“Of course, no amount of math and logic will ever be sufficient to convince a bunch of retired public employees that they have been sold a lie that will inevitably fail now or fail later (take your pick) if drastic measures aren’t taken in the very near future.”

– Teachers Demand $3,200 From Each Kentucky Household To Fund Pension Ponzi For 2 Years:

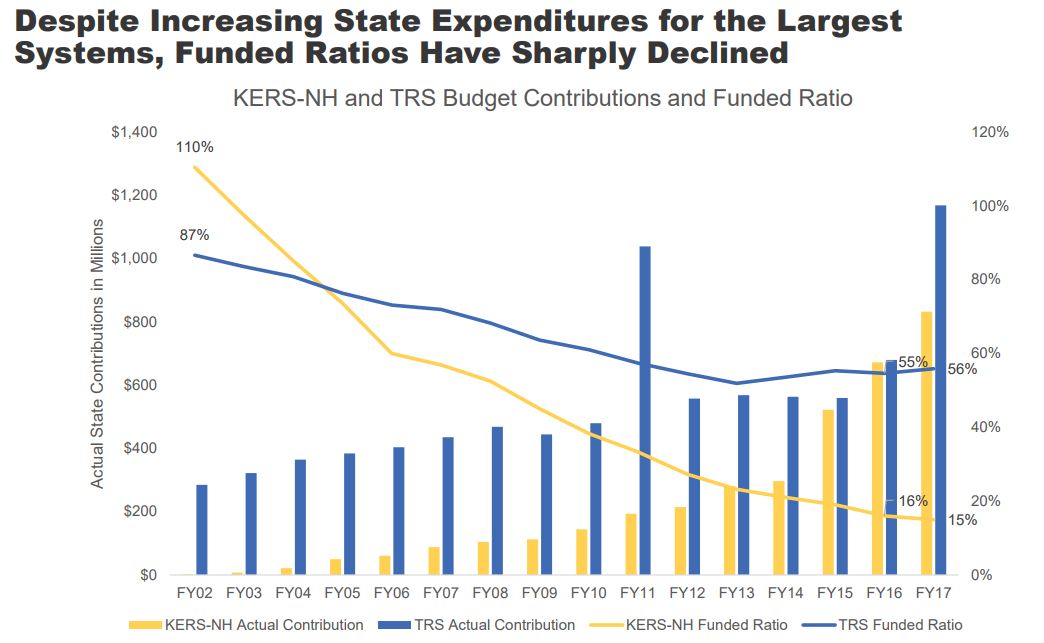

We have written frequently over the past couple of weeks about the disastrous public pension funds in Kentucky that are anywhere from $42 – $84 billion underfunded, depending on which discount rate you feel inclined to use. As we’ve argued before, these pensions, like the ones in Illinois and other states, are so hopelessly underfunded that they haven’t a prayer of ever again being made whole.

That said, logic and math have never before stopped pissed off teachers and/or clueless legislators from throwing good money after bad in an effort to ‘kick the can down the road’ on their pension crises. As such, it should come as no surprise at all that the Lexington Herald Leader reported today that Kentucky’s 365,000 teachers and other public employees are now demanding that taxpayers contribute a staggering $5.4 billion to their insolvent ponzi schemes over the next two years alone. To put that number in perspective, $5.4 billion is roughly $3,200 for each household in the state of Kentucky and 25% of the state’s entire budget over a two-year period.

Kentucky’s General Assembly will need to find an estimated $5.4 billion to fund the pension systems for state workers and school teachers in the next two-year state budget, officials told the Public Pension Oversight Board on Monday.

That amount would be a hefty funding increase and a painful squeeze for a state General Fund that — at about $20 billion over two years — also is expected to pay for education, prisons, social services and other state programs.

“We realize this challenge is in front of us. That’s obviously part of the need for us to address pension reform,” said state Sen. Joe Bowen, R-Owensboro, co-chairman of the oversight board.

“In the short-term, yeah, we’re obligated to find this money,” Bowen said. “And everybody is committed to do that. We have revealed this great challenge. We have embraced this great challenge, as opposed to previous members of the legislature, perhaps.”

In presentations on Monday, the pension oversight board was told that total employer contributions for KRS in Fiscal Years 2019 and 2020 would be an estimated $2.47 billion each year, up from $1.52 billion in the current fiscal year. Nearly $995 million of that would be owed by local governments. The remaining $1.48 billion is what the state would owe.

The Teachers’ Retirement System estimated that it would need a total of $1.22 billion in Fiscal Year 2019 and $1.22 billion in Fiscal Year 2020. That would include not only an additional $1 billion to pay down the system’s unfunded liabilities but also $139 million to continue paying the debt service on a pension bond that won’t be paid off until the year 2024.

Of course, the $5.4 billion will do absolutely nothing to avoid an inevitable failure of Kentucky’s pension system but what the hell…

As we’ve said before, the problem is that the aggregate underfunded liability of pensions in states like Kentucky have become so incredibly large that massive increases in annual contributions, courtesy of taxpayers, can’t possibly offset liability growth and annual payouts. All the while, the funding for these ever increasing annual contributions comes out of budgets for things like public schools even though the incremental funding has no shot of fixing a system that is hopelessly “too big to bail.”

So what can Kentucky do to solve their pension crisis? Well, as it turns out they hired a pension consultant, PFM Group, in May of last year to answer that exact question. Unfortunately, we suspect that PFM’s conclusions, which include freezing current pension plans, slashing benefit payments for current retirees and converting future employees to a 401(k), are somewhat less than palatable for both pensioners and elected officials who depend upon votes from public employee unions in order to keep their jobs…it’s a nice little circular ref that ensures that taxpayers will always lose in the fight to fix America’s broken pension system.

Be that as it may, here is a recap of PFM’s suggestions to Kentucky’s Public Pension Oversight Board courtesy of the Lexington Herald Leader:

An independent consultant recommended sweeping changes Monday to the pension systems that cover most of Kentucky’s public workers, creating the possibility that lawmakers will cut payments to existing retirees and force most current and future hires into 401(k)-style retirement plans.

If the legislature accepts the recommendations, it would effectively end the promise of a pension check for most of Kentucky’s future state and local government workers and freeze the pension benefits of most current state and local workers. All of those workers would then be shifted to a 401(k)-style investment plan that offers defined employer contributions rather than a defined retirement benefit.

PFM also recommended increasing the retirement age to 65 for most workers.

The 401 (k)-style plans would require a mandatory employee contribution of 3 percent of their salary and a guaranteed employer contribution of 2 percent of their salary. The state also would provide a 50 percent match on the next 6 percent of income contributed by the employee, bringing the state’s maximum contribution to 5 percent. The maximum total contribution from the employer and the employee would be 14 percent.

For those already retired, the consultant recommended taking away all cost of living benefits that state and local government retirees received between 1996 and 2012, a move that could significantly reduce the monthly checks that many retirees receive. For example, a government worker who retired in 2001 or before could see their benefit rolled back by 25 percent or more, PFM calculated.

The consultant also recommended eliminating the use of unused sick days and compensatory leave to increase pension benefits.

Meanwhile, PFM warned that the typical “kick the can down the road approach” would not work in Kentucky and that current retiree benefits would have to be cut.

“This is the time to act,” said Michael Nadol of PFM. “This is not the time to craft a solution that kicks the can down the road.”

“All of the unfunded liability that the commonwealth now faces is associated with folks that are already on board or already retired,” he said. “Modifying benefits for future hires only helps you stop the hole from getting deeper, it doesn’t help you climb up and out on to more solid footing going forward.”

Of course, no amount of math and logic will ever be sufficient to convince a bunch of retired public employees that they have been sold a lie that will inevitably fail now or fail later (take your pick) if drastic measures aren’t taken in the very near future.

* * *

PayPal: Donate in USD

PayPal: Donate in EUR

PayPal: Donate in GBP