– China Stocks Crash, More Than Half Of Market Halted Limit Down; PBOC Loss Of Control Spooks Global Assets (ZeroHedge, Aug 18, 2015):

China sure has its micro-managing hands full these days.

Just hours after the PBOC announced a modestly “revalued” fixing in the CNY, which curiously led to weaker trading in the onshore Yuan for most of the day before a forceful last minute intervention by the central bank pushed it back down to 6.39…

USDCNY volumes getting a bit embarrassing now. pic.twitter.com/ai1hLnZpcL

— Gregor Stuart Hunter (@gregorhunter) August 18, 2015

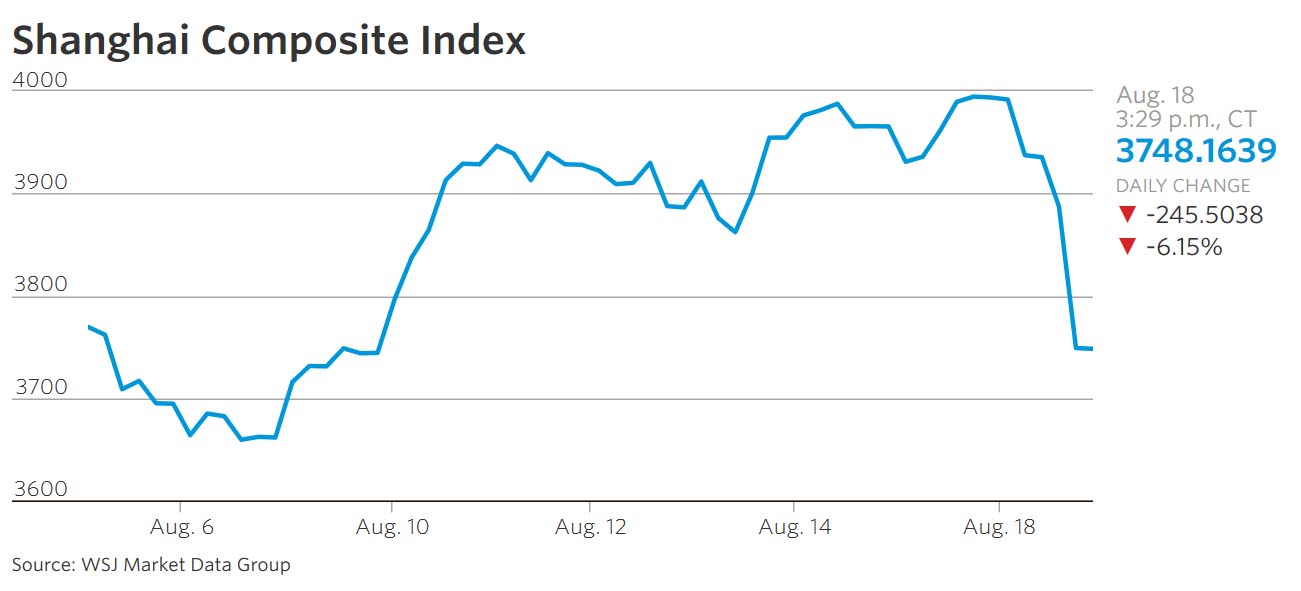

… it was the local stock market spinning plate – which had been relatively stable during the entire FX devaluation process – that China lost control over, and after 7 days of margin debt increases the Shanghai Composite plunged by 6.2% in late trade, tumbling 245 points to 3748, just 240 points above its recent trough on July 8, a closing level some 27% off its June peak. The smaller Shenzhen Composite Index fell 6.6% to 2174.42. This was the biggest single-day rout since July 27.

According to Reuters, “volatility in both indexes spiked in the afternoon in what is becoming a mysteriously recurring pattern in China’s stock markets since Beijing stepped in to avert a full-blown price crash in early summer.”

There were various reasons cited for the selling: one was that with Chinese housing data coming in stronger than expected, that Beijing may limit its future interventions to promote further easing of financial conditions and thus, supporting the market as we warned last night after the housing data came out:

CHINA JULY NEW HOME PRICES RISE M/M IN 31 CITIES; 27 IN JUNE. Not good: means less chance of RRR cut, PBOC buying every stock in perpetuitty

— zerohedge (@zerohedge) August 18, 2015

Another reason cited by Bloomberg is that stocks fells on “short-selling concerns.” BBG cited Central China Securities strategist Zhang Gang who said that “investors worry about potential aggressive short-selling activities after some brokers resume short-selling transactions, and this has hurt sentiment.”

Bloomberg adds that some speculative funds exited after gains in morning on fears that short-term speculative buying of SOE concept stocks may have come to an end.

According to the WSJ, “fresh anxieties about China’s commitment to steadying the stock market sparked heavy losses in Shanghai Tuesday, despite signals of a housing recovery and the central bank’s latest steps to keep cash from fleeing.” The heavy selling in the final minutes of trading echoed sessions in recent weeks, when faltering assurances of China’s role in the market hastened losses.

“At 2 p.m. it started to turn south again at a very fast rate,” said Steve Wang, a research director at Reorient Group. “People questioned why the government hadn’t yet stepped in” at a time of the day that it usually would, he added.

One can’t help but smile at this interpretation of what the “market” has become. Some who aren’t smiling, however, are those who once again decided to lever up with margin debt – as noted above, today was the 7th daily increase in retail investor leverage – only to lose all of it again just as we warned would happen yesterday. And now even the official party mouthpiece is starting to issue snarky announcements.

Wealth shrink! Investor accounts valued above 1-mln-yuan fell by 550k amid #China stock rout in June-July pic.twitter.com/cgfx47JoZY

— China Xinhua News (@XHNews) August 18, 2015

Losses among stocks of state-owned enterprises in Shanghai started building earlier in the morning amid skepticism about Beijing’s commitment to reform. Reports of efforts to accelerate reform, long touted as a way to open up bulky conglomerates to private investment and market forces, had gained momentum in recent weeks and buoyed related stocks.

The final damage: a total of 58% of stocks listed in Shanghai hit their downward daily limit of 10%, while 52% of all Shenzhen-listed shares met the same barrier, according to FactSet.

Here is a case study of what a government takeover of the stock market gone wrong looks like:

Take Guangdong Meiyan Jixiang Hydropower Co.: The state-run firm tasked to prop up the market, China Securities Finance Corp., is the biggest shareholder in the hydropower firm as of August 4, according to a company filing. CSF Corp.’s hefty role makes the company a “signature stock,” said Deng Wenyuan, an analyst at SooChow Securities.

When its shares fell by their 10% limit on Tuesday, it “may have sparked investors to resort to panic selling,” he said. The company’s shares had surged 150% as of Monday, 10 days after the stakeholder announcement.

Stocks that would benefit from reform of state-owned enterprises and those favored by CSF Corp. had been a driving force behind market rally since the June rout. “Both engines lost power today,” Mr. Deng added.

All this happened when neither measures to calm worries of capital flight given a weaker yuan nor positive economic data satiated investors.

Adding to liquidity and capital outflow fears, earlier China’s central bank injected the largest amount of cash into the financial system on a single-day basis in almost 19 months, signaling Beijing’s growing concerns about capital outflows after the yuan’s recent weakening. Reuters adds that “the central bank made its biggest injection of funds into money markets in more than six months early on Tuesday, adding to worries that liquidity was tightening as investors moved more capital out of the country. Minsheng Securities estimated 800 billion yuan ($125 billion) had flowed out in July and August alone.”

And while the currency was for the time stable as this is where all the PBOC firepower appears to be focused on these days, China also lost control of commodities: Copper dropped as much as 1.7% to $5,030/mt, lowest since 2009, before trading at $5,041. Aluminum also dropped as much as 1.2% to $1,549.50/mt, lowest in six years, before paring loss to $1,555.50. Nickel, zinc and lead decline at least 1.7%, and so on.

#Commodities – #Copper prices plunge towards psychological $5,000 per tonne level. YTD down 20% $GLEN$RIO$BHP$AALpic.twitter.com/80hLEvdjLt

— Javier Blas (@JavierBlas2) August 18, 2015

The return of the Chinese rout, which many thought had been “contained”, also spilled over to other global markets.

Asian equity markets fell, led by Shanghai Comp (-6.2%) as participants digested the latest property prices from China, which continued to show a recovery while the PBoC injected CNY 120bIn (most since February 9th) via open market operations, consequently disappointing growing calls of further easing, which comes alongside the resumption of short selling and margin financing by some large Chinese brokers. ASX 200 (-0.3%) and Nikkei 225 (-0.2%) were pressured by energy names as oil prices continued to slump. JGBs pulled off best levels on the back of a disappointing 20-year auction which posted a lower than prior b/c and a wider tail in price. Moody’s maintained China GDP growth forecast at 6.8% in 2015 and 6.5% in 2016, but sees growth declining to 6% in following years.

Stocks in Europe traded lower, as market participants continued to fret over the recent volatility in Chinese based financial instruments. As such European equities opened softer (Euro Stoxx: -0.20%), while energy names underperformed amid continued weakness in the commodity complex. Given the heavy commodity/energy sector weighting meant that the FTSE-100 index underperformed its EU peers.

Despite the weakness in equities, Bunds and Gilts failed to sustain the initial bid tone and pulled off the best levels following the release of firmer than expected UK CPI data. As a result, Gilts have underperformed Bunds, with the Short-Sterling curve aggressively bear steepening following the release.

In FX, GBP outperformed following the release of aforementioned firmer than expected UK CPI data, with the ONS noting that the latest increase was mainly due to clothing, with smaller price reductions in this years summer sales compared with a year ago.

Elsewhere, JPY gained from risk averse flows and also the growing uncertainty over the likelihood of a Fed rate hike, with China being seen as the main culprit for the delay, as opposed to Greece which was often noted in communiqué released by the Fed in the past.

In commodities, Commodities remained under pressure, with WTI trading near lowest level since March 2009, weighed on by the ongoing concerns over China and Iranian supply related risks. At the same time, aluminium and copper also continued to come under pressure and trade near their lowest levels since 2009.

Of note, it was reported that Kuwait Shuaiba oil refinery (Refinery has 200kbpd output) due to reopen within a few days after Monday’s closure due to a fire which had no effect on exports due to existing stockpiles.

In summary: European shares trade mixed, off earlier lows, with the tech and health care sectors outperforming and basic resources, oil & gas underperforming. Oil and copper drop, leading the Bloomberg Commodity index to a 13-year low. Sterling gains after U.K. core inflation rises to highest in 5 months. Asian stocks traded lower with Thai market underperforming after Bangkok bombing, baht reached weakest since 2009; Shanghai Composite fell 6.2% as yuan weakened in onshore trading. The Dutch and Spanish markets are the best-performing larger bourses, U.K. the worst. The euro is little changed against the dollar. Japanese 10yr bond yields fall; U.K. yields increase. Commodities decline, with zinc, copper underperforming and gold outperforming. U.S. housing starts, building permits due later.

Market Wrap

- S&P 500 futures down 0.3% to 2094

- Stoxx 600 little changed at 387.4

- US 10Yr yield down 1bps to 2.16%

- German 10Yr yield little changed at 0.63%

- MSCI Asia Pacific down 0.6% to 137.1

- Gold spot up 0.2% to $1120.4/oz

- Eurostoxx 50 -0.2%, FTSE 100 -0.5%, CAC 40 -0.4%, DAX -0.2%, IBEX little changed, FTSEMIB -0.2%, SMI -0.1%

- Asian stocks fall with the Sensex outperforming and the Shanghai Composite underperforming; MSCI Asia Pacific down 0.6% to 137.1

- Nikkei 225 down 0.3%, Hang Seng down 1.4%, Kospi down 0.6%, Shanghai Composite down 6.1%, ASX down 1.2%, Sensex down 0.1%

- Euro down 0.06% to $1.1071

- Dollar Index down 0.05% to 96.76

- Italian 10Yr yield up 1bps to 1.77%

- Spanish 10Yr yield up 1bps to 1.95%

- French 10Yr yield up 2bps to 0.96%

- S&P GSCI Index down 0.5% to 360.6

- Brent Futures down 0.4% to $48.6/bbl, WTI Futures down 0.4% to $41.7/bbl

- LME 3m Copper down 1.8% to $5020.5/MT

- LME 3m Nickel down 1.7% to $10440/MT

- Wheat futures down 0.1% to 503.8 USd/bu

Bulletin Headline Summary from RanSquawk and Bloomberg

- Stocks in Europe traded lower, as market participants continued to fret over the recent volatility in Chinese based financial instruments

- GBP outperformed following the release of aforementioned firmer than expected UK CPI data, with the ONS noting that the latest increase was mainly due to clothing

- Commodities remained under pressure, with WTI trading near lowest level since March 2009, weighed on by the ongoing concerns over China and Iranian supply related risks

- Treasuries steady, 10Y yield lowest since late May amid declines in currencies from Russia’s ruble to AUD and as a measure of EM stocks fell to four-year low.

- Shanghai Composite Index slid 6.2%, biggest loss since 8.5% rout on July 27; about 35 stocks fell for each that rose, while more than 600 companies plunged by the daily 10% daily limit

- In giving markets a greater say in setting the yuan’s level, Zhou Xiaochuan is bowing to Robert Mundell’s maxim that a country can’t maintain independent monetary policy, a fixed- exchange rate and free capital borders all at the same time

- Britain’s inflation rate rose 0.1% in July, more than forecast, and a core measure of price growth increased to the highest in five months

- Japan needs an economic injection of as much as JPY3.5t ($28b) to shore up consumption and stave off a further economic contraction, said Etsuro Honda, an economic adviser to Abe

- Merkel and Schaeuble will lobby lawmakers today to support the EU86b aid package for Greece, saying it offers a “sustainable path” even though the IMF has yet to commit to footing part of the bill

- Bob Corker (R-TN), the chairman of the Senate Foreign Relations Committee, said he opposes the nuclear agreement with Iran, arguing it won’t end the country’s nuclear enrichment program and may lead to greater instability in Middle East

- Deutsche Bank AG co-CEO John Cryan is overhauling the fixed- income division his predecessor built as he seeks to boost profit and capital

- Sovereign 10Y bond yields mixed. Asian stocks slid, European stocks lower, U.S. equity-index futures decline. Crude oil and copper lower, gold gains

US Event Calendar

- 8:30am: Housing Starts, July, est. 1.180m (prior 1.174m)

- Housing Starts m/m, July, est. 0.5% (prior 9.8%)

- Building Permits, July, est. 1.228m (prior 1.343m, revised 1.337m)

- Building Permits m/m, July, est. -8.2% (prior 7.4%, revised 7%)

DB’s Jim Reid concludes the overnight event wrap

We’re not going to lie to you this morning. This really isn’t the most interesting EMR we’ve ever published as the summer lull seemed to suddenly hit yesterday after so far having been delayed by Greece, Fed debate and more recently China. Having said that the commodity complex continues to be weak, the Malaysia ringgit continues to drift lower, US data yesterday was mixed and Greece still has ongoing internal political intrigue to watch. Today UK CPI and US housing starts/permits will be the main events. So that’s today’s EMR in a few lines and now to justify our existence we’ll flesh it out.

The overriding theme yesterday was the continued weakness in commodity markets and yesterday we saw Oil tumble with WTI (-1.48%) tumbling to a fresh six and a half year low at $41.87/bbl and Brent (-0.91%) falling to $48.74/bbl as China concerns, soft GDP data out of Japan and lingering supply-related headlines continue to weigh on the complex. The latest leg lower has seen WTI in particular fall over 11% already this month after a 21% decline in July. Although the falls dragged down energy stocks slightly yesterday, the S&P 500 started the week on a firming footing, closing up +0.52% and rebounding after sentiment was buoyed following the latest US housing data. European stocks were a tad more mixed. The Stoxx 600 (+0.26%) and CAC (+0.57%) both finished higher, however the DAX (-0.41%) was unable to recover from an earlier decline.

Overnight FX markets have been relatively calm for the most part after the PBoC effectively made little change to the Yuan fix this morning (within 0.03% of Monday’s close). The onshore Yuan has softened 0.26% while the more freely traded offshore Yuan is 0.06% weaker having initially strengthened. Asian FX markets continue to be under pressure this morning although the moves are certainly a lot more muted relative to the last week. The Malaysian Ringgit (-0.52%) however continues to be the standout underperformer, while the Korean Won, Indonesian Rupiah and Philippine Peso are also a tad lower this morning. There’s been little change in the Aussie Dollar meanwhile (hovering around $0.738) after the RBA minutes offered few surprises and continue to point towards no change in the current cash rate.

Meanwhile, July property prices data out of China this morning showed an improving trend after prices rose in more cities than declined for the first time in 16 months. According to the National Bureau of Statistics, new home prices rose in 31 cities last month (out of 70), versus 27 in June and 20 in May. That compares to new home price declines in 29 cities for July, while 10 cities saw prices unchanged. Despite the slightly improved housing market picture out of China, equity bourses there are leading declines although the bomb blast in Thailand overnight appears to be weighing on sentiment. The Shanghai Comp and Shenzhen are -1.46% and -1.20% respectively at the midday break, while the Thailand stock exchange has plummeted over 2%. The Nikkei (-0.16%), Kospi (-0.41%), Hang Seng (-0.08%) and ASX (-0.71%) have also declined this morning.

Back to markets yesterday. Once again the weakness in the commodity complex wasn’t just confined to Oil markets as Aluminum (-0.79%) and Copper (-0.97%) also declined over the session, bringing their YTD losses now to -15.4% and -18.8%. With that pressure and the read-through to dampening inflation expectations, US Treasuries caught a bid yesterday with the 10y benchmark yield in particular falling 3bps to 2.169%. That move lower was also helped by a particularly soft August NY Fed Empire manufacturing reading with the print falling 18.8pts to -14.9, the lowest level since April 2009. The details revealed that gauges of new orders, shipments and inventories in particular were significantly weaker in the month although there was some optimism to take out of the six-month ahead expectations reading which rose 7pts to 34.6. In any case, there’ll be plenty of attention on Thursday’s Philly Fed manufacturing survey in light of the weakness in NY Fed survey.

Despite US equities initially slumping on the back of the data, homebuilders led a rebound after the release of the NAHB housing market index for August showed a 1pt uplift to 61 as expected and in turn reaching the highest reading since November 2005. It’ll be interesting to see if the positive momentum around the US housing market continues today with housing starts and building permits due this afternoon. Despite the better housing data, the Oil related pressure saw Dec15 and Dec16 Fed Fund contract yields fall 0.5bps each, while the probability of a Fed move in September edged a touch lower to 46% from 48% on Friday.

There was very little to report over in the European session yesterday. Sovereign bond yields largely mirrored the moves in the Treasury market. 10y Bund yields closed the session 3.4bps lower at 0.624% while yields in Italy, Spain and Portugal finished 4.8bps, 7.0bps and 3.9bps lower respectively with Italy now falling to the lowest yield (1.757%) since May 8th. Data wise the only notable release was the June trade balance reading for the Euro area which showed a slightly smaller than expected surplus (€21.9bn vs. €23.1bn), up €0.6bn from May.

Elsewhere, it looks like the political tensions in Greece will continue to bubble away for now with Greek press Ekathimerini suggesting that Greece PM Tsipras and his advisers are set to hold off on an immediate call for a vote of confidence and instead focus in the coming weeks on the actions that the government must take as part of its bailout commitments. The article suggests that this could as a result push back any potential timing for snap elections before going on to quote a Greek government official as saying that an October/November time frame for snap elections might be more of a possibility. Meanwhile and staying in Greece, following on from German Chancellor Merkel’s comments on the weekend, German Finance Minister Schaeuble echoed Merkel’s comments regarding IMF participation, saying on German TV ZRD yesterday that ‘I’m also very sure that the IMF will contribute to the program, just as we declared this to be indispensible’. Schaeuble also called upon fellow lawmakers to approve the bailout package, saying that it offers a ‘sustainable path’.

Turning over to today’s calendar now, it’s all eyes on the UK this morning where we get the July CPI/RPI/PPI releases and which may well shed some more light for economists revising their BoE rate forecasts. Aside from that, there’s no other releases in Europe this morning while this afternoon in the US we’ve got July housing starts and building permits data to look forward to. DB’s Joe Lavorgna notes that he expects the housing starts reading in particular to continue to support the grinding improvement in the US housing market, but that building permits may well be slightly softer relative to June due to the possible payback for upward distortions in the Northeast region over the past few months.

The Chinese & Singapore markets sound like 1929………Unfortunately, the only money any of them are putting up has nothing behind it but ink…..China may be stock piling gold, but I don’t recall reading any of it is behind the Yuan.

Thanks to globalization, this infection will continue around the world……Hard to believe how many claimed China would pull us out of the malaise those of us in the west have suffered since 2009……It was all smoke and mirrors.