerage firm’s primary clearing bank” to put a “financial gun” to its head and demand excess collateral.” And here is the kicker: “It claims JPMorgan abused its access to US government officials and then “accelerated Lehman’s free fall into bankruptcy”, hoovering up collateral to protect itself to the detriment of the firm and other eventual creditors.”

And therein lies the rub: because of all TBTF banks, JPMorgan is literally at the nexus of the entire $16 trillion shadow banking system, the very system that the Fed, much more than traditional liabilities, knows and uses constantly to hypothecate and rehypothecate assets, in essence creating money out of nothing, and which in conjunction with the other Tri-Party repo dealer, Bank of New York, as well as State Street, provides the US financial system with over $30 trillion in shadow credit money in the form of custodial assets – liquidity the bulk of which is not accounted for in any conventional monetary textbook or in any modern theory of money as it is such a novel development, yet which is still 100% fungible, and is by far the biggest secret of the American monetary system. It can be seen as summarized in the following graphic, first created by Citi’s Matt King back in the week before Lehman failed (full report can be read here, and should be by anyone who wishes to understand just what is truly going on behind the scenes in modern finance).

Keep in mind, these are the same custody assets which, as explained previously in the case of MF Global, can be rehypothecated in serial fashion, creating a virtually infinite amount of “money” as long as everyone who is in on the fraud agrees to maintain the ponzi. Of course, if and when someone demands delivery of an underlying assets, the whole thing falls apart, which is what happened with AIG, with Lehman, and to a smaller degree, MF Global.

So what does all of this have to do with Blythe Masters?

Simple.

At the end of the day, and as the Lehman lawsuit alleges, JPMorgan has intimate access to US government officials, and particularly the Federal Reserve, who will in turn take advantage of all JPM facilities, including its trading desk, to preserve the sanctity and foundations of the $30+ trillion in custodial assets and rehypothecation system, which further means that any potential implication that fiat money is impaired has to be wiped out. As it so happens, soaring prices of gold and silver are the primary if not only means left to express rising doubts in the future viability of the dollar, but in the viability of the fiat system in the first place. Which means that the Fed is, without a doubt, one of the biggest “clients” of the Fed in a symbiotic crosshold, where what the Fed wants, JPM has to execute and vice versa.

This brings us to the transcript of Blythe’s interview on CNBC, in which a primary topic, ironically, was whether or not Jamie Dimon’s firm manipulates the prices of precious metals, and particularly silver. What followed was the usual avalanche of platitudes that only a muppet can love:

“JPM’s commodities business is not about betting on commodity prices but about assisting clients”… “it’s about assisting clients in executing, managing, their risks and ensuring access to capital so they can make the kind of large long-term investments that are needed in the long run to expand the supply of commodities”…

“There’s been a tremendous amount of speculation particularly in the blogosphere on this topic. I think the challenge is it represents a misunderstanding as the nature of our business. As i mentioned earlier, our business is a client-driven business where we execute on behalf of clients to achieve their financial and risk management objectives. The challenge is that commentators don’t see that. So to give you a specific example, we store significant amount of commodities, for example, silver, on behalf of customers we operate vaults in New York City, Singapore and in London. And often when customers have that metal stored in our facilities, they hedge it on a forward basis through JPMorgan who in turn hedges itself in the commodity markets. If you see only the hedges and our activity in the futures market, but you aren’t aware of the underlying client position that we’re hedging, that would suggest inaccurately that we’re running a large directional position. In fact that’s not the case at all.

“We have offsetting positions. We have no stake in whether prices rise or decline. Rather we’re running a flat or relatively flat matched book.

“What is commonly out there is that JPMorgan is manipulating the metals market. It’s not part of our business model. it would be wrong and we don’t do it.”

Ah yes, because JPMorgan never engages in “wrong” activites…

And while we admire JPM’s naive statement that it can triple its commodities revenues to $2.8 billion in 2011, while everyone else was losing money in the space, without taking prop bets, we just don’t buy it. Just as we didn’t buy Goldman’s explanation that its prop desk only accounted for 12% of that firm’s revenue, as Goldman told us directly (coupled with our challenge of prop trading in 2009, a pursuit taken on by Paul Volcker a few weeks later, resulting in the Volcker Rule). Needless to say, once the firm did break out its prop trading, it became quite clear just how huge of a factor prop trading truly was for Goldman. Because taken at face value, it would mean that all else equal, JPMorgan transacted at least 3 times more in flow in 2011 than in 2010. Yet, everyone knows that trading volumes in 2011 slumped relative to 2010. So no, Blythe, we appreciate your explanation, but we would appreciate the truth even more.

And yet there is one simple explanation that would make Blythe’s story 100% correct: would JPMorgan consider the Fed, whose interests in keeping the price of precious metals as low as possible, and are aligned with those of JPM for the reasons listed above, its client?

Because if so, then absolutely everything falls into place, as JPMorgan is merely the overt conduit by which the Fed, and specifically the New York Fed, conducts monetary policy in the commodities space, just as Brian Sack would conduct open market operations in the bond arena, and as the FRBNY uses, on occasion, Citadel, and its HFT expertise, to execute its discretionary stock trades (yes, we know about those too).

We would welcome Blythe’s comments on any and all of the topics listed above.

In the meantime, for those who missed it, here’s Blythe.

Each day this week, silver has been hammered down at approximately 9:00 am EST. Now, we all know that this isn’t atypical…the EE have been doing this for years and we did see copper sell off at roughly the same time. However, several readers have brought to my attention the little nugget below and I think it requires your serious consideration.

(Click on image to enlarge.)

First things first, here’s a 15-minute May silver chart to peruse. Keep in mind that today’s smackdown was in the face of ongoing strength in gold and crude, so, silver acted somewhat independently.

“WB: JPM is in worse shape then we ever dared to hope 20-Nov-10 07:06 am

Blythe,

This is what I am now hearing from traders on the floor. These traders are not even sure if Blythe knows the full extent of JPM’s silver exposure.

When I first started to realize that JPM has shorted far more silver than they could ever hope to cover, my first question was “why would they do that?” Not only that, why do it with a commodity where you must report your positions through the COT and Bank Participation Report? After all,the whole world can see what you are doing. [my added comment: Ted Butler included!]

Now I know the answer. According to Max Keiser and now a couple of other independent sources, it seems the reasons why first Bear Stearns and now JPM are so desperate to manipulate the price of silver down is due to the fact that BS and JPM shorted billions (yes billions not millions) in ounces of silver through their derivatives.

Just like Joe Conason at AIG, silver shorting through derivatives have caused literally billions in losses not the millions that we know about publicly. That is why JPM has been so desperate to manipulate the price of silver downward so blatantly. If I am right about this, then JPM will be dead when silver hits $60 or so. Based upon the COT and BPR, if silver hits $60, JPM will lose around an additional $6 billion dollars, a large number but not nearly large enough to bring down mighty JPM.

But what is not known is that due to the way that its derivatives are written, JPM’s losses are exponentional once silver breaks $36 or so. Rumors has it that JPM could be losing as much as $40 billion once silver is above $50. It has something to do with how the derivatives are written with payment tied to the price of silver.

Since JPM was a price manipulator with respectt to the price of silver, JPM assumed that any derivative payments tied to silver would be less than they would be tied to some other index like the CPI or TIPS implied inflation index. JPM’s inability to hold down the price of silver relative to other measures of inflation will cause unbelievable losses due to a mismatch in their derivative structures.

In essence,JPM has bet (a huge amount)through derivatives that silver will never outperform inflation. And why not,since JPM assumed that it will always be able to manipulate the price of silver. We have now come to understand that JPM’s loss exposure to silver is much greater than we have ever dared to hope. WB: In an effort to clear up some recent confusion regarding my latest posting, I will try to explain what I have recently uncovered.

JPM’s current short silver position is estimated to be approximately 150 million ounces down from the recent 180 million ounces in August. The losses from these positions are easy to figure out. For every $10 rise in the price of silver, JPM will lose $1.5 billion. But what I have recently discovered is that through its derivative positions, JPM will lose about 5 times that amount ounce the price of silver is above $36.And ounce silver is above $45 dollars, JPM’s losses will increase to 8 times the amount of losses in their short positions. The reason is that as the price of silver increases, certain provisions get activated which multiplies the losses.

While rumors that certain banks and exchanges may or may not be experiencing a dramatic run on physical silver are propagating across the blogosphere, we won’t know for sure until we see Blythe Masters resignation letter.

In the meantime Alexander Gloy of Lighthouse Investment reminds us of something very much indisputable: the physical premium over paper silver has just hit 20%, or an all time record.

In what can be only described as a total gutting of all silver shorts everywhere, including those with infinite Fed funded balance sheets (wink wink Blythe), all one can do is commiserate.

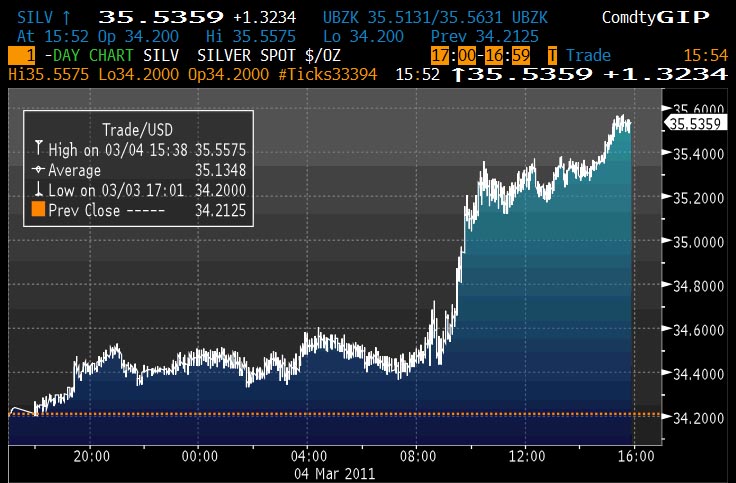

With silver hitting $35.55 intraday, not even a last ditch attempt to spread the ridiculous Chavez rumor once more (this time the two dictators will really get peace ironed out, we promise) will prevent a battery of margin calls from forcing all the silver market timers to liquidate assets to keep their primer brokers happy.

That’s ok: all those market timer will sooner, or much, much later, get the top right.

Submitted by Tyler Durden on 03/04/2011 15:56 -0500

Silver takes out $33.10, hitting a fresh 31 year high, as the relentless short squeeze leads to more body bags, and the only flight to safety currency is now the non-dilutable one (with gold on the verge of $1,400).

Only $20 more to go until the all time Hunt Brother record is smashed – one/two more revolutions should do it; even better: hopefully the CME hikes margins next week: that would bring $40 silver 24 hours later.

And on a more somber note, please join us for a moment of silence in remembrance of the great, the legendary, the soon to be departed Blythe Masters whose most recent zero margin, infinite PM short contraption has just sang its swan song.

Submitted by Tyler Durden on 02/20/2011 23:58 -0500

Blythe Masters invented credit default swaps, and is now heading JPM’s carbon trading efforts

As I have previously shown, speculative derivatives (especially credit default swaps or “CDS”) are a primary cause of the economic crisis. They were largely responsible for bringing down Bear Stearns, AIG (and see this), WaMu and other mammoth corporations.

According to top experts, risky derivatives were not only largely responsible for bringing down the American (and world) economy, but they still pose a substantial systemic risk:

Warren Buffett called them “weapons of mass destruction” in 2003

Warren Buffett’s sidekick Charles T. Munger, has called the CDS prohibition the best solution, and said “it isn’t as though the economic world didn’t function quite well without it, and it isn’t as though what has happened has been so wonderfully desirable that we should logically want more of it”

Former Federal Reserve Chairman Alan Greenspan – after being one of their biggest cheerleaders – now says CDS are dangerous

Former SEC chairman Christopher Cox said “The virtually unregulated over-the-counter market in credit-default swaps has played a significant role in the credit crisis”

Newsweek called CDS “The Monster that Ate Wall Street”

President Obama said in a June 17 speech on his plans for finance industry regulatory reform that credit swaps and other derivatives “have threatened the entire financial system”

George Soros says the market is still unsafe, and that credit- default swaps are “toxic” and “a very dangerous derivative” because it’s easier and potentially more profitable for investors to bet against companies using them than through so-called short sales.

U.S. Congresswoman Maxine Waters introduced a bill in July that tried to ban credit-default swaps because she said they permitted speculation responsible for bringing the financial system to its knees.

Nobel prize-winning economist Myron Scholes – who developed much of the pricing structure used in CDS – said that over-the-counter CDS are so dangerous that they should be “blown up or burned”, and we should start fresh

A leading credit default swap expert (Satyajit Das) says that the new credit default swap regulations not only won’t help stabilize the economy, they might actually help to destabilize it.

Senator Cantwell says that the new derivatives legislation is weaker than current regulation

Round Two: Carbon Derivatives

Now, Bloomberg notes that the carbon trading scheme will be largely centered around derivatives:

The banks are preparing to do with carbon what they’ve done before: design and market derivatives contracts that will help client companies hedge their price risk over the long term. They’re also ready to sell carbon-related financial products to outside investors.

[Blythe] Masters says banks must be allowed to lead the way if a mandatory carbon-trading system is going to help save the planet at the lowest possible cost. And derivatives related to carbon must be part of the mix, she says. Derivatives are securities whose value is derived from the value of an underlying commodity — in this case, CO2 and other greenhouse gases…

Who is Blythe Masters?

She is the JPMorgan employee who invented credit default swaps, and is now heading JPM’s carbon trading efforts. As Bloomberg notes (this and all remaining quotes are from the above-linked Bloomberg article):

Masters, 40, oversees the New York bank’s environmental businesses as the firm’s global head of commodities…

As a young London banker in the early 1990s, Masters was part of JPMorgan’s team developing ideas for transferring risk to third parties. She went on to manage credit risk for JPMorgan’s investment bank.

Among the credit derivatives that grew from the bank’s early efforts was the credit-default swap.

Some in congress are fighting against carbon derivatives:

“People are going to be cutting up carbon futures, and we’ll be in trouble,” says Maria Cantwell, a Democratic senator from Washington state. “You can’t stay ahead of the next tool they’re going to create.”

Cantwell, 51, proposed in November that U.S. state governments be given the right to ban unregulated financial products. “The derivatives market has done so much damage to our economy and is nothing more than a very-high-stakes casino — except that casinos have to abide by regulations,” she wrote in a press release…

However, Congress may cave in to industry pressure to let carbon derivatives trade over-the-counter:

The House cap-and-trade bill bans OTC derivatives, requiring that all carbon trading be done on exchanges…The bankers say such a ban would be a mistake…The banks and companies may get their way on carbon derivatives in separate legislation now being worked out in Congress…

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More https://infiniteunknown.net/dsgvo/

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

Premium To NAV Surges To Record High")

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}