– How low does this go before there’s a currency crisis? (Sovereign Man, March 11, 2014):

How’s this for irony –

In our modern monetary system, the term ‘fiat currency’ refers to this absurd notion of paper currency that is conjured out of thin air by central bankers and backed by nothing but hollow promises.

‘Fiat’ is a subjunctive conjugation of the Latin verb ‘fi?’; literally translated, it means “let it be” as in “Let there be light.”

Or in this case… ‘let there be paper money,’ which pretty much crystalized the absurdity of our monetary system.

Former Fed Chairman Ben Bernanke summed this up nicely in a 60 Minutes interview he gave a few years ago in which he said, “We can raise interest rates in 15 minutes. . .”

And he was right. Central bankers can change interest rates whenever they want.

If you think about it, interest rates are nothing more than the ‘price’ of money. It’s the rate that people pay when they ‘demand’ money in the form of loans based on the supply of money available.

But this price of money is incredibly influential around the world. Interest rates affect the prices of shares in the stock market. Oil. Agricultural commodities. Real estate. Automobiles.

Almost everything we touch is affected by interest rates.

So in setting the price of money, we have given central bankers the power to effectively set the price of… everything.

Make no mistake, this is a form of price controls. And there’s not a doubt in my mind that one day (probably soon), future historians are going to look back and wonder how so many people could be bamboozled.

We have somehow been conned into believing that the path to prosperity is for the grand wizards of the financial system to conjure paper currency out of thin air.

Yet this notion of ‘money backed by nothing’ is an absurd fantasy that has failed every single time it has ever been tried before in history.

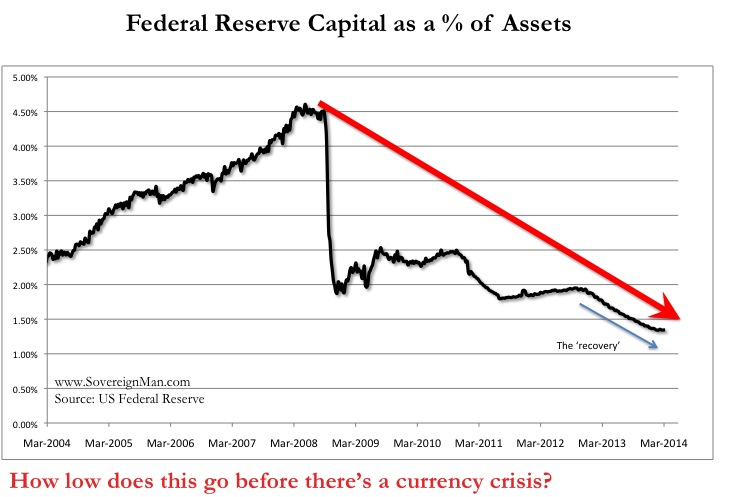

I bring this up because I want to share a chart with you that I presented yesterday to a savvy group of investors.

Bear in mind first that a central bank, like any bank or business, has both assets and liabilities.

Central bank assets are things like gold and government bonds (e.g. US government Treasuries).

Central bank liabilities are the ‘notes’ that they issue. And if you’re wondering what a central bank ‘note’ is, just look in your wallet.

If you’re in the US, those aren’t dollars. The dollar was defined by the Coinage Act of 1792 as 416 grains of standard silver.

Rather, you’ll see the paper in your pocket says “Federal Reserve Note”– a liability of the US central bank.

The difference between assets and liabilities is called equity, or the bank’s capital. And well-capitalized banks maintain substantial capital as a percentage of their assets.

You could think about this as a margin of safety. The less ‘capital cushion’ a bank has as a percentage of its assets, the less it will be able to withstand shocks to the system.

I tracked this data for the US Federal Reserve. And as the chart below shows, there has been an astounding decline in the Fed’s ‘margin of safety’ over the last few years.

The lower this line goes, the more the Fed gets pushed into insolvency.

Note that the trend levels out in early 2012, only to start another steep decline a few months later just as they told us the economy had ‘recovered’. This is apparently what recovery looks like.

The question I ask is: how low does this go before there’s a currency crisis?

When I studied economics, the ‘assets’ had to be represented by not less than 6% in Gold Bullion, as insurance for the said shock of a run or funding need such as conflict abroad.

This was called “The Fiduciary Issue” and led to confidence and stability.

After Reagan wedged Milton Friedman’s principles of a Corporate Free for All for every Nation’s assets, firmly into the system, and the Banks of the Western World were de-regulated (ie they were given carte blanche with no controls or responsibility) the doors were opened for opportunists who wormed their way into the world of unlimited money for the taking.

They changed the rules, rendering the humble depositor a classic victim of the quick buck syndrome.

By 2004, after milking the system for all it was worth, the spivs who now ran the ‘industry’ needed to create another source of easy con money. Hence the sub-prime con, which was neatly parcelled up in camouflage covered in chocolate, so the dumb greedy wannabee banksters round the world who hadn’t quite climbed on the bandwagon, would snap them up.

The spivs knew damned well it would fail, but that it wouldn’t show till after they got their money and ran.

The rest is history, except for the simple fact that had the principle of the Fiduciary Issue & the Regulations been in place, it couldn’t have happened.

Is it a mere coincidence that the names of all the people who benefited from that catastrophe were jewish?

Not all of the beneficiaries were Jewish…….but they have made a terrible mistake making themselves the target of hatred once again. After the fall of Nazi Germany, the banks were careful to keep them in the back rooms. That all vanished in the 1990s……they were hawking junk on all the financial channels, and stealing anyone’s money they could.

Why they keep doing this is one more example of human stupidity.

How they keep this lying cheating system going baffles me.

I was trying to find out some real information on interest rates after my research showed me the UK has a debt level of over 400% of GDP, along with most members of the EU suffering with at least 200% debt to GDP. The US is at 99%…..all disposable income is gone.

These thieves keep the rates low for the insiders, but for the consumer……that’s another story. I wonder when they will have to raise interest rates to get any money from real deposits………..how they keep it going makes no sense.

Once interest rates go up, all the indebted nations will really find out what pain is like……..and I just know it is around the corner. It is the last way to bleed the people……there are no more bubbles left.

85% of the stock market is skim and sell stealing….only 15% made up of actual investors. Of those, we don’t know how many are buying on margin.

One other comment. The US dollar is losing buying power dramatically in the grocery stores and fuel stations……the currency crisis is probably on now.