– What Goes Up Also Comes Down: The Heavy Hand Of Bubble Symmetry:

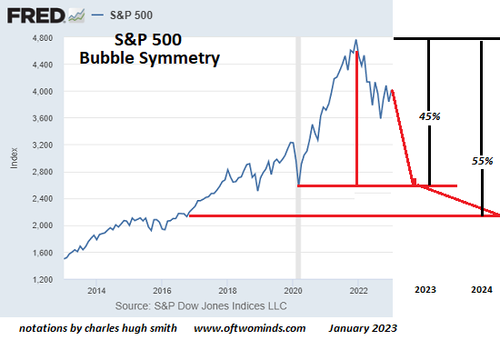

Should bubble symmetry play out in the S&P 500, we can anticipate a steep 45% drop to pre-bubble levels, followed by another leg down as the speculative frenzy is slowly extinguished.

Bubble symmetry is, well, interesting. The dot-com stock market bubble circa 1995-2003 offers a classic example of bubble symmetry, though there are many others as well. The key feature of bubble symmetry is the entire bubble retraces in roughly the same time frame as it took to soar to absurd heights.

Nobody could see bubble symmetry coming, of course. At the peak and for some time after, bubbles are viewed as the natural order of markets and so they should continue expanding forever.

Alas, the natural order of markets is mean reversion and the collapse of whatever is unsustainable. This includes speculative manias, credit bubbles, asset bubbles and projections of endless expansion of margins, profits, sales, consumption, tax revenues and everything else under the sun.

There’s a well-worn psychological path in the collapse of bubbles. This path more or less tracks the Kubler-Ross phases of denial, anger, bargaining, depression and acceptance, though the momentum of speculative frenzy demands extended displays of hubris and over-confidence, i.e. the first wobble “must be the bottom.”

There’s also repeated spikes of false hope that “the bottom is in” and the bubble is starting to reflate.

This pattern repeats until the speculative fever finally breaks and all those betting on a resumption of the bubble mania finally give up.

This process often takes about the same length of time that it took for the bubble mania to become ubiquitous. If it took about 2.5 years for the bubble to expand, it takes about 2.5 years for the bubble to pop and the market to return to its pre-bubble level.

Once again we hear reasonable-sounding claims being used to support predictions of a never-ending rise in stock valuations.

What hasn’t changed is humans are still running Wetware 1.0 which has default settings for extremes of emotion, particularly manic euphoria, running with the herd (a.k.a. FOMO, fear of missing out) and panic / fear.

Despite all the assurances to the contrary, all bubbles pop because they are based in human emotions. We attempt to rationalize them by invoking the real world, but the reality is speculative manias are manifestations of human emotions and the feedback of running in a herd of social animals.

With all this in mind, let’s consider the current bubbles in stocks and housing. Should bubble symmetry play out in the S&P 500, we can anticipate a steep 45% drop to pre-bubble levels, followed by another leg down as the speculative frenzy is slowly extinguished.

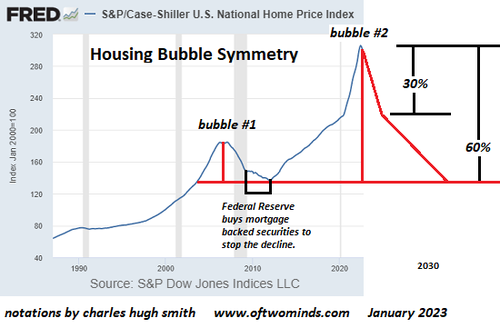

Housing is notoriously “sticky” when it comes to price declines, as sellers show remarkable tenacity in the denial phase. The last few greater fools buying on the first modest decline spur the hopes of sellers that the flood of mania-driven buyers is about to resume, but manias don’t last nor do they resume.

If bubble symmetry plays out, we can anticipate a relatively steep drop of about 30% to pre-mania levels, followed by a longer decline to pre-Bubble #1 and Bubble #2 levels, a roughly 60% drop from bubble heights.

Such declines are of course “impossible.” There are always endless reasons why bubbles can’t possibly pop and why 60% declines are impossible, even as history tells us that 60% declines are inevitable, and in the bigger picture, rather modest. It’s the 90% declines that really hurt.

***

* * *

PayPal: Donate in USD

PayPal: Donate in EUR

PayPal: Donate in GBP