… at this very moment, politicians from Spain’s Podemos to Italy Five Star movement are drafting memos demanding that the IMF evaluate their own debt sustainability. Or rather unsustainability.

– Did The IMF Just Open Pandora’s Box? (ZeroHedge, July 3, 2015):

By now it should be clear to all that the only reason why Germany has been so steadfast in its negotiating stance with Greece is because it knows very well that if it concedes to a public debt reduction (as opposed to haircut on debt held mostly by private entities such as hedge funds which already happened in 2012), then the rest of the PIIGS will come pouring in: first Italy, then Spain, then Portugal, then Ireland.

The problem is that while it took Europe some 5 years to transfer a little over €200 billion in Greek private debt exposure to the public balance sheet (by way of the ECB, EFSF, ESM and countless other ad hoc acronyms) at a cost of countless summits and endless negotiations, which may or may not result with the first casualty of the common currency which may prove to be reversible as soon as next week, nobody in Europe harbors any doubt that the same exercise can be repeated with Italy, or Spain, or even Portugal. They are just too big (and their nonperforming loans are in the hundreds of billions).

And yet, today, in a stunning display of the schism within the Troika, it was the IMF itself which explicitly stated that Greece is no longer viable unless there is both additional funding provided to the country, which can only happen if there is another massive debt haircut.

This is what the IMF said:

Even with concessional financing through 2018, debt would remain very high for decades and highly vulnerable to shocks. Assuming official (concessional) financing through end–2018, the debt-to-GDP ratio is projected at about 150 percent in 2020, and close to 140 percent in 2022 (see Figure 4ii). Using the thresholds agreed in November 2012, a haircut that yields a reduction in debt of over 30 percent of GDP would be required to meet the November 2012 debt targets. With debt remaining very high, any further deterioration in growth rates or in the mediumterm primary surplus relative to the revised baseline scenario discussed here would result in significant increases in debt and gross financing needs (see robustness tests in the next section below). This points to the high vulnerability of the debt dynamics.

And the kicker:

- “these new financing needs render the debt dynamics unsustainable.”

Bingo, because that is, in a nutshell, precisely what Tsipras and Varoufakis have been claiming since day one. As expected, a Greek government spokesman promptly said that the IMF report is in line with the Greek government’s view on debt.

What makes the IMF report even more odd, is not so much its content and position which have been largely known for quite some time now, but its timing: just three days before the Sunday referendum, Tsipras now has prima facie evidence to wave in front of the Greek people and say “see, we were right all along.”

It is exactly the case that only a “No” vote at this point would allow Greece to continue a negotiation which has already seen one of the three Troika members side with the Greek position. Should Greece vote “Yes”, it will make any future negotiation with the Troika impossible, and while the country will get a few months respite the resultant bank run after the bank reopen with the ECB’s blessing will mean that all Greece will do is buy itself a few months time. Only this time all the debt will still be due.

And, should hey vote “Yes”, this time the Greeks will only have themselves to blame for all the future pain, pain which will continue well after the mid-point of this century.

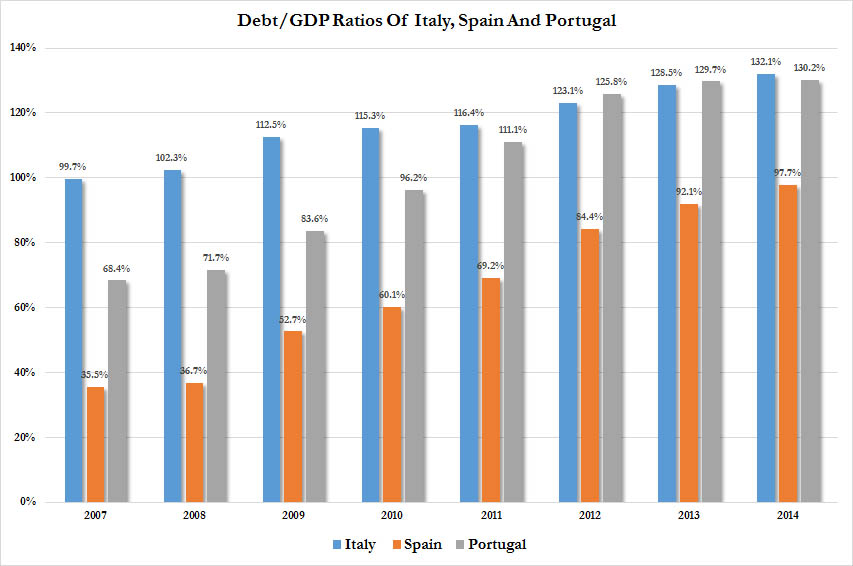

But ignoring Greece for a minute, what the IMF’s “debt sustainability analysis” has just done is open the door for every single other comparably insolvent peripheral European nation to knock on Christine Lagarde’s door and politely ask: “Mme Lagarde, if Greece is unsustainable, then why aren’t we?”

Because as the chart below shows, the debt situations of all the other peripheral European nations is just as “unsustainable.”

In this way, while the outcome of the Greek situation is currently unknown, it has also become moot, because at this very moment, politicians from Spain’s Podemos to Italy’s Five Star movement are drafting memos demanding that the IMF evaluate their own debt sustainability. Or rather unsustainability.

Perhaps more importantly, these same politicians will now dangle the prospect of an IMF admission that they, too, deserve a haircut as the catalyst to be elected into power. After all who can refuse that their life would be made so much better if only the country was permitted to selectively “default” on €50, €100, €200 billion or more in debt? Just elect this politician, or that, and watch your living standard soar…

And since the IMF has no choice but to agree that just like Greece all these nations are accordingly drowning in debt, Syriza’s sacrifice (assuming Tsipras fails to outnegotiate Merkel) will not have been in vain. In fact, it may very well end up that today the IMF opened up the Pandora’s box, one which, more than a Grexit, will destroy Merkel’s “united Europe” legacy.

The truth is even more harsh, the IMF is buried in debt, and under any careful scrutiny, it will expose the fact all the banks are insolvent.

Lets review one more time. First, Greece has already defaulted on IMF debt, that money is gone, so the IMF has to show the losses of billions upon billions in bonds, securities……and God only knows what other forms of debt they have claimed as assets, regardless it has been obvious to anyone Greek debt is worthless…..and has been for years. I read somewhere, perhaps here, that Greece has shown a debt level far outweighing any income for the past half a century…..

Somewhere in the first fake boom years after the 2002 crash, standard business practice was to take $100 million (borrowed?) and leverage it into $100 Billion, a 1000:1 ratio. After years of zero growth in any western economy, a couple of years ago, they started leveraging the leveraged funds. We are now in the quadrillions, and the most any of it might have been based upon was $100 million……Likely loaned as well, making all the quadrillions of debt created out of thin air.

Multiply this by hundreds or thousands all over the word, and it quickly becomes obvious the problem is serious, and thanks to Greece’s default to the IMF, the weakness is exposed. There is no way to pave over this one, the damage is too deep and far reaching.

The IMF can speak now, they are not being involved in any other lending to Greece. Even more, their losses are obvious to all who have invested in them.

This is a real set back for the greedy guts, and it has been a long time coming.

It had to happen.

How the US stock market continues to move as if it is unaffected by the enormous exposure the greedy guts face thanks to Greece is hard to watch. I figure the impact will hit them this coming week. The only product sold on the US, Euro and Chinese markets has been debt. Now that the debt market is crumbling, the markets will follow, rigged or not.

Debt has been over produced and oversold, 1000:1 is optimistic. The implosion that is already resulting cannot be stopped.

Germany has a lot more to fear than just the default of Italy, Spain, Portugal and Ireland…..Germany, along with France, Spain and Italy is underwriting 98% of all the Greek debt that is being defaulted upon as I write here. Germany, just like all the other Euro nations is mired in debt with debt to GDP well in excess of 100%. Every cent that comes in is already owed elsewhere, there is no money for improvements or jobs.

With the debt market failing, thousands more jobs will vanish.

Germany is in no position to stand the losses from a Greek default, this is one of the reasons their leaders have been so dogmatic, too much so, and their rigid refusal to work with them has cost them more than we can yet measure….but it is more than they can afford.

The same with France, Italy and Spain. None of them ought to have undertaken such a fool debt……..economic suicide.

Pandora’s box? Thats a good term for it.

What happened to the Greek economy is a mirror reflection of what happened to the US, especially in the real estate market…….Greenspan used to urge citizens to go ARMs because they could save thousands in such low rates….fixed rates were much more expensive……..

The mindless have indeed inherited the earth……From the UK Guardian:

http://www.theguardian.com/world/2015/jul/03/greece-overspending-defence-wages-taxation-economic-crisis