– India’s Modi Admits Plan Shifting Nation To “Cashless Society”:

Well who could have seen this coming? Just as we noted, the slippery slope towards full government control in a cash-less society is where Indian PM Modi is heading following his chaos-creating demonetization efforts of the last two weeks. While massive opposition protests are planned tomorrow, Modi remains indignant, as Reuters reports, “we can gradually move from a less-cash society to a cashless society…this is the chance for you to enter the digital world.”

Indian Prime Minister Narendra Modi on Sunday urged the nation’s small traders and daily wage earners to embrace digital payment channels, as a cash crunch following the government’s surprise ban on high-value bank notes drags on.

Modi, speaking in his monthly address on national radio, said the government understands that millions have been affected by the ban on 500-rupee and 1000-rupees notes, but defended the action.

“I want to tell my small merchant brothers and sisters, this is the chance for you to enter the digital world,” Modi said speaking in Hindi, urging them to use mobile banking applications and credit-card swipe machines.

“It’s correct that a 100 percent cashless society is not possible. But why don’t we make a beginning for a less-cash society in India?,” Modi said. “We can gradually move from a less-cash society to a cashless society.”

More than 90 percent of consumer purchases in India are transacted in cash, Credit Suisse estimates. While a smartphone boom and falling mobile data prices have led to a surge in digital payments in recent years, the base still remains low.

Modi urged technology-savvy young people to spare some time teaching others how to use digital payment platforms.

But, as GoldMoney.com’s Alasdair Macleod explains, the economic consequences of Mr. Modi’s action are far more significant…

Two weeks ago, India’s Prime Minister Narendra Modi demonetised an estimated 86% of rupees in circulation, offering conversion into a bank account or into smaller currency notes until 31 December, after which these notes will have no redemption value.

Together with forgeries in circulation, it could be over 90% of all circulating money. The terms of redemption are so inconvenient for anyone other than black-marketeers, that for all purposes $50bn equivalent of rupees have been eliminated from the economy at a stroke, pending the introduction of new currency notes.

The sadness in all this is that Modi should have foreseen the extent of the disruption to the poor and rural communities, but has obviously forgotten the hard lessons of life learned in his youth as a lowly chai wallah. It could be that the Reserve Bank went along with it as a government puppet, consoling itself with the thought it would be a good way to write off obligations, believing a significant quantity of notes is likely never to be redeemed by black-marketeers and tax evaders. It effectively reduces the central bank’s obligations to the private sector at the expense of those the state likes least. However, the $10-20bn equivalent the state will make from it is less important than the disruptive economic effect and the likely impact on the rupee’s future purchasing power.

The purpose of this article is to look at the economic consequences of Modi’s action. Initial estimates by western macroeconomists of the effect on GDP seems to be benigni. It could be because their contacts in India are typically the more highly-paid city bourgeoisie, who rarely spend cash except for tips, using bank and credit cards more normally for everyday purchases. These people would almost certainly welcome moves to bring illegal trading under control and extend the income tax base, playing down the negatives. However, the cash immediately removed amounts to about 2.5% of GDP, eventually to be replaced at an unspecified time in the future by the new notes bearing a portrait of the Mahatma. But while these notes are shortly to become available, it could take months to convert ATMs and ensure their widespread availability.

If the long-term consequences will be to bring unrecorded transactions into the GDP statistic, some western macroeconomists postulate recorded GDP could end up rising faster than anyone expected before Modi’s action. This misses the point. Banning high denomination notes worth as little as $7.50 equivalent to be replaced by the new Ghandi notes has been a major disruption in most Indians’ lives, particularly for the rural population. Removing everyday money is like trying to run an engine without any oil in it. It seizes up, which is what the Indian economy is certain to do. India’s economy is therefore likely to face a short-term slump, which government economists will counter by reflating, in other words by increasing the quantity of money. It will do the economy no good, but nominal GDP, which is not the same thing, will eventually rise, to the satisfaction of the central planners.

Behind the confusion in government economists’ minds is a false conviction that GDP records the performance of an economy. This is wrong. GDP is just a money-total at a previous point in time, and no more than that. It is not a measure of economic progress or regress. A change in GDP reflects only a change in the quantity of money in the economy, so it is perfectly possible for an economy to contract, or even collapse, while nominal GDP rises. Not only is this fatally misunderstood by today’s economists, but this outcome has become far more likely for India, and will simply end up generating more monetary inflation from the banking system. Behind the Indian authorities’ poor grasp of the economic consequences of their actions are misconceptions common with establishment economists everywhere. However, it is likely that central bankers in India and elsewhere are at least vaguely aware of the long-term danger of increasing price inflation. But the consensus in banking circles is that more money and credit may be required to stave off recession, and even systemic risk. And in the case of systemic risk, cash is a danger because it allows the public to expose a bank’s insolvency. If only cash was somehow replaced, there could perhaps be greater control over economic and systemic outcomes.

All the signs of this loose thinking are there. We keep on hearing of central banks planning to do away with cash, and Modi’s action is consistent with this standpoint. His government is not only trying to eliminate black markets, but it is also brutally trying to eliminate economic dependence on physical cash. It rhymes with the direction of travel for central bank policy in the advanced economies as well as in the emerging.

Doubtless, for this reason, central banks everywhere will be watching the Indian experiment closely. But we can easily guess what their analysis will conclude. If the experiment succeeds, it will encourage them to proceed with their own plans to digitise money and dispense with the folding sort. If it doesn’t, failure will be deemed to be due to the peculiarities of the Indian economy and the failure of the Reserve Bank to implement policy effectively, so they will proceed with their plans anyway.

However, hopes that the elimination of cash will give central banks greater control over inflationary outcomes appear to be badly misplaced. Not only does history tell us the exact opposite is the case, and that the reality is central banks have no control over price outcomes, but subjective price theory also confirms. The pricing power of money is not and never has been in the control of central banks; it is a matter only for the users of money in their day-to-day transactions. Money’s use as money is wholly down to its public acceptance as money, as experience proves, and central banks’ abuse of this trust is ultimately dangerous, as so often demonstrated. For example, despite government diktats and heavy-handed enforcement, Zimbabwe’s currency has become at best, to put it politely, a replacement for another form of paper whose vital supply has been disrupted. The digital version has even less value, because it has no alternative use.

India and Gold

We must return to the specific subject of India, and the likely outcome of Modi’s clumsy attempt to eliminate means of payment using cash. It is almost certainly going to backfire. Indians have little respect for government as it is, and this action will only convince them with renewed purpose to have as little to do with the government and its money as possible. When the new Gandhi notes come into circulation, they will likely be rejected as the preferred money by growing numbers of a rightly suspicious public. This means that the rupee’s purchasing power will diminish more rapidly than if Modi had not disrupted what had become a relatively stable monetary situation.

Ordinary people in their actions are well ahead of western financial analysts, having quickly anticipated this outcome for themselves. Despite longstanding government attempts to persuade them otherwise, they are rushing to convert worthless rupees into the one form of money they have trusted for millennia and over which government has no control, gold. They know that priced in rupees, gold will be more expensive in the months to come, so anything that can be encashed will be encashed for gold, not rupees.

This is the reason why gold in India is now trading at a substantial premium to international prices. The Indian government restricts its supply because it has always seen gold, correctly, as a challenge to its own fiat money. Accordingly, the central planners condemn gold as being more appropriate to history than today’s economic environment. And having dismissed its relevance as money and as a superior store of value to the rupee, they see gold imports as unproductive hoarding. The government and central bank also appear to make the mistake of believing that if gold imports were eliminated, the balance of trade would improve accordingly. The result is various acts and regulations since the Gandhi era have only encouraged gold smuggling. The importation of gold has never halted, and responding to every twist and turn of monetary policy has increased over the long-term, and will continue to do so following Modi’s clumsy action.

The impact of government ineptness on the gold market is likely to be considerable. After a period of relative currency stability, gold demand, at the officially recorded level, had in fact declined earlier this year. The premium on gold was less than the new sales tax, putting many jewellers out of business, because they could not compete with smuggled gold, which bore no tax and attracted a lower premium than the sales tax. More jewellers will probably be put out of business by this latest action. Smuggling will consequently rise and rise, particularly if the rupee’s purchasing power declines because of escalating public distrust of it as money.

The central banking community, headed by the Bank for International Settlements, was concerned at Indian gold demand increasing at a time when Chinese citizens were absorbing most of the world’s free supply of newly-mined and scrap gold. It is almost certain that the appointment of Raghuram Rajan in September 2013 as Governor of the Reserve Bank of India had much to do with the urgency to bring Indian demand for gold under control, because he was and still is the BIS’s establishment man. He has generally failed in this mission, and his tenure was not renewed for reasons unknown, other than he preferred to return to the calmer pastures of academe and his Vice-Chairmanship of the Bank for International Settlements.

This is not characteristic of a career central banker at the height of his powers and influence. Perhaps Rajan realised his attempt to manage gold demand would never work, and Modi was proving too dangerous for his own legacy at the Reserve Bank to survive unblemished. He was recently quoted as saying that the RBI’s ability to say no to the government must be protected, some months after he declined the opportunity to serve a second term. Was this a reflection of something that happened?

In conclusion, the surprise money-grab by the Indian authorities intensifies the public’s perception of a corrupt, overly-bureaucratic, and ineffective government. The public’s suspicion that government paper money is ultimately worthless will have, in its collective mind at least, gained immeasurable credence. An accelerating decline in the purchasing power of the rupee is the most likely economic consequence of Mr Modi, ultimately destabilising for both the country and his government.

As we concluded previously, on a final philosophical point. Our entire monetary system depends on trust. A banknote is a piece of paper that says the RBI will give the bearer another similar piece of paper, or make an entry in an electronic ledger for that amount. The system works because everybody believes that those pieces of paper will be accepted by everybody else and therefore, money serves as an useful medium of exchange. This move has shaken that trust. Expecting a nation used to 90% cash transactions to ever trust government-sponsored digitzation is beyond farce and financial repression, it is monetray larceny.

One final question, will the police be enlisted to beat the population into a cash-less society also?

https://youtu.be/gZD5ojDPGT0

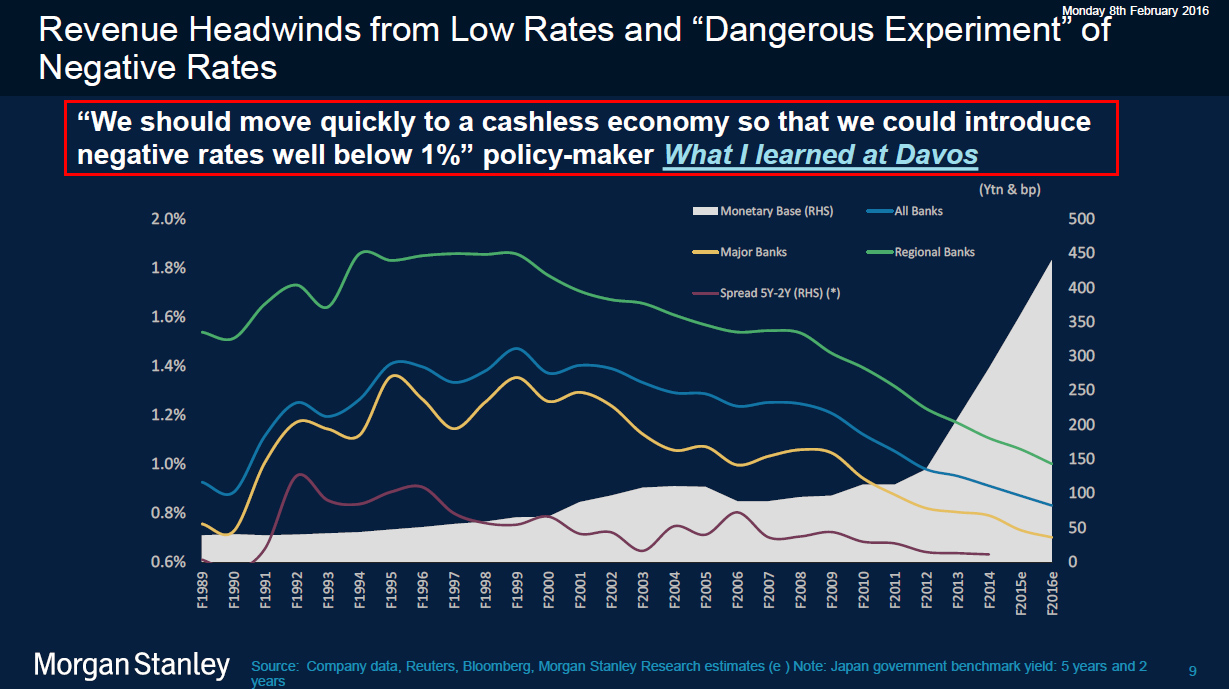

None of this should come as a surprise, of course, since we first pointed out the ‘disturbing’ slide in a Morgan Stanley presentation earlier this year…

While we have seen op-eds by both Bloomberg and FT urging the banning of cash, the most disturbing development we have seen yet in the push for a cashless society has come from the following slide in a Morgan Stanley presentation, one in which the bank’s head of EMEA equity research Huw van Steenis, pointed out the following…

… and added this:

One of the most surprising comments this year came from a closed session on fintech where I sat next to someone in policy circles who argued that we should move quickly to a cashless economy so that we could introduce negative rates well below 1% – as they were concerned that Larry Summers’ secular stagnation was indeed playing out and we would be stuck with negative rates for a decade in Europe. They felt below (1.5)% depositors would start to hoard notes, leading to yet further complexities for monetary policy.

Consider this the latest, and loudest, warning on the road to digital fiat serfdom.

* * *

PayPal: Donate in USD

PayPal: Donate in EUR

PayPal: Donate in GBP