– American students are well over $1 trillion in debt, and it’s starting to hurt everyone (TIME, Feb 26, 2014):

American students are well over $1 trillion in debt, and it’s starting to hurt everyone, economists say

Chris Rong did everything right. A 23-year-old dentistry student in New York, Chris excelled at one of the country’s top high schools, breezed through college, and is now studying dentistry at one of the best dental schools in the nation.

But it may be a long time before he sees any rewards. He’s moved back home with his parents in Bayside, Queens—an hour-and-a-half commute each way to class at the New York University’s College of Dentistry—and by the time he graduates in 2016, he’ll face $400,000 in student loans. “If the money weren’t a problem I would live on my own,” says Rong. “My debt is hanging over my mind. I’m taking that all on myself.”

Rong isn’t alone. Across the country, students are taking on increasingly large amounts of debt to pay for heftier education tuitions. Figures released last week by the Federal Reserve of New York show that aggregate student loans nationwide have continued to rise. At the end of 2003, American students and graduates owed just $253 billion in aggregate debt; by the end of 2013, American students’ debt had ballooned to a total of $1.08 trillion, an increase of over 300%. In the past year alone, aggregate student debt grew 10%. By comparison, overall debt grew just 43% in the last decade and 1.6% over the past year.

According to a December study by the Institute for College Access & Success, seven out of 10 students in the class of 2012 graduated with student loans, and the average amount of debt among students who owed was $29,400. There’s no clear end in sight. ”The total amount of student debt is growing basically at a constant rate,” Wilbert van der Klaauw, an economist with the Federal Reserve Bank of New York tells TIME. “The inflow is much higher than the outflow, which is likely to continue in the future as reliance on student loans for college is expected to remain high.”

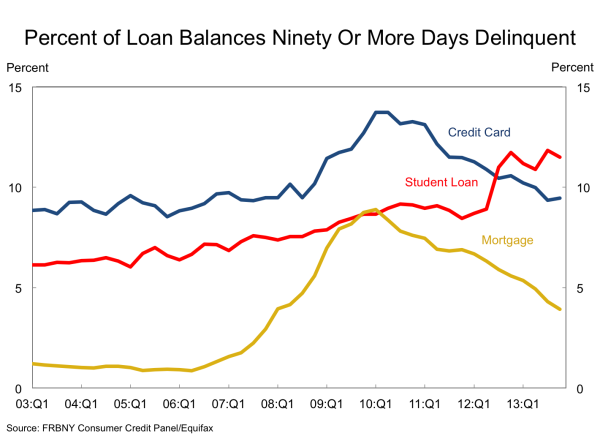

Debt is painful for many students, and an increasing number of graduates are unable to pay back their loans on time. Delinquencies on student loans have risen dramatically over the past decade: 11.5 percent of graduates were at least 90 days late on paying back their loans at the end of 2013, compared with 6.2 percent delinquencies on student loans in 2003. Moreover, the Fed’s figures on delinquencies hide more stark data: nearly half of all students with debt aren’t currently in repayment thanks to deferments and forbearances and the fact that students are not expected to pay while they’re in school, according to van der Klaauw. What that means is that for the graduates who are actually expected to pay their loans now, the delinquency rate is roughly double the 11.5% figure.

Delinquencies on student loans rose to 11.5% in the last quarter of 2013, even as credit card and mortgage delinquencies fell. Evidence suggests that student loan delinquencies for graduates actually expected to make payments are far higher.

Why are student debts and delinquencies continuing to rise? One answer is that the cost of higher educations is increasing. Between the 2000-2001 academic year and the 2010-2011 academic year, the annual cost of a degree at public and private 2- and 4-year institutions rose 70%, from an average of $10,820 to $18,497, according to data provided by the federal government’s Institute of Education Sciences. Families’ incomes aren’t rising at the same rate, so students are forced to take out more loans.

On the plus side, more students than ever before are attending college, which is a certainly a good thing, as van der Klaauw points out, even if it is a contributing to factor to overall debt increasing. A degree is usually worth the cost of college, even if the price tag is increasingly tough to bear. “It is always important to keep in mind that the average returns to a college degree remain high,” van der Klaauw says.

But a more pernicious explanation of rising debts is that outstanding student loans tends to linger for years, as interest rates accumulate debt and students decide to pay off other loans first. Student debt piles on because it takes years to pay them off, and they can’t afford to pay back such hefty loans until later in their careers. For example, some dentistry school graduates sometimes intentionally choose to default on their student loans in order to pay the staggeringly high costs of opening their own dental practice, Rong says.

For Rong, avoiding default on his $400,000 student loans may involve some clever thinking once he graduates. Rong says he’s entertained the idea of joining the military, or moving to a state with no income tax, like Texas, so he can pay off his debts more quickly. “I was just going to stay in New York after graduating, but now I realize there’s so much on my plate,” he explains. “When you take out loans, you’re taking years off of what you want to do and where you really want to be.”

Students across the country are trapped by their debts and often unable to take advantage of the freedom that a college degree should theoretically afford them. Julia Handel is the marketing manager for celebrity New York chef David Burke. The 2012 Ithaca College graduate is making over $40,000 a year, which is better than many of her friends. But she had $75,000 in loans, and it’ll take her at least 15 years to pay off her debts. For now, Handel is officially on her parents’ lease but crashing with her boyfriend, pinching pennies and paying back $700 every month. She may have to give up her dream of going to culinary school, and at this point, she can definitely cross off the idea of renting her own apartment.

By the time Handel pays off her loans, she may be nearly 40. “Whenever I do anything, loans are always in the back of my mind,” she says. “It controls what I do every day and what I spend my money on.”

Student debt doesn’t just weigh heavily on graduates. Evidence is growing that student loans may be dragging down the overall economy, not just individuals. Think about it this way: if students have significant debts, it means they’re less likely to spend money on other goods and services, and it also means they’re less likely to take out a mortgage on a house. Consumer purchasing is the primary driver of the U.S. economy, and mortgages and auto loans play a huge role as well. There aren’t any comprehensive, hard numbers yet on how much of a drag student debt may be on the economy, but “the associations definitely suggest that growing student debt is a drag on consumption,” says van der Klaauw. “This is still something we’re discussing. There are a range of views on this. My personal view is that the increasing reliance on student loans for financing college education is going to be a drag on consumption for some time.”

Knowing the kind of debt he’ll face once he graduates, Rong says he rarely goes to happy hours, and Handel says she’s much less likely to get regular haircuts, schedule doctor prompt doctors’ appointments, or buy the small things that add up—and, in aggregate, eventually prop up the economy and drive GDP growth. “It’s the little things,” she says. “Putting off a haircut for a long time, getting more makeup, prescriptions, or doctors appointments, the things that I don’t even think cost money but end up adding up a lot.”

It’s also become harder and harder to qualify for a mortgage if you have student loans, says Andrew Haughwout, another economist with the New York Federal Reserve. Banks tightened their underwriting standards after recession and are now much less willing to grant house and auto loans at low-interest rates, particularly for graduates with more debt than ever before. That’s slowing down the housing recovery and the construction markets.

In 2005, before the Great Recession, having student loans was a good indicator that a graduate also had a mortgage. Student loans usually indicated a higher level of education, a higher salary, and better credit-worthiness. Better-educated, higher-earning people were more likely to take have the capital and the wherewithal to take out a mortgage; but now, that dynamic has changed. Bigger debts mean college graduates are less likely to take out mortgages than they used to be, dampening economic growth. “Now that’s kind of gone away, that relationship,” Haughwout says. “Knowing that someone has student debt doesn’t tell you very much at all about whether they’re going to have a mortgage in spite of the fact that it probably still signals higher level of education.”

Is college still worth it? Yes, without a doubt. But you’re going to need a lot of patience and a lot of luck, class of 2014.

… without a doubt???

You’re going to need rich parents with a lot of connections.

And yes, good luck!