… as intended …

“When a country embarks on deficit financing (Obamanomics) and inflationism (Quantitative easing) you wipe out the middle class and wealth is transferred from the middle class and the poor to the rich.”

– Ron Paul

Mission accomplished!

… but it will get much, much worse … soon.

Prepare for the greatest financial collapse in world history.

– The Destabilizing Truth: Only The Wealthy Can Afford A Middle Class Lifestyle (OfTwoMinds, May 6, 2014):

By Charles Hugh Smith

The “middle class” has atrophied into the 10% of households just below the top 10%.

The truth is painfully obvious: a middle class lifestyle is unaffordable to all but the top 20%. This reality is destabilizing to the current arrangement, i.e. debt-based consumerism a.k.a. neofeudal state-cartel capitalism, so it is actively suppressed by the officially sanctioned narrative: that middle class status is attainable by almost every household with two earners (a mere $50,000 annual household income makes one middle class) and middle class wealth is increasing.

It’s not that difficult to define a middle class lifestyle: just list what was taken for granted in the postwar era of widespread prosperity circa the 1960s, four decades ago.

In What Does It Take To Be Middle Class? (December 5, 2013), I listed 10 basic “threshold” attributes and two somewhat higher thresholds for membership in the middle class:

1. Meaningful healthcare insurance (i.e. not phantom “insurance” with deductibles that cost thousands of dollars a year that offers no non-catastrophic care at all)

2. Significant equity (25%-50%) in a home

3. Income/expenses that enable the household to save at least 6% of its income

4. Significant retirement funds: 401Ks, IRAs, etc.

5. The ability to service all debt and expenses over the medium-term if one of the primary household wage-earners lose their job

6. Reliable vehicles for each wage-earner

7. The household does not rely on government transfers to maintain its lifestyle

8. Non-paper, non-real estate assets such as family heirlooms, precious metals, tools, etc. that can be transferred to the next generation, i.e. generational wealth

9. Ability to invest in offspring (education, extracurricular clubs/training, etc.)

10. Leisure time devoted to the maintenance of physical/spiritual/mental fitnessThe higher thresholds:

11. Continual accumulation of human and social capital (new skills, markets for one’s services, etc.)And the money shot:

12. Family ownership of income-producing assets such as rental properties, bonds, etc.The key point of these thresholds is that propping up a precarious illusion of consumption and status signifiers does not qualify as middle class. To qualify as middle class, the household must actually own/control wealth that won’t vanish if the investment bubble du jour pops, and won’t be wiped out by a layoff, college costs or a medical emergency.

In Chris Sullin’s phrase, “They should be focusing resources on the next generation and passing on Generational Wealth” as opposed to “keeping up appearances” via aspirational consumption financed with debt.

I then added up the real cost of these minimum thresholds and arrived at a minimum of $106,000 annual household income–double the median household income in the U.S. According to Census Bureau data, only the top 20% earn this level of income.

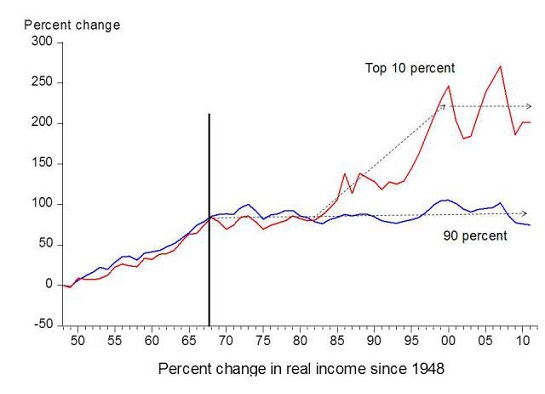

Here is a chart of the real income of the lower 90% and the top 10%, which by definition cannot be “middle class”:

The top 10% takes home 51% of all household income:

This suggests that the “middle class” has atrophied into the 10% of households just below the top 10%. Households in the “bottom 80%” are lacking essential attributes of a middle class lifestyle that were once affordable on a much more modest income.

Note that this $100,000+ household income has no budget for college costs, lavish vacations, boats, weekends spent skiing, etc., nor does it budget for luxury vehicles, SUVs, oversized pickup trucks or private schooling. Savings are modest, along with living expenses and retirement contributions. This is a barebones middle class budget.

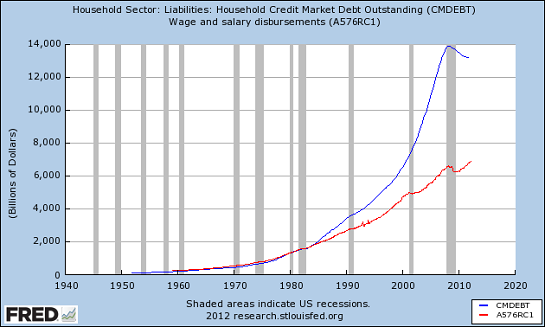

So how have we maintained an increasingly unaffordable lifestyle? With debt:Wages have risen modestly while debt has increased enormously.

As I have described many times, the Federal Reserve’s “solution” to the widening gap between income and expenses was to financialize the middle class’s primary asset: the home. I have explained this in depth: The Fed’s Solution to Income Stagnation: Make Everyone a Speculator (January 24, 2014)

Fed to the Sharks, Part 2: Housing and the Death of the Middle Class (April 9, 2014)

But turning everyone into a speculator via financialization had an unintended consequence: widening wealth inequality. It turns out most people are poor speculators, believing “this time it’s different” again and again. In addition, financialization favors those with the most capital: this is the essential take-away from Thomas Piketty’s book Capital in the Twenty-First Century.

The conclusion is inescapable: What’s the Primary Cause of Wealth Inequality? Financialization (March 24, 2014).

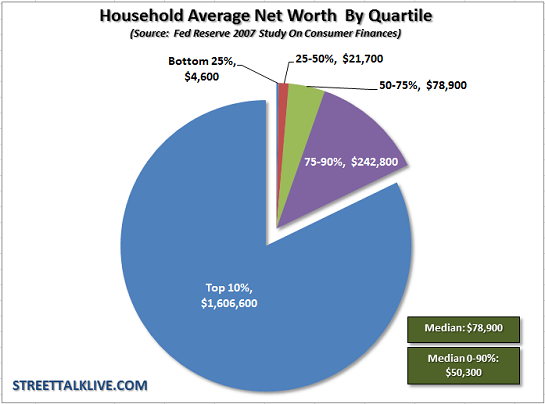

As a consequence, net worth (i.e. ownership of assets and wealth) of middle income households has been reduced to a sliver:

The widening wealth gap cannot be entirely explained away as the result of some innate force of capitalism; the rich have gotten richer as the direct result of central state/central bank policies introduced since the heyday of the middle class forty years ago.

So where does this leave us? To answer that, we need to examine the systemic causes of the higher costs and reliance on speculative bubbles that have eaten the middle class alive. We’ll address those tomorrow in Part 2.