– Western Banks Scramble As China’s “Rehypothecation Evaporation” Goes Global (ZeroHedge, June 7, 2014):

While we have warned about the problem with near-infinitely rehypothecated physical/funding commodities/metals, be they gold or copper, many times in the past, and most recently here, it was only this week that China finally admitted it has a major problem involving not just the commodities participating in funding deals – in this case copper and aluminum – but specifically their infinite rehypothecation, which usually results in the actual underlying metal mysteriously “disappearing”, as in it never was there to begin with. It would appear our fears of global contagion (through various transmission channels) are now coming true as WSJ reports that as many as a half-dozen banks are trying to determine whether the collateral for loans they made to commodities traders was used fraudulently by a third party to obtain other loans. As we detailed previously, it appears the day when the Commodity Funding Deals finally end is fast approaching… and as we note below, why that will certainly be a watershed event.

As we warned would happen, The Wall Street Journal reports that as many as a half-dozen banks are trying to determine whether the collateral for loans they made to commodities traders was used fraudulently by a third party to obtain other loans, according to people with knowledge of the matter.

The banks, including Citigroup Inc. and Standard Chartered, provided loans to trading firms that were backed by metals such as copper and aluminum stored at one of China’s biggest ports, the people said. The trading firms hold the deed to the metal, which can be used to secure financing, but the metal stays in a warehouse. Banks fear a private Chinese company may have used the metal as collateral to get multiple loans, potentially defrauding the lenders and trading firms.

Two of the people with knowledge of the matter estimated the value of the loans and collateral at several hundred million dollars.

The banks are frustrated because they haven’t been able to get access to the collateral, the people said.

The metals are stored at Qingdao Port, which administers the warehouses.

An executive at one of the banks said the title documents from the warehouses may have been photocopied and used to secure the loans.

The vicious cycle has begun…

The fear in the copper market is that banks will become more cautious about allowing metal to be used as collateral.

Many traders and analysts believe a significant amount of China’s metal imports are used for this purpose.

China is the world’s top copper consumer, so anything that threatens imports can send shock waves through the metals market.

Copper prices have fallen 4% in the past four days after media reports on the potential fraud. In March, prices fell nearly 10% amid worries the Chinese government was preparing to crack down on copper-backed loans.

On Friday, copper for June delivery, the front-month contract, fell 3.8 cents, or 1.2%, to $3.0530 a pound, on the Comex division of the New York Mercantile Exchange.

The potential fraud raises questions about the integrity of commodities warehouses in China, one of the world’s largest users of commodities, and how trading is financed.

There has been concern among policy makers that commodities in China are being used to get financing for cash-strapped companies. As credit tightens and the nation’s economy slows, some investors worry that the commodities will be dumped onto the market as banks seize collateral, potentially knocking down prices.

There is also concern that demand in China will collapse because so much of the metal had been stockpiled in warehouses.

This is not just a Chinese banking system issue anymore as major Western banks and trading shops are now directly affected… and are scrambling…

Two of the trading houses that may be exposed to the possible fraud are Geneva-based Mercuria Energy Group Ltd., which mostly trades oil, energy products and industrial commodities, and Glencore PLC, the Switzerland-based mining and trading company, according to people familiar with the matter.

Mercuria, which in March agreed to buy the physical commodities business of J.P. Morgan Chase & Co., didn’t respond to requests for comment. A Glencore official declined to comment.

In addition to Citigroup and Standard Chartered, the banks potentially affected include ABN Amro Bank NV, BNP Paribas SA, Natixis and Standard Bank PLC, the people familiar with the matter said.

Standard Bank said it is investigating “potential irregularities at the port at this time and will be working with the local authorities as part of its investigations.” The bank said it couldn’t quantify any potential loss.

ABN and BNP declined to comment. Natixis didn’t respond to a request for comment.

As we detailed previously, it appears the day when the Commodity Funding Deals finally end is fast approaching.

Here is Goldman’s take on what will certainly be a watershed event – one which will certainly dwarf the recent Chaori Solar default in its significance and scale.

Financing deal concerns mounting as CNY volatility rises

Concerns on an unwind of commodity financing deals trigger selloff

The recent sell-off in copper and iron ore prices reflects the market’s ongoing concerns regarding the impact of a potential unwind of Chinese commodity financing deals, though the weak underlying market fundamentals should not be discounted. The concerns intensified following the recent CNY depreciation which has raised uncertainty regarding the profitability of the deals and the impact on different asset classes were they to unwind. Up to 1mt of copper and 30mt of iron ore could be released were the deals to unwind, which would be bearish given the relatively limited physical liquidity to absorb the shock.

CCFDs are facilitating China’s total credit growth

We believe CCFDs are ongoing and facilitating ‘hot money’ inflows into China by providing a mechanism to import low-cost foreign financing. In general, the profitability of most hedged commodity financing deals remains substantial (iron ore is the exception), due to a still positive CNY and USD interest rate differential, limited depreciation in the CNY forward curve and available commodity supply. In 2013, ‘hot money’ accounted for c. 42% of the growth in China’s monetary base of which we estimate thatCCFDs contributed US$81-160 bn or c.31% of China’s total FX short-termloans. Given this, it is crucial for the government to manage the immediate impact of ‘hot money’ flow changes on the economy and markets.

More commodities are used; a medium-term unwind is bearish

An increasing range of commodities are being used to raise foreign financing, which now includes iron ore, soybeans, palm oil, rubber, zinc, and aluminum, as well as gold, copper, and nickel. CCFDs create excess physical demand and tighten the physical markets artificially; in contrast, an unwind creates excess supply and thus is bearish to prices. We think CCFDs will be unwound over the medium term, mainly triggered by an increase in Chinese FX volatility, as indicated by recent CNY depreciation and PBOC’s latest move to widen the daily trading band. FX volatility could result in a higher cost of currency hedging, effectively closing the interest rate arbitrage. Higher US rates are another likely catalyst for an unwind in the long run. A continuous CNY depreciation in the short term, however, would trigger some deals to be unwound sooner than expected, and hence place downside risks to our short-term commodity price forecasts.

It should now become apparent why the ongoing sharp devaluation of the CNY, far more than merely impacting a few massively levered speculators, and recall that the European Knock In point of maximum vega is about USDCNY 6.20 as discussed previously, will have a far more broad hit to asset levels not just in China but across the world if and when the inevitable moment of CCFD unwind finally begins, and in a reflexive fashion, initial selling begets more selling, more CNY devaluation, greater margin calls, further CCFD unwinds, and so on, until finally the PBOC has no choice but to come in and bail out the financial system one more time.

For those unfamiliar with the concept of CCFD, and too lazy to read our previous article on the topic, here is Goldman’s Roger Yuan with a succinct summary of just why these key component of China’s shadow funding mechanism are so important on the way up… and down.

Days numbered for Chinese commodity financing deals

As part of a broader shift in China’s funding base from domestic to various foreign funding vehicles, Chinese commodity financing deals have become increasingly prevalent, owing to the combination of the relatively high level of Chinese interest rates and the existence of Chinese capital controls. Financing deals use commodities and other goods as a tool to unlock the interest rate differential, with potential implications for Chinese growth, China’s linkage with ex-China interest rates, CNY volatility and commodity market pricing.

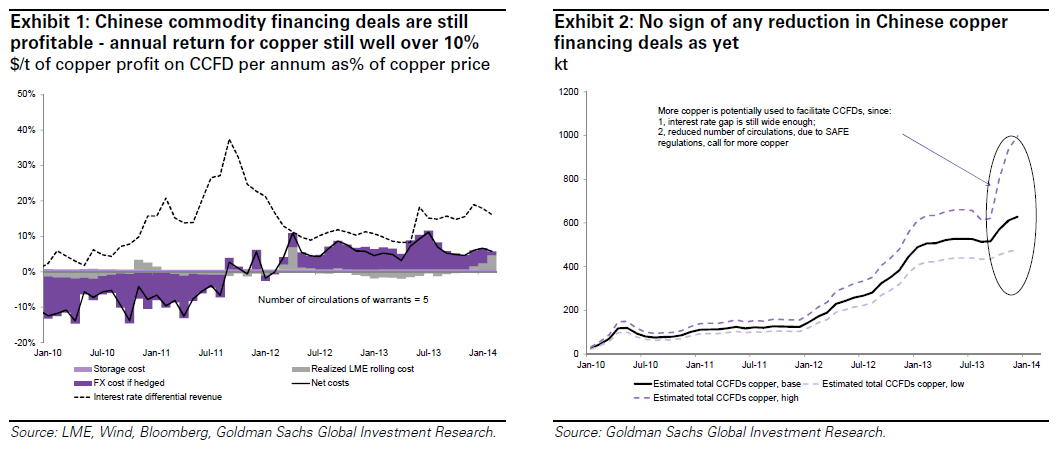

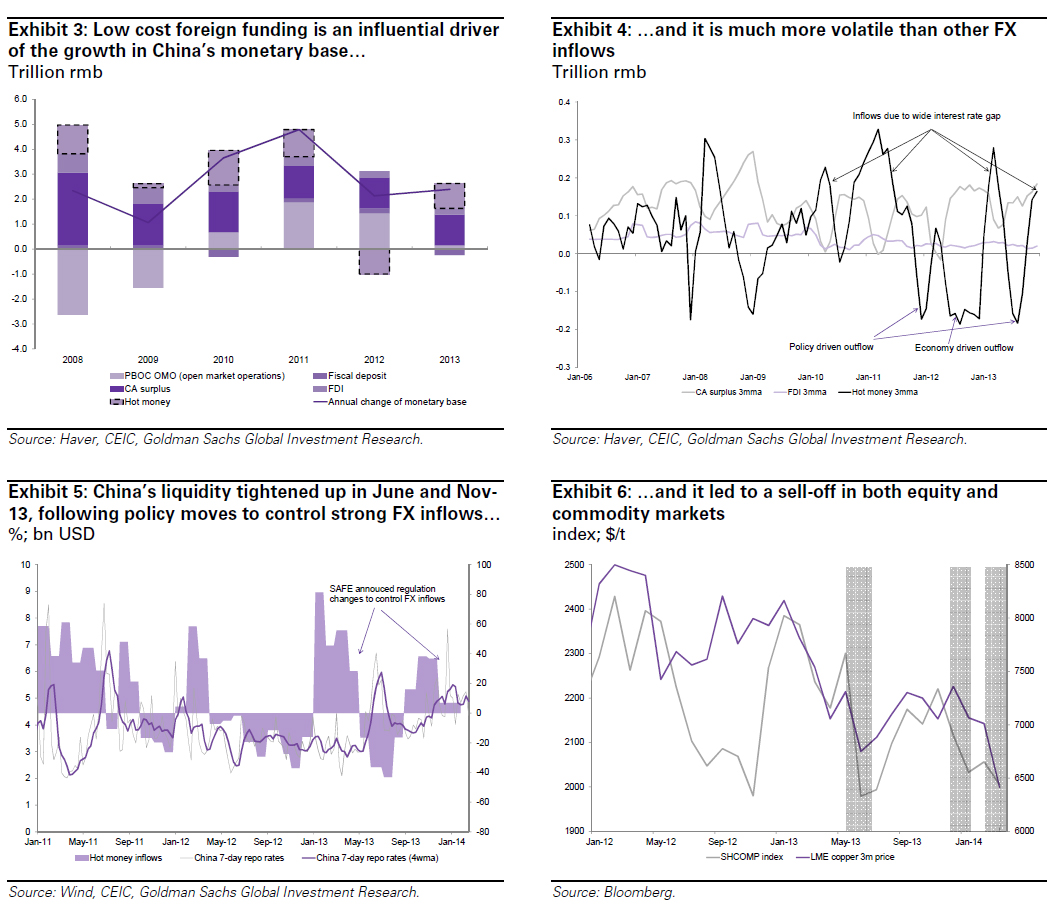

In contrast to some media reports, we find that the bulk of Chinese commodity financing deals are ongoing, facilitating ‘hot money’ inflows into China and providing a mechanism to import low cost foreign financing. In general, the profitability of most currency and commodity hedged Chinese commodity financing deals remains substantial, owing to a still positive CNY and USD based interest rate differential (>4%), limited depreciation in the CNY over the past month (<2%) and the CNY forward curve (limited cost of hedging the currency exposure), and a lack of tightness in the underlying commodity (i.e. limited cost of hedging the commodity). Returns in copper are still >10% (Exhibit 1), and up to 1mt of physical copper could still be tied up in deals (Exhibit 2).

While triggered by concerns about Chinese credit following the Chaori default, an unwind in iron ore financing deals, and concerns about an unwind in copper financing deals, the recent copper price weakness has reflected the combination of sluggish Chinese demand growth and strong global copper supply growth, rather than a financing deal unwind. Supporting this assertion is the fact that nickel (to an even greater extent than copper), and zinc both have a sizeable amount of exposure to financing deals, and their prices have substantially outperformed copper. Further, were this a true copper financing deal unwind, Chinese bonded copper prices would have led the price declines (instead they lagged the domestic Shanghai copper price declines), Chinese bonded stocks would have declined (instead they have risen) and the LME futures curve would likely have moved into contango (it remains in backwardation).

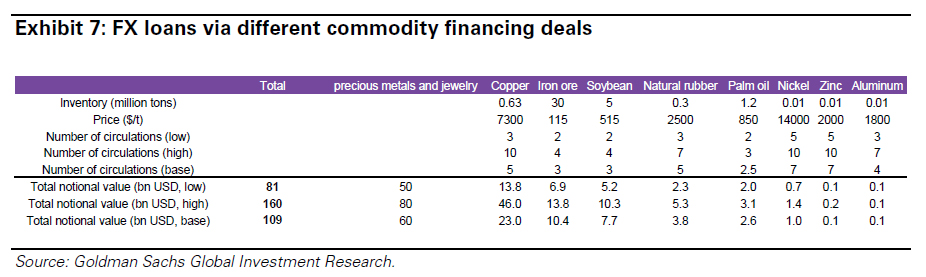

More broadly, the main reason why the government has not shut down ‘hot money’ inflows in an abrupt fashion to date, in our opinion, is that a complete shutdown could have major consequences for China’s short-term liquidity. Indeed, China’s economic growth is increasingly supported by different types of FX inflows, including those from commodity financing deals, as they can bring in low cost foreign funding and increase China’s monetary base, the foundation of both China’s rapid credit growth and solid economy growth. In 2013, we estimate that c.42% of the increase of China’s monetary base can be attributed to the low cost foreign funding or the ‘hot money’ inflows (Exhibit 3).

These FX / hot money inflows are of substantial size and high volatility (Exhibit 4) and the government attempts to smoothly manage the short-term liquidity cycle in response to these flows. When these flows are very strong China tends to respond (Exhibit 5), as in June and December 2013, as well as February/March 2014, with bearish implications for equities and commodities (Exhibit 6).

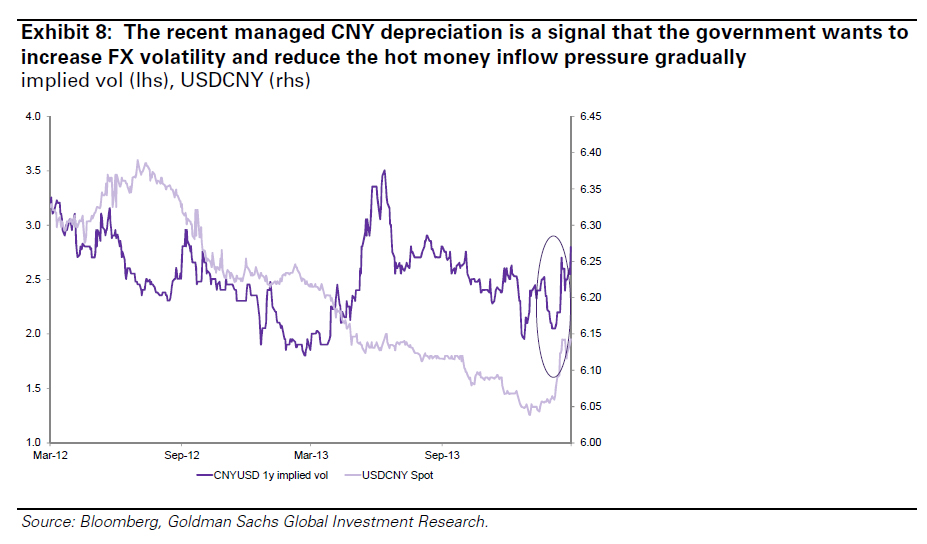

There are three main drivers of ‘hot money’ inflows: commodity financing deals, overinvoicing exports, and the black market. In this article, we focus on the Chinese commodity financing deal channel, which has by our estimates facilitated roughly US$81-160 bn of FX inflows since 2010, which is c.31% of China’s total FX short-term borrowings (duration < 1 year) (Exhibit 7). Of these deals, gold, copper and iron ore are three leading commodities, followed by soybean, palm oil, natural rubber, nickel, zinc and aluminum.

One reason why the range of commodities and the amount of each of those commodities being used for financing purposes has increased since mid-2013 is that the Chinese government moved to reduce the amount of money that can be borrowed per commodity unit. This reduction in apparent financing deal ‘leverage’6 (to c.3-10 times the value of the commodity from much higher levels a year ago), has meant that larger amounts of commodities are needed to raise the same amount of low cost foreign funding. In copper’s case for example, the amount of copper used in financing deals could have risen from 500kt to 1mt over the past nine months, as shown in Exhibit 2.

Looking ahead, our view is that Chinese commodity financing deals will gradually unwind over the medium term (the next 12-24 months), driven by an increase in FX hedging costs, which would slowly erode financing deal profitability and eventually close the interest rate arbitrage. Indeed, we expect that the government will continue to increase FX volatility in order to manage the hot money inflow cycle, thus increasing FX hedging among broader market participants, and raising the cost of hedging the currency for commodity financing deals. This FX policy outlook would be in line with the government’s policy targets of gradually increasing the CNY trading band before eventually loosening the nation’s capital controls, and is likely to occur before the CNY/USD interest rate differentials close, based on our Economists’ forecasts. Finally, an abrupt government crackdown on Chinese commodity financing deals, even with an offsetting monetary stimulus package, is unlikely in our view, given the potential negative impact this could have on credit and thus economic growth.

With respect to the impact of an unwind in Chinese commodity financing deals on China’s economic growth, we expect that the government will actively manage the impact on domestic credit creation, however we note that this process, if not managed perfectly, will not be without downside risks to Chinese growth.

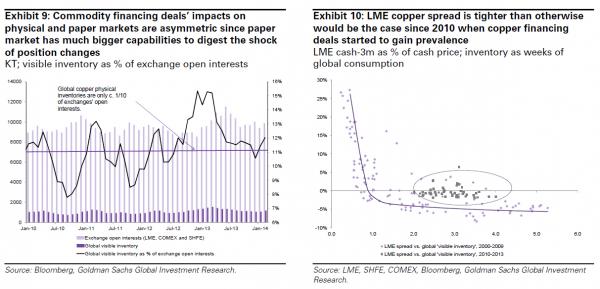

From a commodity market perspective, financing deals create excess physical demand and tighten the physical markets, using part of the profits from the CNY/USD interest rate differential to pay to hold the physical commodity. While commodity financing deals are usually neutral in terms of their commodity position owing to an offsetting commodity futures hedge, the impact of the purchasing of the physical commodity on the physical market is likely to be larger than the impact of the selling of the commodity futures on the futures market (ZH: unless of course momentum algos take offsetting commodity futures hedge selling in, say, gold and boost, or “ignite” the downward momentum to a far greater degree than the offsetting physical buying, making a recursive pattern whereby buying physical ends up resulting in a lower physical price as has been the case with gold over the past year). This reflects the fact that physical inventory is much smaller than the open interest in the futures market (Exhibit 9). As well as placing upward pressure on the physical price, Chinese commodity financing deals ‘tighten’ the spread between the physical commodity price and the futures price (Exhibit 10).

In this context, an unwind of Chinese commodity financing deals would likely result in an increase in availability of physical inventory (physical selling), and an increase in futures buying (buying back the hedge) – thereby resulting in a lower physical price than futures price, as well as resulting in a lower overall price curve (or full carry) (Exhibit 11).

Finally, as we showed before when it comes to commodity financing deals, in terms of total notional value, both copper and aluminum pale by comparison to the one metal most used (by value) in China as a funding substitute: gold

As we commented previously:

When we previously contemplated what the end of funding deals (which the PBOC and the China Politburo seems rather set on) may mean for the price of other commodities, we agreed with Goldman that it would be certainly negative. And yet in the case of gold, it just may be that even if China were to dump its physical to some willing 3rd party buyer, its inevitable cover of futures “hedges”, i.e. buying gold in the paper market, may not only offset the physical selling, but send the price of gold back to levels seen at the end of 2012 when gold CCFDs really took off in earnest.

In other words, from a purely mechanistical standpoint, the unwind of China’s shadow banking system, while negative for all non-precious metals-based commodities, may be just the gift that all those patient gold (and silver) investors have been waiting for. This of course, excludes the impact of what the bursting of the Chinese credit bubble would do to faith in the globalized, debt-driven status quo. Add that into the picture, and into the future demand for gold, and suddenly things get really exciting.

So if tens of thousands of tons of copper and aluminum are suddenly “missing”, one can assuredly say: “at least the gold is still there.” Right?

* * *

One more thing… we don’t remember seeing “the breaking of infinitely rehypothecated collateral chains” in the Stress Test documentation… makes you wonder just how much collateral is really there on the balance sheets of the West’s biggest banks…

It isn’t just China, I assure you. It is all of them. The implosion has begun. China is the first to fall, but a house of straw used to spin into gold is doomed to fail….these crooks know no bounds.

What a mess, and most fool Americans don’t realize it is happening to them………they listen to US media. I wonder how long they can keep the market afloat with this news out……..?