When the coming economic crisis strikes, more than half the country is going to be financially wiped out within weeks. At this point, more than 60 percent of all Americans are living paycheck to paycheck, and a whopping 24 percent of the country has more credit card debt than emergency savings. One of the primary principles that any of these “financial experts” that you see on television will teach you is to have a cushion to fall back on. At the very least, you never know when unexpected expenses like major car repairs or medical bills will come along.

And in the event of a major economic collapse, if you do not have any financial cushion at all you will be a sitting duck. Yes, I know that there are millions upon millions of families out there that are just trying to scrape by from month to month at this point. I hear from people that are deeply struggling in this economy all the time. So I don’t blame them for not being able to save lots of money. But if you are in a position to build up an emergency fund, you need to do so. We have been experiencing an extended period of relative economic stability, but it will not last. In fact, the time for getting prepared for the next great economic downturn is rapidly running out, and most Americans are not ready for it at all.

The following are 14 signs that most Americans are flat broke and totally unprepared for the coming economic crisis:

With the Federal Reserve printing trillions upon trillions of dollars to keep the economic system afloat, many investors and financial pundits have surmised that the fundamental economic problems facing the United States during the crash of 2008 have been resolved. Stocks are, after all, at historic highs.

But the insiders know different. And if there’s any single person out there who understands U.S. monetary policy and its long-term effects on domestic and global affairs it’s former Federal Reserve chairman Alan Greenspan. As the head of the world’s most powerful central bank for nearly two decades he’s privy to the insider conversations and government machinations that have brought us to where we are today.

“There are signs that underlying inflation has bottomed out, but the situation abroad is now more uncertain and this increases the risk that inflation will not rise sufficiently fast. The Executive Board of the Riksbank has therefore decided to cut the repo rate by 0.10 percentage points, to -0.10 per cent, and to adjust the repo-rate path down somewhat. At the same time, the interest rates on the fine-tuning transactions in the Riksbank’s operational framework for the implementation of monetary policy are being restored to the repo rate +/- 0.10 percentage point. Moreover, the Riksbank will buy government bonds for the sum of SEK 10 billion. These measures and the readiness to do more at short notice underline that the Riksbank’ is safeguarding the role of the inflation target as a nominal anchor for price setting and wage formation.”

With NIRP raging in the Eurozone and over €1.5 trillion in European government bonds trading with negative yields, many were wondering when any of this perverted bond generosity will spill over to other debtors, not just Europe’s insolvent governments (who can only print negative interest debt because of the ECB’s backstop that it will buy any piece of garbage for sale in the doomed monetary union). In fact just earlier today we, rhetorically, asked a logical – in as much as nothing is logical in the new normal – question:

Little did we know that just minutes after our tweet, we would learn that at least one place is already paying homeowners to take out a mortgage. That’s right – the negative rate mortgage is now a reality.

Thanks of Mario Draghi’s generosity with “other generations’ slavery”, and following 3 consecutive rate cuts by the Danish Central Bank, a local bank – Nordea Credit – is now offering a mortgage with a negative interest rate! This means, according to DR.dk, that Nordea have had to pay instead of charging interest to to a handful of customers, says housing economist at Nordea Kredit, Lise Nytoft Bergmann for Finance.

“People say, ‘Sell government bonds and lend money to widget manufacturers.’ It doesn’t really work like that.” Hayes says, adding that “Low yields don’t necessarily mean more lending to the real economy; time and confidence are key elements and last 6 years have shown QE can’t control those.” In short: it hasn’t even started and QE is already a complete failure. Good job central-planners.

Draghi’s answer is simple: we have now thrown the kitchen sink at the deflation problem and there has been no inflation (he conveniently forgets to mention that the world is now caught in a vicious spiral in which every single central bank is printing money just to export deflation to its peers, with more and more printing necessary each year just to stay in one place). In other words, just because hyperinflation hasn’t materialized so far, it never will.

Or, as Bernanke would say: “Hyperinflation is contained.”

Given that already surging money supply growth rates in the euro area are now bound to increase at an even stronger rate, economic activity as measured by aggregate statistics is bound to pick up eventually. It is always important to keep in mind though that quantitatively measurable “activity” as such is not telling us anything about its quality. The boom prior to the 2008 crisis was also characterized by a measurable increase in “activity”, but as it turned out, most of it was merely a complete waste of scarce capital.

There is no reason to assume that this time will be different. These boom-bust sequences will continue until the economy is structurally undermined to such an extent that monetary intervention cannot even create the illusory prosperity of a capital-consuming boom anymore.

The bankers applauding Draghi’s actions today will come to rue them tomorrow.

*DRAGHI SAYS TODAY’S MEASURES WILL BOLSTER INFLATION

*DRAGHI CITES SIGNALING EFFECT ON INFLATION EXPECTATIONS

Signal This!!

“Different this time?” or “Einsteinian Insanity”?

With The ECB set to announce a QE4EVA-esque bond-buying initiative within the next hour or two, we thought it worth looking at just what The Fed’s balance-sheet experiment did for inflation expectations (the key narrative that is driving Draghi’s decision) and economic growth (what every politician is demanding Draghi help with)…

From “whatever it takes” to OMT to “discussing” bond purchases, with European interest rates at record (incomprehensible) lows (apart from Greece) and EURUSD at 11-year lows (down 25 handles in the last 8 months), Mario Draghi looks set to unleash interventionist ‘hell’ on the investing public in Europe with EUR50 billion (plus plus) of ECB QE per month for as long as it takes.

Priced-in?

And then there’s this:

*MERKEL SAYS DEBT CRISIS ‘MORE OR LESS UNDER CONTROL,’ NOT OVER

*MERKEL SAYS ECB IS MAKING AN INDEPENDENT DECISION TODAY

Live Feed below (in case of error, here is a link to the source webcast):

And so with less than 24 hours to go, the ECB has decided to leak its deliberations not only to Merkel and Hollande, but Dow Jones. To wit:

DJ: ECB EXEC BOARD’S QE PROPOSAL CALLS FOR ROUGHLY EUR50B IN BOND BUYS A MONTH – SOURCES ECB SAID TO PROPOSE QE OF 50 BILLION EUROS A MONTH THROUGH 2016

More as we see it, but if indeed this will be a program without risk-mutualization and conditional and limited burden-sharing, where the hope was that Draghi would “shock and awe” the world with the size of the bond purchasing program instead, €600 billion per year looks decidedly on the low side of any “surprise” announcement where the whisper number was for €1 trillion per year, and if indeed this is the final formulation may result in a substantial disappointment for stocks after the initial kneejerk reaction.

“This last 1900 point Dow Jones push upwards – and the Ebola events leading into it – it was so orchestrated and heightened at critical points but the ascent and push straight up in price, and sideways nonreaction after was completely unlike anything I’ve seen before. After going up for a record-breaking amount of time the last five or so years, in a nonlinear exponential mania type of ascent, there should normally be tremendous volatility that follows… After this year and especially this last 1900 point Dow run up in October, and post non-reaction, that I am 100 percent confident that that one buyer is our own Federal Reserve or other central banks with a goal to “stimulate” our economy by directly buying stock index futures.”

…

American Epidemic? NYPD cop shoots dead unarmed man ‘without warning’:

The global financial system has come unglued. Everywhere the real world evidence points to cooling growth, faltering investment, slowing trade, vast excess industrial capacity, peak private debt, public fiscal exhaustion, currency wars, intensified politico-military conflict and an unprecedented disconnect between debt-saturated real economies and irrationally exuberant financial markets.

Yet overnight two central banks promised what amounts to more monetary heroin and, presto, the S&P 500 index jerked up to 2070. That is, the robo-traders inflated the PE multiple for S&P’s basket of US-based global companies to a nose bleed 20X their reported LTM earnings.

I’ve long written about how the percentage of sociopaths within a group of humans becomes increasingly concentrated the higher you climb within the positions of power in a society, with it being most chronic amongst those who crave political power (see: Humanity is Rising).

The security services are facing questions over the cover-up of a Westminster paedophile ring as it emerged that files relating to official requests for media blackouts in the early 1980s were destroyed.

Two newspaper executives have told the Observer that their publications were issued with D-notices – warnings not to publish intelligence that might damage national security – when they sought to report on allegations of a powerful group of men engaging in child sex abuse in 1984. One executive said he had been accosted in his office by 15 uniformed and two non-uniformed police over a dossier on Westminster paedophiles passed to him by the former Labour cabinet minister Barbara Castle.

Ah, national security. Remember that the next time you are lectured that we need to give up our civil liberties in the name of “national security.” Think about what that really means. It really means the security of the status quo to continue to behave like insane criminals with zero accountability.

It is unclear whether the person in charge of the Lois Lerner “disappeared IRS emails” strategy was also Dr. Gruber, but whoever conceived of the idiotic idea that the fatal failure of a local hard disk means that emails which are stored on at least one server miles away, and subsequently downloaded via POP3, IMAP or some other protocol, have vaporized, clearly also relied on the stupidity (and laziness) of the American people. And like in the case of Obamacare, the lies worked, if only for a short period of time. And because when it comes to lies coming from the very top, there is never just one cockroach, and they always inevitably scatter, the latest headache for a scandal-ridden president is that Lois Lerner’s email, supposedly gone in perpetuity, have mysteriously reappeared, and as the Washington Examiner reports, “up to 30,000 missing emails sent by former Internal Revenue Service official Lois Lerner have been recovered by the IRS inspector general, five months after they were deemed lost forever.”

In the wake of the failure of the U.S. Senate to move forward on the USA Freedom Act, many activists and civil liberties advocates have come to the conclusion that we can’t rely on the feds to do anything decent on the subject. One of the proposed grassroots ways to fight back has been an emphasis on increased use of encryption (recall my pre-Snowden era post, Bitcoin and Kim Dotcom: Why it’s Time to “Encrypt Everything”). Another obvious solution is for people to revolt at the local level. It appears that the citizens of Utah are doing just that.

Lawmakers are considering a bill that would shut off the water spigot to the massive data center operated by the National Security Agency in Bluffdale, Utah.

I am a United Sates Army general, and I lost the Global War on Terrorism. It’s like Alcoholics Anonymous; step one is admitting you have a problem. Well, I have a problem. So do my peers. And thanks to our problem, now all of America has a problem, to wit: two lost campaigns and a war gone awry.

“The situation has become so bad… that a middle-aged investor, fearing that a local developer wouldn’t be able to make his promised interest payments, threatened to commit suicide in dramatic fashion last summer. After hearing similar stories of desperation, city officials reminded residents that it is illegal to jump off the tops of buildings.”

As The West shows its fortitude (and apparent philanthropy) with mere 32-degree Fahrenheit ice-bucket-challenges, Russian chemistry professor Yury Zhdanov goes 290-degrees better…

Nikolay Novosyolov, founder of a science popularization project, poured a bucket of liquid nitrogen, which temperature was minus 322 degrees Fahrenheit (minus 197 Celcuis), as part of the #IceBucketChallenge campaign, taking the world’s social media charity craze to a whole new level.

The ultimate goal of the anti-Russian sanctions imposed by some Western nations is to stir public protests and oust the government, Russian Foreign Minister Sergey Lavrov said.

“Western leaders publicly state that the sanctions must hurt [Russia’s] economy and stir up public protests. The West doesn’t want to change Russia’s policies. They want a regime change. Practically nobody denies that,” he told a leading think-tank in Moscow.

Lavrov said that the tensions between Russia and the West had been brewing for years before the Ukrainian crisis, adding that now the Europeans had decided to go for all-or-nothing and play chicken with Russia. But at least the positions have been made clear, Lavrov said.

German police used pepper spray and clashed with anti-EU protesters, who stormed and vandalized the new European Central Bank building, which is under construction now in central Frankfurt.

Calling themselves Blockupy, thousands of activists gathered in the city center on Saturday and marched to the goal of their protest, the new ECB office, which is to be inaugurated next March.

The cost of the new office is almost 1.3 billion euros and this fact has caused a lot of criticism while the policy of austerity is applied all over Europe.

“While our colleagues, friends and comrades in Southern Europe continue to rebel against the depletion and impoverishment policies of the Troika, the ECB moves into its new palace,” Blockupy website says. “Blockupy moves on to the road. We will make our own move to the new building and give back to the ECB the garbage – in and with many moving boxes – that should have been thrown into the dustbin of history: racist and sexist division, impoverishment, privatization of public funds and goods and wars to secure resources.”

The news this week of China’s largest corporate bankruptcy – Haixin Iron & Steel Group – amid crashing iron ore and steel prices was followed by analysts noting it “will be followed by others,” as the major flaw of producers of iron ore, the most traded commodity after oil, is they tend to be “over-bullish.” Distressed debt funds are starting to circle in preparation for what they expect to be a bloodbath as Bloomberg reports, bad debts in China are well underestimated because authorities persist in propping up weak companies and bailing out local investors, according to DAC Management, “we’ve yet to see it because if you look at corporate defaults, they keep getting covered by the government. At some point, they can’t cover every single one.” Most worryingly though, as KPMG points out, “when you see restructuring advisers getting hired by SOEs… you know it’s coming.”

Healthcare workers at Hope Assisted Living & Memory Care Center in Dacula, Georgia, whose identities have not been made known as of this writing, have informed Health Impact News that on November 7, 2014, five residents of the center received flu vaccinations, only to die one week later.

Temperatures will drop to 19F (-4C) in some areas of the country next week as winter arrives.

Temperatures on Sunday night are expected to plummet to 26F (-3C) in rural areas of Northern Scotland and there may be snow showers on the mountains and widespread frost.

The cooler temperatures will continue on Monday, with overnight temperatures in the North down to 30F (-1C).

Once a market leader among Western 24-hour news channels, CNN has now become infamous for its slipshod mislabeling of maps across the world. This week the network hit a new low, transforming a synagogue into a mosque.

Are you in better shape financially than you were last Thanksgiving? If so, you should consider yourself to be very fortunate because most Americans are not. As you chow down on turkey, stuffing and cranberry sauce this Thursday, please remember that there are millions of Americans that simply cannot afford to eat such a meal. According to a shocking new report that was just released by the National Center on Family Homelessness, the number of homeless children in the U.S. has reached a new all-time high of 2.5 million. And right now one out of every seven Americans rely on food banks to put food on the table. Yes, life is very good at the moment for Americans at the top end of the income spectrum. The stock market has been soaring and sales of homes worth at last a million dollars are up 16 percent so far this year. But most Americans live in a very different world. The percentage of Americans that are employed is about the same as it was during the depths of the last recession, the quality of our jobs continues to go down, the rate of homeownership in America has fallen for seven years in a row, and the cost of living is rising much faster than paychecks are. As a result, the middle class is smaller this Thanksgiving than it was last Thanksgiving, and most Americans have seen their standards of living go down over the past year.

In 2014, there are tens of millions of Americans that are anonymously leading lives of quiet desperation. They are desperately trying to hold on even though things just keep getting worse. For example, just consider the plight of 49-year-old Darrell Eberhardt. Once upon a time, his job in a Chevy factory paid him $18.50 an hour, but now he only makes $10.50 an hour and he knows that he probably would not be able to make as much in a new job if he decided to leave…

Koichi Hamada is a special adviser to prime minister Shinzo Abe and one of his closest confidants. That makes his comments, as The Telegraph reports, even more stunningly concerning. Focusing his attention on the fact that Japan must delay the 2nd stage of its planned consumption tax hike – for fear of derailing the ‘recovery’ – Hamada unwittingly, it seems, explains the terrible reality behind the so-called “godfather” of Abenomics’ perspective on the extreme monetary policy he has unleashed…

Select stunning quotes that everyone should ignore and just BTFPonziD in Japan…

AMARI: ABENOMICS HASN’T FAILED(so this was the expected outcome?) SUGA: INVENTORIES, WEATHER, CONSUMER MINDSET CAUSED GDP FALL (nothing to do with record-high misery-index induced by crushing the currency of an energy-import-dependent nation?)

Japanese GDP fell for the 2nd quarter in a row making it official – as we warned a month ago – that Japan has entered a triple-dip recession. Againstr hope-strewn expectations that the rebound from a sales-tax-driven slump would create a magical 2.2% (annualized) expansion, Japanese GDP slumped 1.6% in Q3 – missing by the most since March 2011. So no tax increase… and thus fiscal responsibility goes out the window. Abe dissolves government and bails on another failure? The initial kneejerk reaction sent USDJPY surging back over 117.00 (and NKY followed) but that has quickly reversed and NKY futures are 600 off their highs (and S&P futures are back to last Monday’s lows).

“Yet, our political-financial system has gone from the dysfunctional to the failed to the surreal. Speculation, once left to individuals and investors, is now federally sponsored, subsidized and institutionalized. When this sham finally buckles and the next shoe falls and rates do eventually rise, the stock market will tank, liquidity will die, and the broader economy will plunge into a worse Depression than before. We are not there yet because of these coordinated moves and the political force behind them. But we are on a precarious path to that inevitability. “

A funny thing happened on the way to the ‘end’ of the multi-trillion dollar bond buying program known as QE – the Fed chronicles. Aside from the shift to a globalization of QE via the European Central Bank (ECB) and Bank of Japan (BOJ) as I wrote about earlier, what lingers in the air of “post-taper” time is an absence of absence. For QE is not over. Instead, in the United States, the process has simply morphed from being predominantly executed by the Federal Reserve (Fed) to being executed by its major private bank members. Fed Chair, Janet Yellen, has failed to point this out in any of her speeches about the labor force, inflation, or inequality.

John Hussman is highly respected for his prodigious use of data and adherence to what it tells him about the state of the financial markets. His regular weekly market commentary is widely regarded as one of the best-researched, best-articulated publications available to money managers.

John’s public appearances are rare, so we’re especially grateful he made time to speak with us yesterday about the precarious state in which he sees global markets. Based on historical norms and averages, he calculates that the ZIRP and QE policies of the Fed and other world central banks have led to an overvaluation in the stock market where prices are 2 times higher than they should be:

“In the absence of the gold standard, there is no way to protect savings from confiscation through inflation. … This is the shabby secret of the welfare statists’ tirades against gold. Deficit spending is simply a scheme for the confiscation of wealth. Gold stands in the way of this insidious process. It stands as a protector of property rights. If one grasps this, one has no difficulty in understanding the statists’ antagonism toward the gold standard.” – Alan Greenspan

“By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.” – John Maynard Keynes

While it is remarkable that the same media organization that a week ago was fawning over the rotting carcass of Keynes’ disastrous economic legacy, can today issue a warning that “Japan Creates World’s Biggest Bond Bubble”, we have long since given up being surprised by things that make absolutely zero sense in the New Abnormal.

So here is William Pesek with a less than Keynesian view on why Banzainomics’ very own Kuroda-san will be regarded as either a genius or a madman in a decade. Spoiler alert: it won’t be “genius.”

This is the big problem with fiat currency – eventually the temptation to print more of it when you are in a jam becomes too powerful to resist. In a surprise move on Friday, the Bank of Japan dramatically increased the size of the quantitative easing program that it has been conducting. This sent Japanese stocks soaring and the Japanese yen plunging. The yen had already fallen by about 11 percent against the dollar over the last year before this announcement, and news of the BOJ’s surprise move caused the yen to collapse to a seven year low. Essentially what the Bank of Japan has done is declare a currency war. And as you will see below, in every currency war there are winners and there are losers. Let’s just hope that global financial markets do not get shredded in the crossfire.

Trying to “fix” a sclerotic, inefficient state-cartel economy by boosting inflation–the ultimate goal of Japan’s Monetary Pearl Harbor– is a self-liquidating path to destruction.

The Bank of Japan’s surprise expansion of financial stimulus strikes me as the monetary equivalent of Pearl Harbor –not in the sense of launching a pre-emptive war (though the move does raise the odds of a global currency war), but in the sense of a leadership pursuing a Grand Strategy to the point of self-destruction because they have no alternative within their intellectual and political framework.

“Holy smokes,” Janet Yellen must have barked last week when Japan stepped up to plug the liquidity hole left by the US Federal Reserve’s final taper trot to the zero finish line of Quantitative Easing 3. The gallant samurai Haruhiko Kuroda of Japan’s central bank announced that his grateful nation had accepted the gift of inflation from the generous American people, which will allow the island nation to fall on its wakizashi and exit the dream-world of industrial modernity it has struggled through for a scant 200 years.

It has been clear for a while now that the lunatics are running the asylum in Japan, so perhaps one shouldn’t be too surprised by what happened overnight. Bloomberg informs us that “Kuroda Jolts Markets With Assault on Deflation Mindset”.

The policy hasn’t worked so far, in fact, it demonstrably hasn’t worked in Japan in a quarter of a century. Therefore, according to the Keynesian mindset, we need more of it. Mr. Kuroda therefore delivered a surprise spiking of the punchbowl that immediately impoverished Japan’s consumers further by causing a sharp decline in the yen:

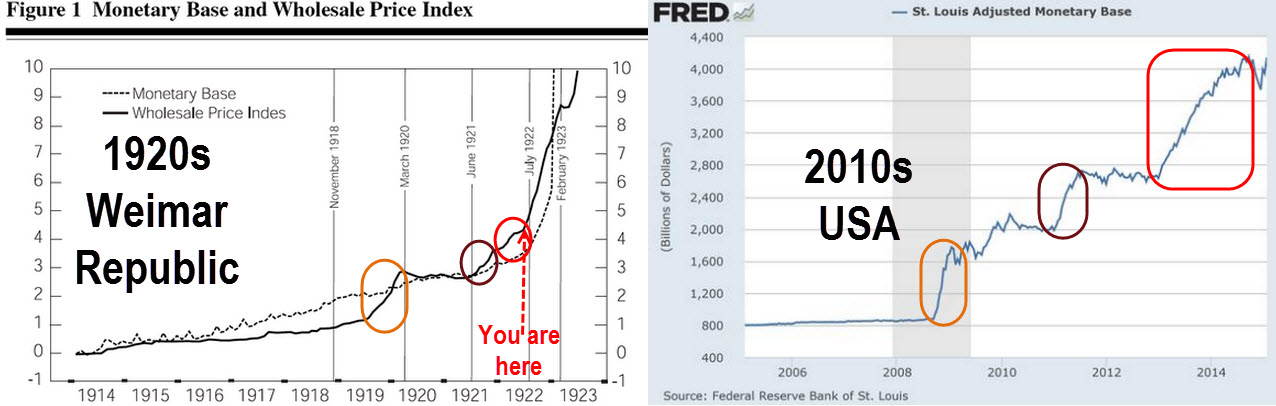

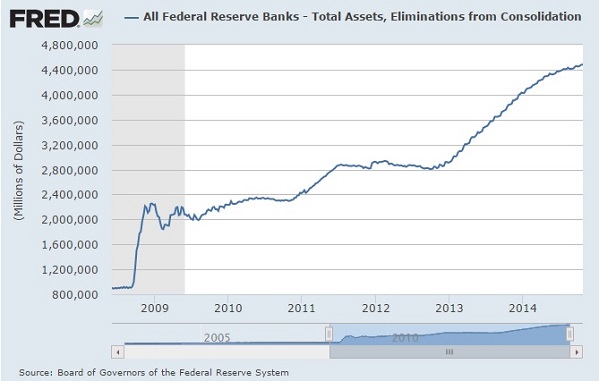

What has been expected for quite a while has now officially happened. The Federal Reserve stated that it would stop intervening on the market where it has been buying treasury bonds and mortgage-backed securities like there was no tomorrow anymore. The program started at a rate of $45B per month but was upscaled rather fast to $85B per month before being gradually scaled back since the beginning of this year. The Fed’s balance sheet has expanded considerably as you can see on the next chart.

Whereas the total balance sheet of the Fed was less than 1 trillion Dollars by the end of 2008, this has been increasing exponentially and in just the last 24 months the assets on the Fed’s balance sheet increased by 60% to 4.5 trillion dollars. Yellen has kept her promise as she said she’d scale the open-market purchases back if the economy would strengthen sooner than anticipated.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More https://infiniteunknown.net/dsgvo/

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.