See also:

– Is Deutsche Bank The Next Lehman? ( NotQuant, June 11, 2015):

Looking back at the Lehman Brothers collapse of 2008, it’s amazing how quickly it all happened. In hindsight there were a few early-warning signs, but the true scale of the disaster publicly unfolded only in the final moments before it became apparent that Lehman was doomed.

First, for purposes of drawing a parallel, let’s re-cap the events of 2007-2008:

There were few early indicators of Lehman’s plight. Insiders however, were well aware: In late 2007, Goldman Sachs placed a massive proprietary bet against Lehman which would be known internally as the “Big Short”. (It’s a bet that would later profit from during the crisis).

In the summer 2007 subprime loans were beginning to perform poorly in the marketplace. By August of 2007, the commercial paper market saw liquidity evaporating quickly and funding for all types of asset-backed security was drying up.

But still — even in late 2007, there was little public indication that Lehman was circling the drain.

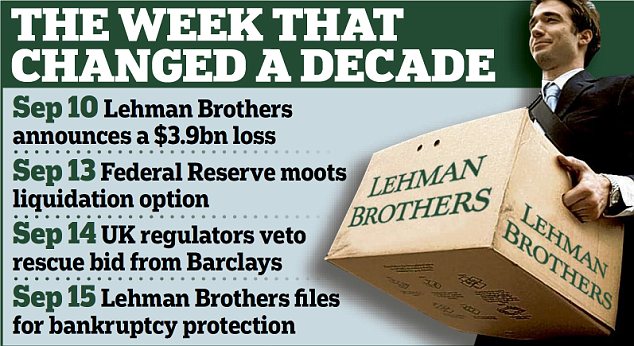

Probably the first public indication that things were heading downhill for Lehman wasn’t until June 9th, 2008, when Fitch Ratings cut Lehman’s rating to AA-minus, outlook negative. (ironically, 7 years to the day before S&P would cut DB)

The “negative outlook” indicates that another further downgrade is likely. In this particular case, it was the understatement of all time.

A mere 3 months later, in the course of just one week, Lehman would announce a major loss and file for bankruptcy.

And the rest is history.

Could this happen to Deutsche Bank?

First, we must state the obvious: If Deutsche Bank is the next Lehman, we will not know until events are moving at an uncontrollable and accelerating speed. The nature of all fractional-reserve banks — who are by definition bankrupt at all times – is to project an aura of stability until that illusion has already begun to implode.

By the time we are aware of a crisis – if one is in the offing — it will already be a roaring blaze by the time it is known publicly. It is by now well-established that truth is the first casualty of all banking crises. There will be little in the way of early warnings. To that end, we begin connecting the dots:

Here’s a re-cap of what’s happened at Deutsche Bank over the past 15 months:

- In April of 2014, Deutsche Bank was forced to raise an additional 1.5 Billion of Tier 1 capital to support it’s capital structure. Why?

- 1 month later in May of 2014, the scramble for liquidity continued as DB announced the selling of 8 billion euros worth of stock – at up to a 30% discount.Why again? It was a move which raised eyebrows across the financial media. The calm outward image of Deutsche Bank did not seem to reflect their rushed efforts to raise liquidity. Something was decidedly rotten behind the curtain.

- Fast forwarding to March of this year: Deutsche Bank fails the banking industry’s “stress tests” and is given a stern warning to shore up it’s capital structure.

- In April, Deutsche Bank confirms it’s agreement to a joint settlement with the US and UK regarding the manipulation of LIBOR. The bank is saddled with a massive $2.1 billion payment to the DOJ. (Still, a small fraction of their winnings from the crime).

- In May, one of Deutsche Bank’s CEOs, Anshu Jain is given an enormous amount of new authority by the board of directors. We guess that this is a “crisis move”. In times of crisis the power of the executive is often increased.

- June 5: Greece misses it’s payment to the IMF. The risk of default across all of it’s debt is now considered acute. This has massive implications for Deutsche Bank.

- June 6/7: (A Saturday/Sunday, and immediately following Greece’s missed payment to the IMF) Deutsche Bank’s two CEO’s announce their surprise departure from the company. (Just one month after Jain is given his new expanded powers). Anshu Jain will step down first at the end of June. Jürgen Fitschen will step down next May.

- June 9: S&P lowers the rating of Deutsche Bank to BBB+ Just three notches above “junk”. (Incidentally, BBB+ is even lower than Lehman’s downgrade – which preceded it’s collapse by just 3 months)

And that’s where we are now. How bad is it? We don’t know because we won’t be permitted to know. But these are not the moves of a healthy company.

How exposed is Deutsche Bank?

The trouble for Deutsche Bank is that it’s conventional retail banking operations are not a significant profit center. To maintain margins, Deutsche Bank has been forced into riskier asset classes than it’s peers.

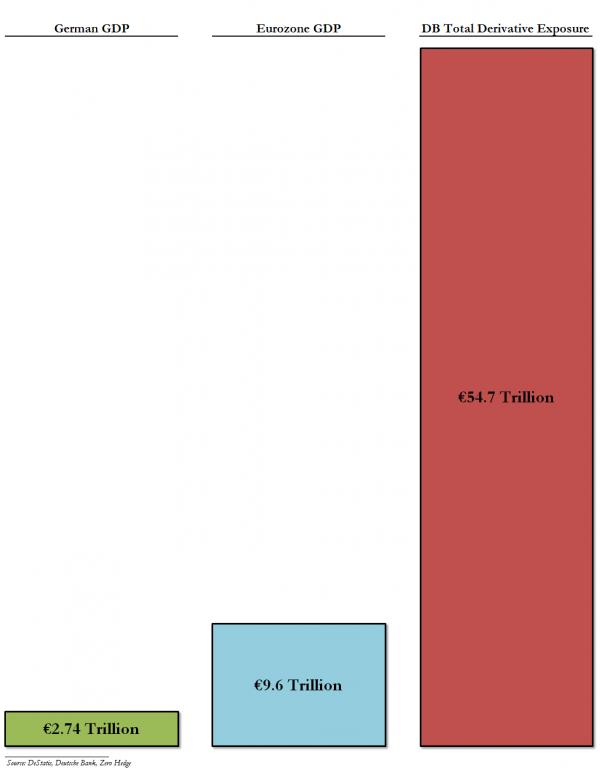

Deutsche Bank is sitting on more than $75 Trillion in derivatives bets — an amount that is twenty times greater than German GDP. Their derivatives exposure dwarfs even JP Morgan’s exposure – by a staggering $5 trillion.

With that kind of exposure, relatively small moves can precipitate catastrophic losses. Again, we must note that Greece just missed it’s payment to the IMF – and further defaults are most certainly not beyond the realm of possibility.

Not good.

And if the dominos were not adequately stacked already, there is one final domino which perfects the setup.

Meet Tom Humphrey. He heads up Deutsche Bank’s Investment Banking operations on Wall Street.

He was also head of fixed income at Lehman.

Prior history.History never repeats. But it does rhyme. In market terms, it tends to rhyme just about every 7 years.