Brilliant!!!

What could possibly go wrong?

In summary:

– George Carlin: The American Dream (Video)

– Hillary Clinton Is Grooming A Former Goldman Banker To Become America’s Next Treasury Secretary (ZeroHedge, April 17, 2015):

For years on end, many wondered how it is possible that Gary Gensler allowed Wall Street firms to manipulate, rig, and otherwise abuse the US commodity market which he, as head of the Commodity Futures Trading Commission from 2009 until 2014, was supposed to regulate.

Some, such as this website, suggested that what Gensler was doing was simply protecting his former colleagues from civil or criminal investigation and prosecution. After all Gensler is far better known for not only having worked at Goldman Sachs for 18 years most recently as co-head of finance, prior to joining the CFTC, but for becoming the youngest ever Goldman partner, at the tender age of 30.

Certainly, being the wealthiest member of the original Obama administration did not hurt: in 2009 the Wasingtonian reported his net assets as being between $15,533,000 and $61,745,000. We take the higher number. To be sure, he had been paid well at Goldman and now had a duty to his former employer: to keep Goldman (or any other Wall Street bank) off the hook of any regulatory investigation.

Overnight, this speculation was confirmed, and further explained why Gensler handled his former Wall Street colleagues with silk gloves: according to Bloomberg, “Hillary Clinton is planning to name Gary Gensler… as the chief financial officer of her campaign, according to a Democrat familiar with the decision.” And as hard as we try when reading the Bloomberg assertion that Gensler was “a strong advocate for strict Wall Street rules”, we can’t help but burst in laughter.

The humorous spin continues:

For Clinton, who has been fighting her left flank’s concern that she is too cozy with Wall Street, Gensler is a notable hire. He became known as someone with sharp elbows —even during his negotiations within the Obama administration—in his push for tighter regulation.

Actually, the only thing he became known for is avoiding any notable charges against any banks that involved more than a wrist slap, and certainly against Goldman: the same Goldman which alongside JPMorgan tried and almost succeeded to corner the physical aluminum (and countless other markets) and become a commodity cartel, a charge Wall Street’s banks are currently fighting in court.

But what is most amusing is how he fits in with the faux populism exhibited by Hillary. As Bloomberg notes “during her first visit to Iowa as a newly minted presidential candidate on April 14, Clinton struck a populist tone, saying “there’s something wrong when hedge fund managers pay less in taxes than nurses or the truckers I saw on I-80,” a reference to her two-day roadtrip to the state from New York. “I think it’s fair to say that if you look across the country, the deck is stacked in favor of those already at the top,” the former secretary of state told a roundtable at Kirkwood Community College.”

It got so bad a member of the Hillary SuperPAC almost caused the entire staff of CNBC to burst out in laughter when she said that “Hillary is certainly making it clear that she is running as a champion for everyday Americans. People who are looking how to get by, get ahead, stay ahead.”

One may even be believe these lies until one sees just who Clinton’s biggest US-based backers have been during her career: “everyday Americans” indeed:

Suddenly it all falls into place: Wall Street’s banks paid Clinton handsomely so that, under the guise of endless populism, she would stack her staff with current and former Wall Street professionals, those who would never dare abuse the status quo in which Wall Street was, is and will remain at the very top in America’s social and financial oligarchy. In other words, more of the same.

Oddly, Bloomberg yet again tries to paint Gensler as a person “of the people“:

Though a former partner at Goldman Sachs Group Inc., Gensler became a champion for strict new Wall Street regulation and was viewed by financial reform advocates as one of their top allies throughout his time as chairman of the CFTC.

Actually no. Gensler was put in so that he would be a figurehead and to neutralize and undo all real attempts at change, those undertaken by his predecessor Brooksley Born, who was truly a focused on fixing America’s runaway derivatives doomsday machine until she was shut down by the “committee to save the world” of Summers, Rubin and Greenspan.

In his role at the agency, Gensler pushed hard for rules transforming one of the most lucrative parts of Wall Street before the crisis: derivatives, the products investor Warren Buffett famously labeled “financial weapons of mass destruction.’’ In frequent speeches, public and private meetings at the agency and testimony to Congress, he used his nearly five-year tenure in the job to seek dozens of rules reining in Wall Street’s control of the $700 trillion market. Wall Street bristled at Gensler’s efforts. Banks, hedge funds and other companies visited the agency thousands of times pushing changes to the regulations. When they didn’t get what they want, the industry’s top lobbying groups then sued the agency multiple times.

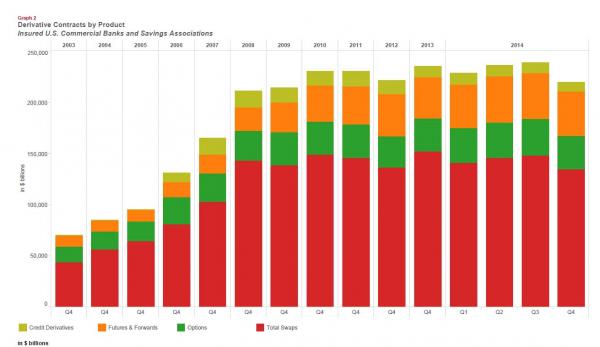

Really? Wall Street “bristled“? Well Bloomberg may be shocked to learn then that until last quarter, there was a record of $239.3 trillion held by FDIC-insured commercial banks and savings institutions, as in the most ever!

A more skeptical mind may conclude that Gensler’s “hard push” against Wall Street failed miserably and that all attempts to “rein in” the derivative market were met with epic disaster.

Of course, the reality is that Gary Gensler never even tried: he was siding with Wall Street all along. Because Bloomberg spin aside, here is the truth about Gary Gensler, from a 2011 Zero Hedge article:

Who was Gary Gensler?

When Gary Gensler was nominated to head the CFTC, most Americans had never heard of him. Yet he had been cruising the inner Beltway of D.C. and halls of influence for years under the radar of most. Genlser succeeded Brooksley Born who was given a very rough time by the club of Summers, Rubin, Greenspan et. al when she sounded the alarm bell on the rapid and unregulated growth of off-exchange derivatives. Born sought at least transparency as they “could pose potentially serious dangers to our economy.” Although appointed by Clinton, she never got his support and resigned from her post. For more on her prescient warnings, view this fascinating PBS documentary. As more collapses happen, the failure to regulate off exchange derivatives from CDO’s to re purchase agreements are increasingly understood to be a prime source of financial collapse.

Lobbying for Loopholes

Back to U-boat Gary. While still at Goldman Sachs brought Robert Rubin (yes, also from GS) recruited Gensler in 1997 to join him as Assistant Secretary for Financial Markets. Later he was promoted to Undersecretary for Domestic Finance in 1999. Here he worked on the changes to regulation assuring that credit default swaps and other off exchange derivatives were free from regulation. During the Enron disaster these were called “The Enron Loophole.”

In 2000 Congress passed the Commodity Futures Modernization Act, sponsored by Senator Phil Gramm (and John McCain’s campaign Economic Adviser). This act was written to keep off exchange derivatives unregulated and, as many are now discovering, opening “Mac Truck sized loopholes” allowing expanded access to customer funds for off exchange, but rated instruments beyond US Treasuries. Gary Gensler was the Treasury’s under secretary for domestic finance and it was his job to assure lobby that the CFMA got through Congress and signed into law.

Cheering the Confirmation

Gensler’s confirmation flew through Congress in 2009, but it was not cheered by all, especially the informed public. The New York Times named it “troubling” at the time and Salon came out with a damming article, “The Oligarch’s President.” Senator Tom Harkin, of the Agriculture Committee, at the time released a statement of “concerned about the de-regulatory orientation in this nominee’s past.” Senator Bernie Sanders tried to block it and was one of the two votes against Gensler with the strong statement:

… I cannot support his nomination. Mr. Gensler worked with Sen. Phil Gramm and Alan Greenspan to exempt credit default swaps from regulation, which led to the collapse of A.I.G. and has resulted in the largest taxpayer bailout in U.S. history. He supported Gramm-Leach-Bliley, which allowed banks like Citigroup to become “too big to fail.” He worked to deregulate electronic energy trading, which led to the downfall of Enron and the spike in energy prices. At this moment in our history, we need an independent leader who will help create a new culture in the financial marketplace and move us away from the greed, recklessness and illegal behavior which has caused so much harm to our economy.

Like Brooksley Born, Sander’s lone and prescient voice was ignored by the cheering mob in Congress. Gensler’s nomination was approved.

So how did a guy like this who was a key member of the Washington Beltway Demolition Derby get appointed as Chair of the CFTC? How did this happen after it was known that the loopholes Gensler had a hand creating and defending known loopholes in regulation that were pivotal to the mortgage banking collapse? Those things do not matter in Washington. Independence has no value.

Gensler served as senior economic adviser to the Hillary Clinton in the 2008 campaign. When her campaign closed shop, he jumped into the Obama camp as a fundraiser and adviser. Once elected, the Obama transition team then charged him with charge of the reviewing the SEC.

/p>

Prior to this Gensler was active in Democratic party politics, appointed treasurer of the Maryland Democratic Party in 2003. He emerged as a major donor contributing more than $220,000 to Democratic party candidates and committees from 2002. This figure includes the more than $72,000 in 2008 shortly before his appointment.

Washington D.C. is filled with souless hacks. Such men and women reduce themselves to be nothing more than instruments of others.

We saw that on display at the hearing this week called by the Agriculture Committee where Chairman Gensler was asked to testify. His prepared statement did not address the purpose of the hearing, but instead offered more about the Swaps market concluding with meaningless platitudes, “This is why the CFTC is working so hard to ensure that swaps-market reforms promote more open and transparent markets, lower costs for companies and their customers, and protect taxpayers. Thank you, and I would be happy to take questions.”

As questions were asked, more than once Gensler replied he could only speak only as allowed by his legal council…

Mr. Gensler talked much, but said little. On Monday, the CFTC will finally, and after much delay, vote on rule a required under the Dodd-Frank act removing a brokers’ ability to use their clients’ excess margin, or collateral for future trades, in corporate notes, bonds and commercial paper. The very changes to CFTC rule 1.25 that Gensler worked so hard to put in place 12 years before. The changes John Corzine and Laurie Ferber, MF Global’s general counsel, lobbied hard in recent months to protect and keep in place.

Expect Mr. Corzine to say nothing when he appears to answer to the American people. Such are the the government servants delivered to us.

Oh, yes, Jon Corzine. Almost forgot about him…

Why is all of this important? Because should Gary Gensler truly be Clinton’s chief financial officer, and should Hillary become America’s next president, then ladies and gentlemen, in the fine tradition started by Hank Paulson who nearly brought the entire wastern world to ruin, the next US Treasury Secretary will be the following fine former Goldman Sachs employee and “champion for everyday Americans.”

Neocons and Democons are both answering to the same master.

“If voting made any difference they wouldn’t let us do it.”Mark Twain

Flashback:

– Gary Gensler Explains How CFTC Allowed PFG To Steal $200 MM In Client Funds 8 Months After MF Global

– Gerald Celente On Eurozone Reckoning Day And Dropped Charges For Goldman Sachs! (Video)

* * *

– BiLDeRBiTCH…: