– Is Greece About To “Lose” Its Gold Again? (ZeroHedge, April 25, 2015):

When it comes to the topic of Greece, most pundits focus on two items: i) when will Greece finally run out of confiscated cash, and ii) will Greece fold to the Troika (and agree to another bailout(s) with even more austerity) or to Russia (and agree to the passage of the Russian Turkish Stream pipeline, potentially exiting NATO and becoming the most important European satellite of the USSR 2.0) once that moment arrives.

And yet what everyone appears to be forgetting is a nuanced clause buried deep in the term sheet of the second Greek bailout: a bailout whose terms will be ultimately reneged upon if and when Greece defaults on its debt to the Troika (either in or out of the Eurozone). Recall that as per our report from February 2012, in addition to losing its sovereignty years ago, Greece also lost something far more important. It’s gold:

To wit:

Ms. Katseli, an economist who was labor minister in the government of George Papandreou until she left in a cabinet reshuffle last June, was also upset that Greece’s lenders will have the right to seize the gold reserves in the Bank of Greece under the terms of the new deal.

The “new deal”referred to is the Second Greek Bailout, which either will be extended and lead to a third (and fourth, and fifth bailout, each with every more draconian terms until finally Greece does default), or will collapse at which point the Troika will indeed have the right to seize the Greek gold reserves.

What makes this case particularly curious, however, is that it won’t be the first time Greece will have “lost” its gold. In The Tower of Basel, citing the BIS archive from Febriary 9, 1931, Adam LeBor writes:

In February 1931, Gates McGarrah, the [BIS’s] American president, wrote to H. C. F. Finlayson, in Athens, asking about the Bank of Greece’s gold. Finlayson, a former British financial attaché in Berlin, was now an adviser to the Bank of Greece. Some of the Greek bank’s gold may have gone missing. Rather like nowadays, it seemed the accounting at the Bank of Greece left something to be desired. “What has ever happened to the gold of the Bank of Greece, some of which you thought might be left in our custody in Paris or elsewhere?” inquired McGarrah, who, as the president of the BIS might have been expected to know what it held and where. It might, McGarrah suggested, be a good time to find the Greek gold and place it with the BIS.

The BIS, wrote McGarrah, could give the Bank of Greece “all sorts of facilities, rather greater than those of a local Central Bank.” For example, if the Bank of Greece held gold at the Bank of France and wanted to buy another currency, it first had to buy francs from the Bank of France. The Bank of Greece then converted the francs to the second currency, with all the usual losses of exchange rates and commissions. However, if the Bank of Greece held gold at the Bank of France in the name of the BIS, the BIS could “give the Bank of Greece any currency it desires at any time and can fix an agreed rate without going through the actual exchange operation.” And, the BIS did not charge any commission.

And all Greece would need to do to get these copious and generous “benefits”would be to hand over its gold to the Bank of International Settlements. Of course, it would have to find it first…

But most importantly, and what ties everything together is that other historic event which took place in 1931.

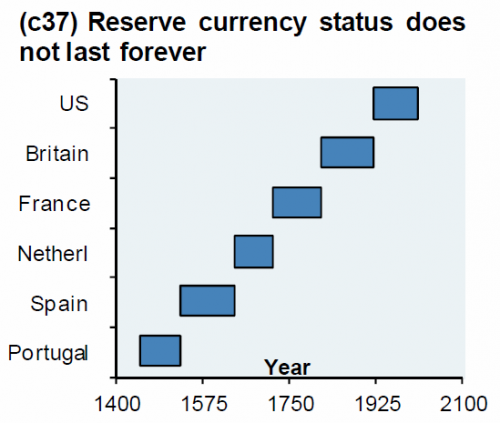

For those who may not be gold history buffs, this is what happened: in September of that year the Bank of England decided to formally (and for the final time) abandon the gold standard. And, as the chart below first posted on Zero Hedge many years ago, that decision, coupled with the great depression and the loss of confidence in the pound, ultimately ended the reserve status of the British currency, ushering the reserve currency status of the US Dollar.

A few months ago, when the Minutes from the Bank of England’s court were published for the first time in January, we learned precisely what happened months after the BIS casually inquired about the lost Greek gold. The Telegraph summarized it as follows:

At the time, sterling was pegged to bullion. This meant that the pound was worth a fixed amount compared to other currencies and gold itself. In order to ensure that sterling retained its value, the Bank of England was obligated to exchange gold for pounds at the specified rate.

However, as political turmoil engulfed the UK, the country’s first national government – a coalition between Labour and the Conservatives – presided over a budget crisis that triggered a run on the pound.

Minutes from the Bank’s court in 1931, published on Wednesday, detailed how foreign exchange reserves were being drained to such an extent that the gold standard had to be abandoned.

Up to that point, the gold standard had been preserved by loans from the Federal Reserve and the French central bank, with the Bank’s bullion reserves used as collateral. But Threadneedle Street decided in September that its reserves would run dry if New York and Paris withdrew support. Ernest Harvey, the Bank’s deputy governor at the time, wrote to Ramsay MacDonald, the prime minister, and Philip Snowden, the chancellor, on September 19, 1931, saying that reserves worth more than £100m were close to running out.

Mr Harvey wrote: “I am directed to state that the credits for $125,000,000 and Fcs 3,100,000,000 arranged by the Bank of England in New York and Paris respectively, are exhausted, and that the credit for $200,000,000 arranged in New York by His Majesty’s Government, together with credits for a total of Fcs 5 milliards [5bn] negotiated in Paris, are practically exhausted also.” “The heavy demands for exchange on New York and Paris still continue. In addition the Bank are being subjected to a drain of gold for Holland.

“Under these circumstances, the Bank consider that, having regard to the above commitments and to contingencies that may arise, it would be impossible for them to meet the demands for gold with which they would be faced on withdrawal of support from the New York and Paris exchanges.

“The Bank therefore feel it their duty to represent that, in their opinion, it is expedient in the national interest that they should be relieved of their obligation to sell gold under the provisions of [the Gold Standard Act 1925].”

In other words, the Bank of England became insolvent in hard money terms, and was forced to back the currency with nothing but its “faith and credit.” No wonder at that moment the sun had set on the British Pound.

40 years later, Nixon finally did the same with the US Dollar (but not before FDR confiscated all gold as the US also devalued its currency by 40% in “hard money terms” on January 30, 1934 with the Gold Reserve Act), but in the absence of any gold-backed currency to arise (oh, hi Beijing), the dollar still remains the one-eyed king in the land of blind fiat.

Still, one wonders: the last time Greek gold was “lost” a historic event for the world’s reserve currencie took place. Is Greek gold about to be “lost” once more, and will monetary history rhyme?